Oil prices jumped 5% overnight as OPEC+ announced a surprise production cut of 1.65 million barrels per day. The cut will start in May and last through the end of the year. Major oil producers like Saudi Arabia, Russia, and Iraq are making significant production cuts.

Oil prices jumped 5% overnight as OPEC+ announced a surprise production cut of 1.65 million barrels per day. The cut will start in May and last through the end of the year. Major oil producers like Saudi Arabia, Russia, and Iraq are making significant production cuts.

Here’s the full breakdown of production cuts:

- Saudi Arabia: 500,000 barrels

- Russia: 500,000 (this was a seasonal cut that Russia decided to maintain until the end of 2023)

- Iraq: 211,000

- United Arab Emirates: 144,000

- Kuwait: 128,000

- Kazakhstan: 78,000

- Algeria: 44,000

- Oman: 40,000

The cut comes as many commentators suggested the United States should replenish the Strategic Petroleum Reserve (SPR) when oil prices were in the $60s, the lowest level since 2021. The White House called the cuts “ill-advised” in response.

Higher oil prices are also a big thorn in the Federal Reserve’s side. The production cut just weeks after the Federal Reserve signaled a dramatically slower pace of future rate cuts in the face of a banking crisis. Because energy prices are a key input to inflation, it makes the Fed balancing the tightrope between fighting inflation and not causing more bank crises that much harder.

Oil Stocks On The Move

Oil exploration & production (E&P) names are up significantly this morning, with the SPDR S&P Oil & Gas Exploration & Production ETF (NYSE: XOP) up 3.1%, while energy stocks in general, represented by the SPDR Select Energy ETF (NYSE: XLE) is up 4%.

Major oil producers like ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX) are up 5.65% and 3.9%, respectively. Meanwhile, E&P pure plays like Marathon Oil (NYSE: MRO) and ConocoPhillips (NYSE: COP) are up about 8% each.

If this production cut starts a new bull market in oil prices, we will likely see considerable repositioning in energy equities. Midstream and downstream names like tankers, oil services, and refiners have been significantly outperforming E&Ps over the last year due to the downtrend in crude oil prices. If an uptrend in oil begins, we're likely to see investors shift into E&Ps as they have the most leveraged exposure to oil spot prices.

Traders are selling tankers and refiners this morning, two energy trades that have worked best during the downtrend in oil prices. Large tanker firms like Scorpio Tankers (NYSE: STNG) and Teekay Tankers (NYSE: TNK) fell 4% and 10%, respectively. Large refiners like Marathon Petroleum (NYSE: MPC) and Valero Energy (NYSE: VLO) are selling off modestly, about 1% each.

The End of the Oil Bear Market?

Despite crude oil being a favorite trade of inflation bulls, it failed to continue its run following the blow-off top in March 2022, settling into a treacherous downtrend starting last summer. Crude currently sits at a critical resistance level of $80. Price action around this level will answer whether the bear market is over or if this is just an overcorrection created by short-covering.

The underperformance in crude oil over the last year had disappointed many as it looked like many fundamental factors set it up for a major bull run, even before the Russia and Ukraine war began.

The most consequential factor is the underinvestment in the industry. The flight of capital following the shale boom & bust and the rise of ESG directing energy industry capital into renewables has ensured oil & gas is starving for capital. And the remaining capital invested into the sector demands returns to shareholders in the form of buybacks and dividends in favor of investment into new production.

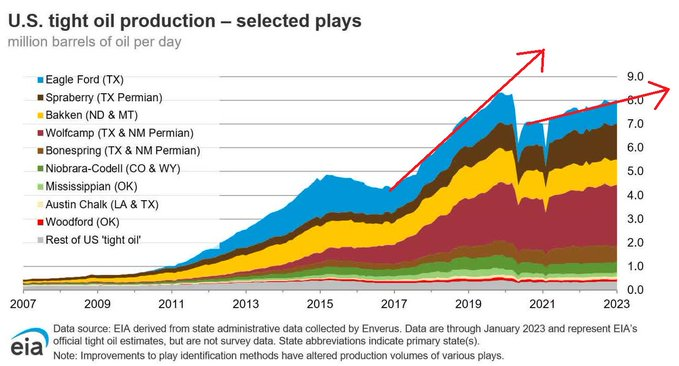

This underinvestment means that the US oil industry isn't digging new wells at the rate it used to, especially post-COVID. Below is a chart from the US Energy Information Association detailing US oil production in specific regions:

For this reason, the industry is very tight, and many assumed this alone would buoy oil prices for the next several years. However, as is usual with commodities, higher prices hurt demand, and higher prices reveal spare capacity the market didn't know about. This and the unusually warm winter put downward pressure on energy prices. If the winter would have been unusually cold, many were calling for an upward squeeze in energy prices, especially in Europe.

The Counter Point

A popular saying goes something like "the cure for high prices is high prices." In other words, people consume less oil when it's expensive, eventually driving down prices. It works in the opposite direction as well.

This is especially true as the global economy is on shaky ground. While the US consumer has been abnormally strong despite expectations otherwise, there are indications that the global economy is contracting.

For instance, this morning, China and Vietnam, key manufacturing hubs and net oil importers, reported worse-than-expected PMI readings. Because China's reopening is a key input to the oil bull thesis, traders should closely watch China's manufacturing recovery.