Here’s the ProShares VIX Short-Term Futures ETF (VIXY), the ETF I use most often to try to hedge against sudden market breakdowns. The ProShares Short S&P 500 ETF (SH), ProShares Short QQQ (PSQ), ProShares Short Russell 2000 (RWM), and other single inverse ETFs are part of the mix. However, their impact is more mild, and thus more capital is required to get the desired outcomes.

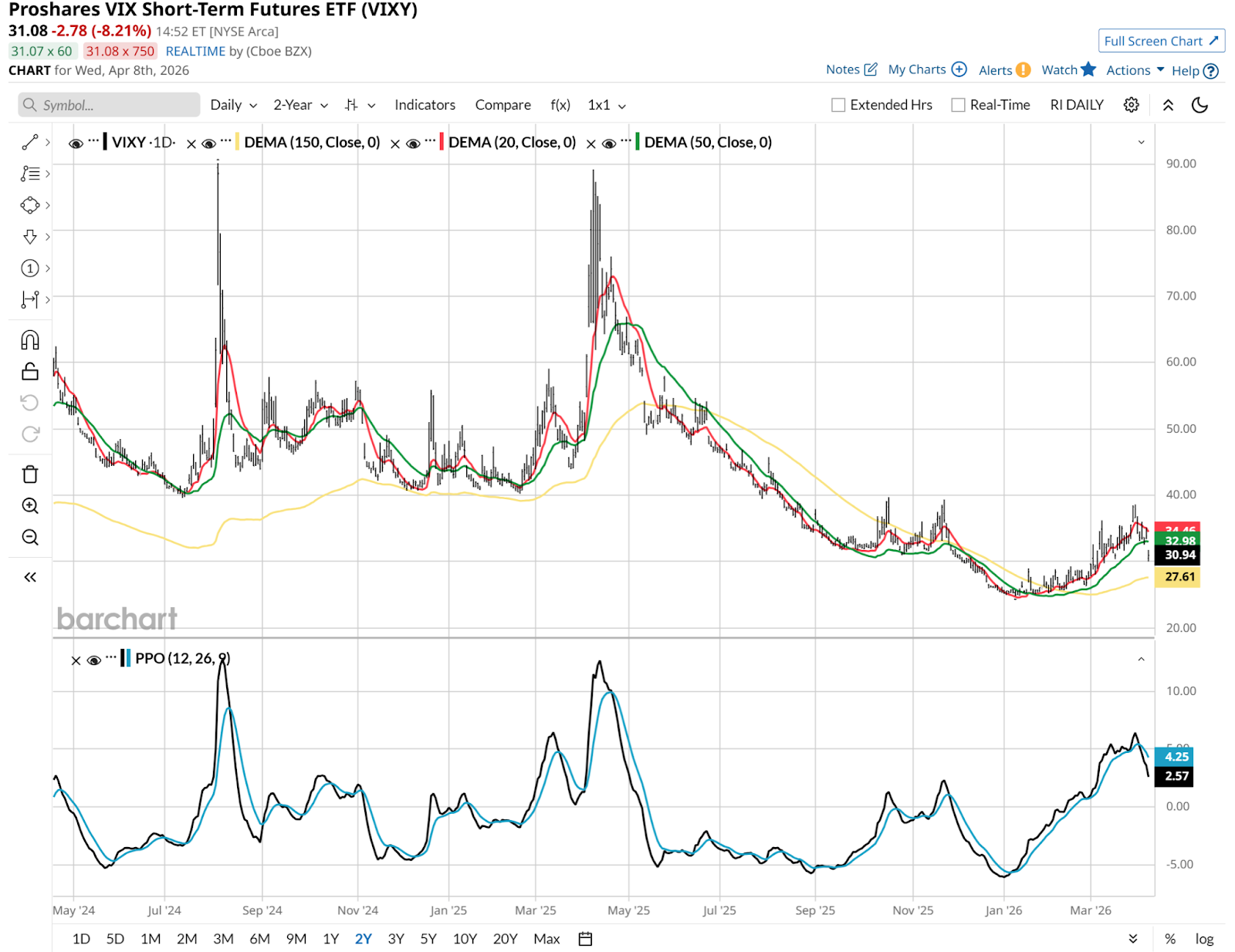

Leveraged inverse ETFs are useful too, but they still require more capital than a VIX volatility-driven ETF. Like VIXY. Here’s its daily chart going back two years.

I bring this up because, while we just saw this ETF plunge by more than 8% intraday Wednesday, that followed a 50% up move from early January through late March of this year. And it renews my faith in using VIX-tracking ETFs in a specific way. As a surrogate or replacement for S&P 500 ETF (SPY) put options.

This is not the most precise analysis, but it is intended to make a point. For those who prefer not to use options, or who don’t want to use them after VIX has recently spiked, these ETFs can be handy tools.

