NVR has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 9.3% to $8,176 per share while the index has gained 7.9%.

Is there a buying opportunity in NVR, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.We're swiping left on NVR for now. Here are three reasons why you should be careful with NVR and a stock we'd rather own.

Why Is NVR Not Exciting?

Known for its unique land acquisition strategy, NVR (NYSE: NVR) is a respected homebuilder and mortgage company in the United States.

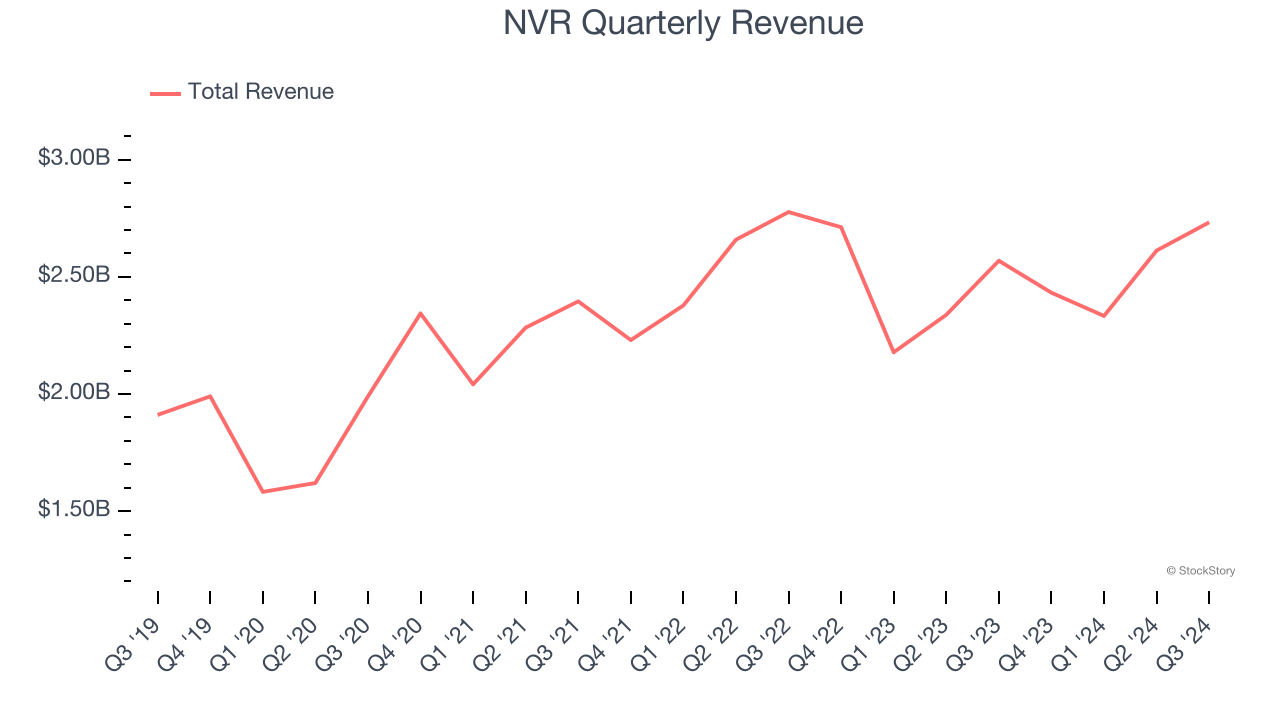

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Over the last five years, NVR grew its sales at a mediocre 6.5% compounded annual growth rate. This fell short of our benchmark for the industrials sector.

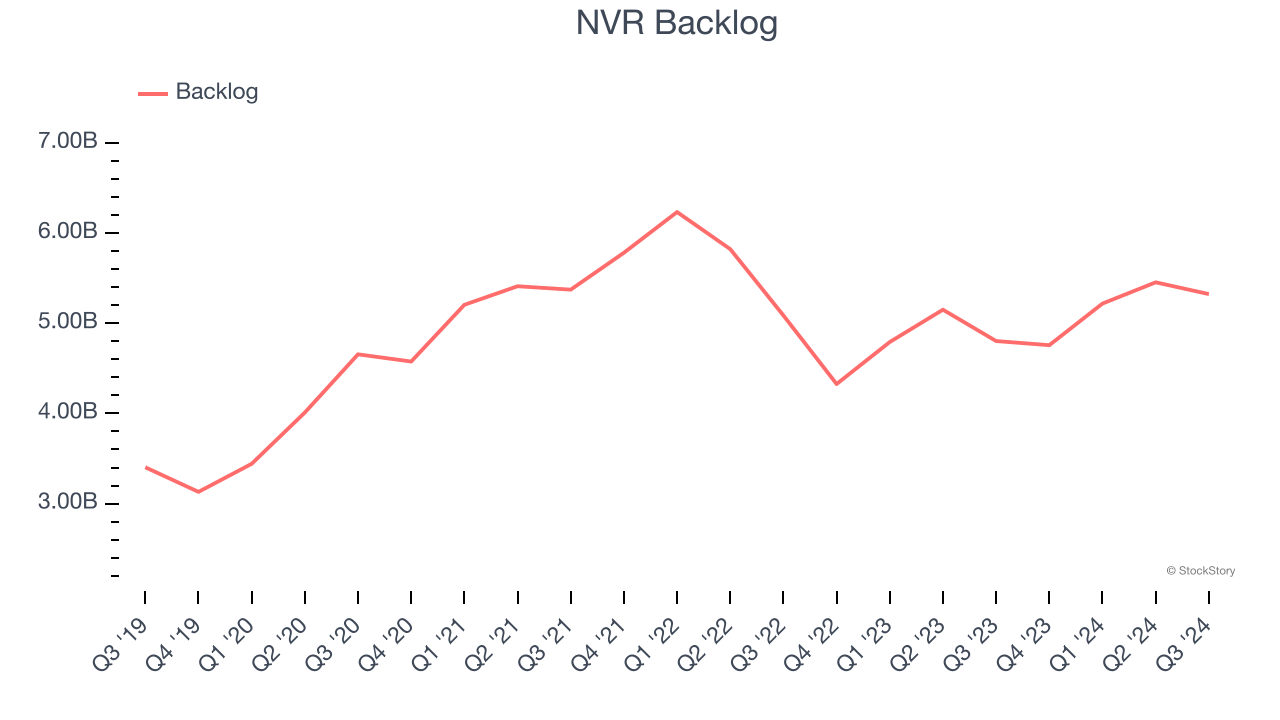

2. Backlog Declines as Orders Drop

We can better understand Home Builders companies by analyzing their backlog. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into NVR’s future revenue streams.

NVR’s backlog came in at $5.32 billion in the latest quarter, and it averaged 3.7% year-on-year declines over the last two years. This performance was underwhelming and shows the company is not winning new orders. It also suggests there may be increasing competition or market saturation.

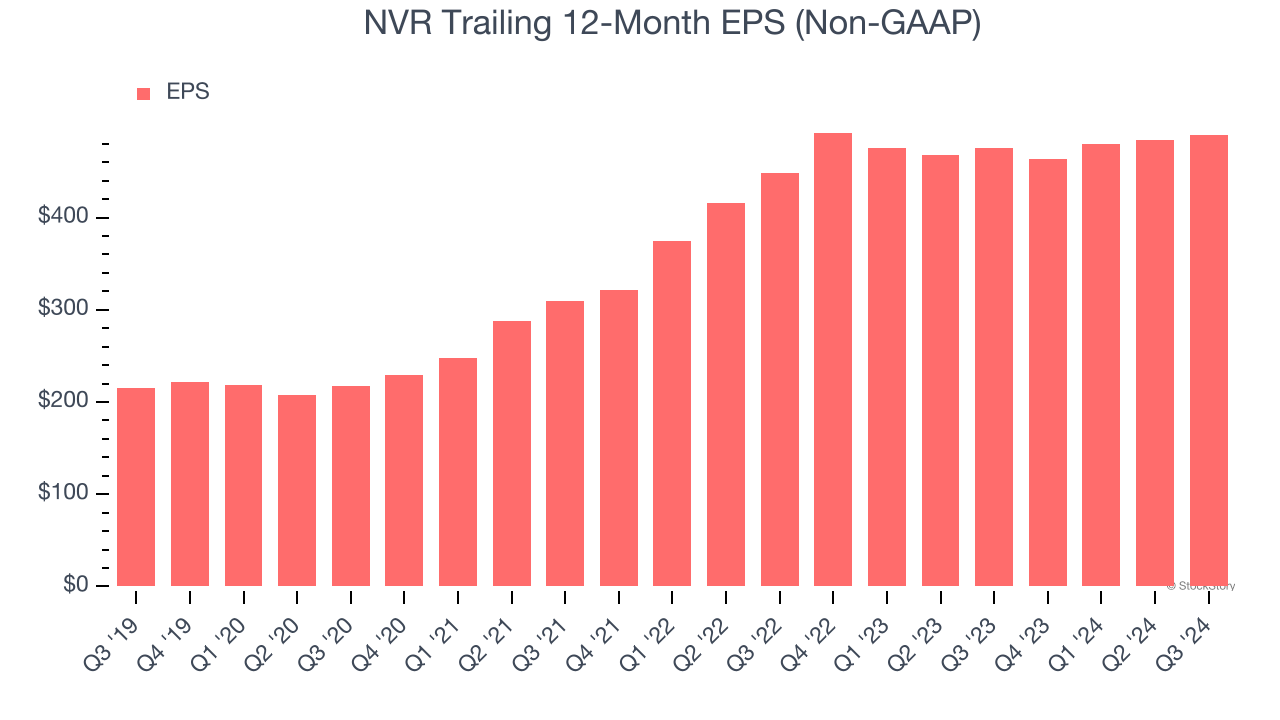

3. Recent EPS Growth Below Our Standards

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

NVR’s EPS grew at an unimpressive 4.5% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its flat revenue and tells us management responded to softer demand by adapting its cost structure.

Final Judgment

NVR isn’t a terrible business, but it isn’t one of our picks. That said, the stock currently trades at 16.1× forward price-to-earnings (or $8,176 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. Let us point you toward Cloudflare, one of our top software picks that could be a home run with edge computing.

Stocks We Like More Than NVR

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.