How VIXY Compares to Buying SPY Put Options

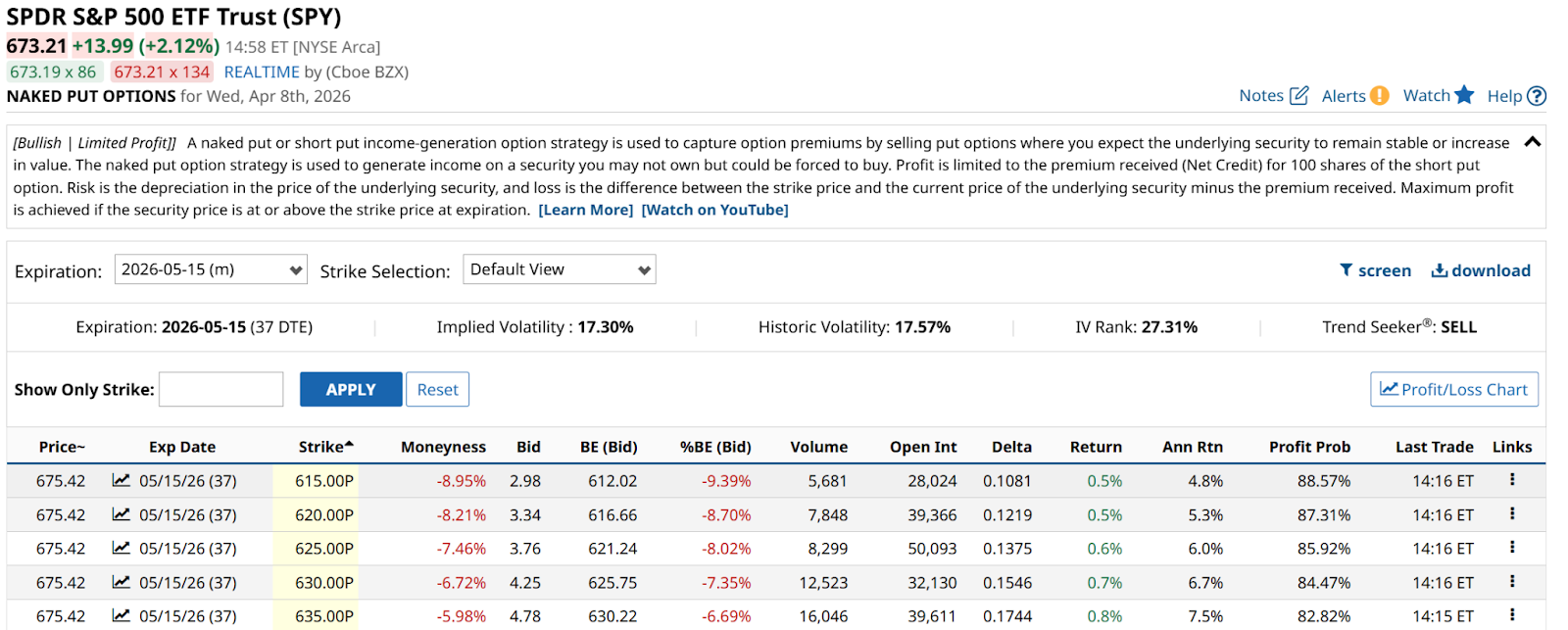

Here’s an array of next-month put contracts for SPY. That’s a similar impact, at least on a single-day basis. And that makes for a decent proxy.

For the first time since the “Hormuz Hurricane” sent shockwaves through the global tape in March, the Cboe Volatility Index ($VIX) finally dipped back below the psychological 20 level. But it didn’t stay there long.

Still, this recent round trip in VIXY and other VIX-oriented ETFs reminds us that the index is still relevant. There has been much talk in 2026 about how the rise of zero days to expiration (0DTE) options has “broken” the VIX, making it less relevant as a predictor of market stress. However, the recent spike to 31 in March proved that when a genuine macro shock hits, the VIX remains the ultimate fire alarm.

The VIX is uniquely relevant because it doesn’t just measure movement; it measures implied volatility. That’s the price investors are willing to pay for insurance. When the VIX drops below 20, insurance becomes cheaper. For an equity-focused investor, this creates an opportunity to use VIXY call options as a direct surrogate for S&P 500 put options. And its opposite ETF, SVXY (SVXY), as an S&P 500 call option replacement.

Many DIY investors default to buying SPX put options to hedge their portfolios, but this can be a wasted research exercise. SPX puts suffer from heavy time decay (theta) and can be prohibitively expensive during a slow-grinding selloff. The VIX offers an ETF-packaged alternative.

Convexity: Taking Big Shots with Small Amounts of Money

“Convexity” is really my favorite word for this year, as I’m finding increased use of this concept. That’s where you buy something way out of the money, and allow the initial shock value of a market reversal to turn a small amount into a much bigger amount. This is how I “take big shots with small amounts of money.”

VIX call options exhibit extreme convexity. Because the VIX is mean-reverting, it tends to explode upward during a crash far more violently than the S&P 500 falls. A 5% drop in the SPX can easily trigger a 40% spike in the VIX. This means you can often achieve the same level of protection using a much smaller amount of capital in VIX calls than you would in SPX puts.

But to me, the biggest feature of VIXY and other VIX ETFs is what I call the “crouching tiger, hidden dragon” effect, playing off an old movie title.

When the VIX is below 20, VIX hedging gets cheap. When it drops below 15, it is a great hedge. You are essentially buying a fire extinguisher when nobody smells smoke. If the ceasefire fails to hold, the VIX will be the first asset to react. That could create a scenario where a very small position (say 1%-5% of the portfolio, more if you are really daring) can offset a ton of stock market losses.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart