What a fantastic six months it’s been for Bloom Energy. Shares of the company have skyrocketed 96.5%, hitting $24.38. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Bloom Energy, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.Despite the momentum, we don't have much confidence in Bloom Energy. Here are three reasons why we avoid BE and a stock we'd rather own.

Why Is Bloom Energy Not Exciting?

Working in stealth mode for eight years, Bloom Energy (NYSE: BE) designs, manufactures, and markets solid oxide fuel cell systems for on-site power generation.

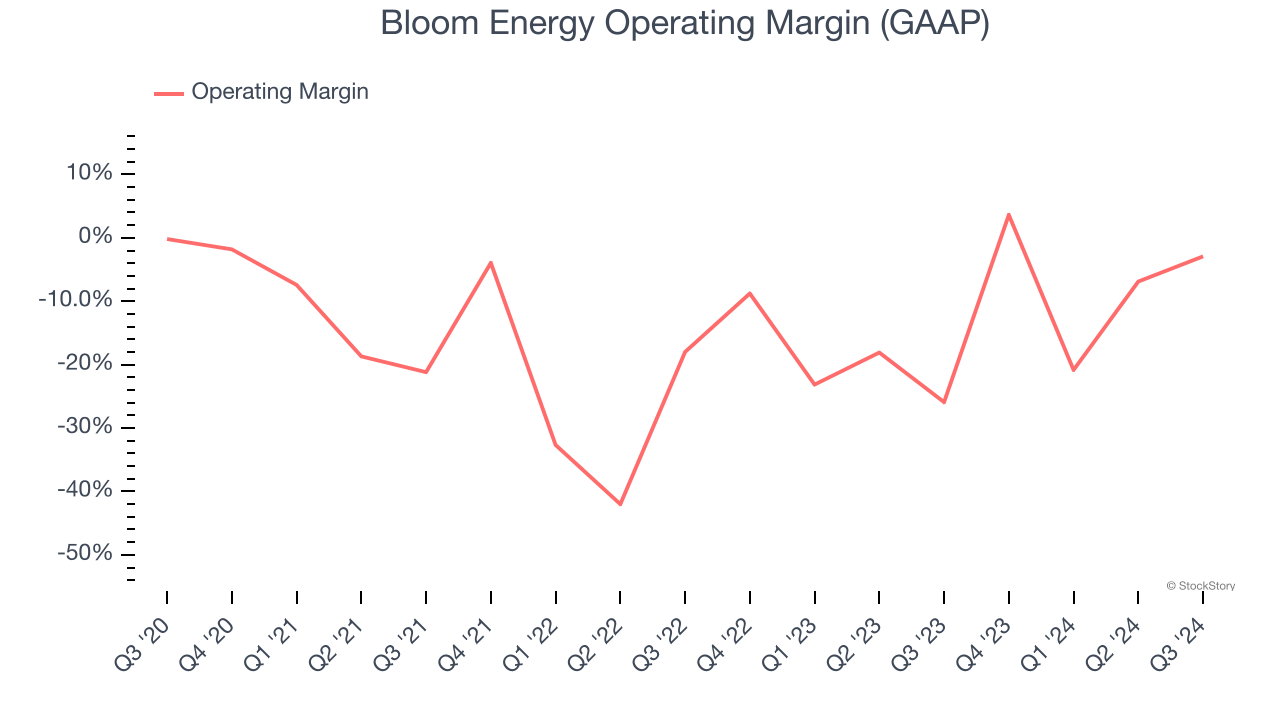

1. Operating Losses Sound the Alarms

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Bloom Energy’s high expenses have contributed to an average operating margin of negative 14.7% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

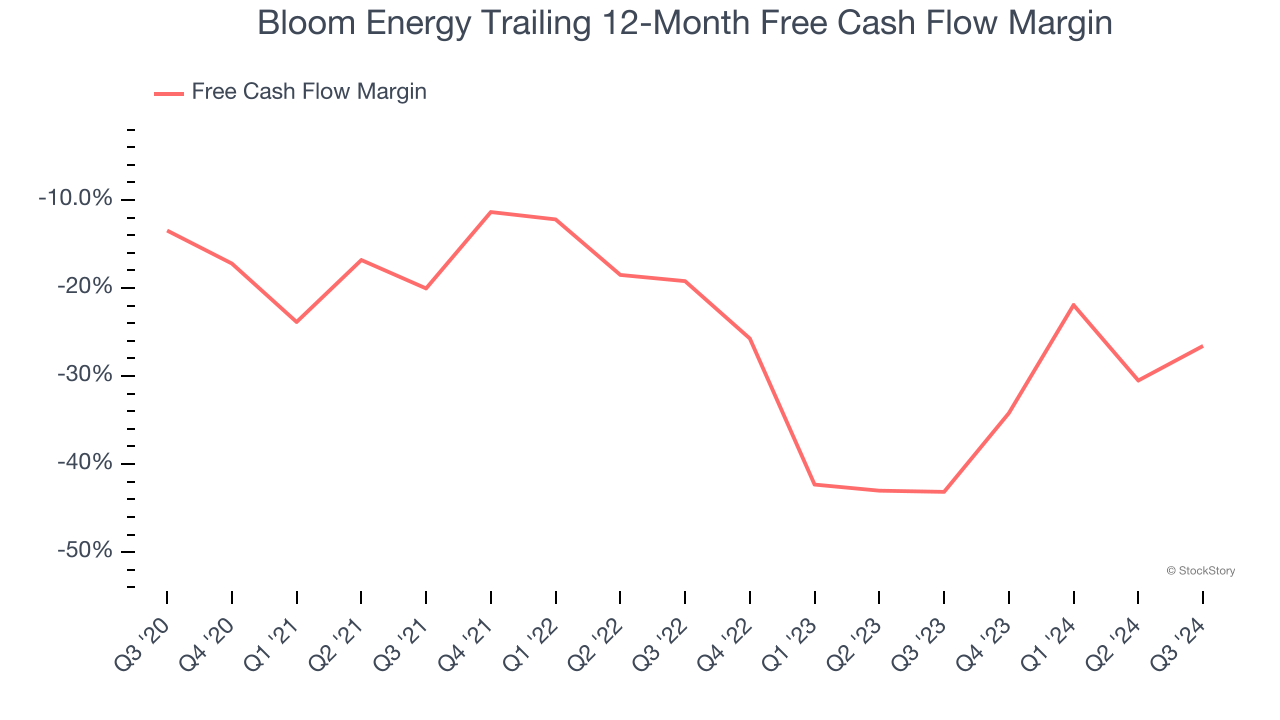

2. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Bloom Energy’s margin dropped by 13.1 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. Almost any movement in the wrong direction is undesirable because it’s already burning cash. If the longer-term trend returns, it could signal it’s becoming a more capital-intensive business. Bloom Energy’s free cash flow margin for the trailing 12 months was negative 26.6%.

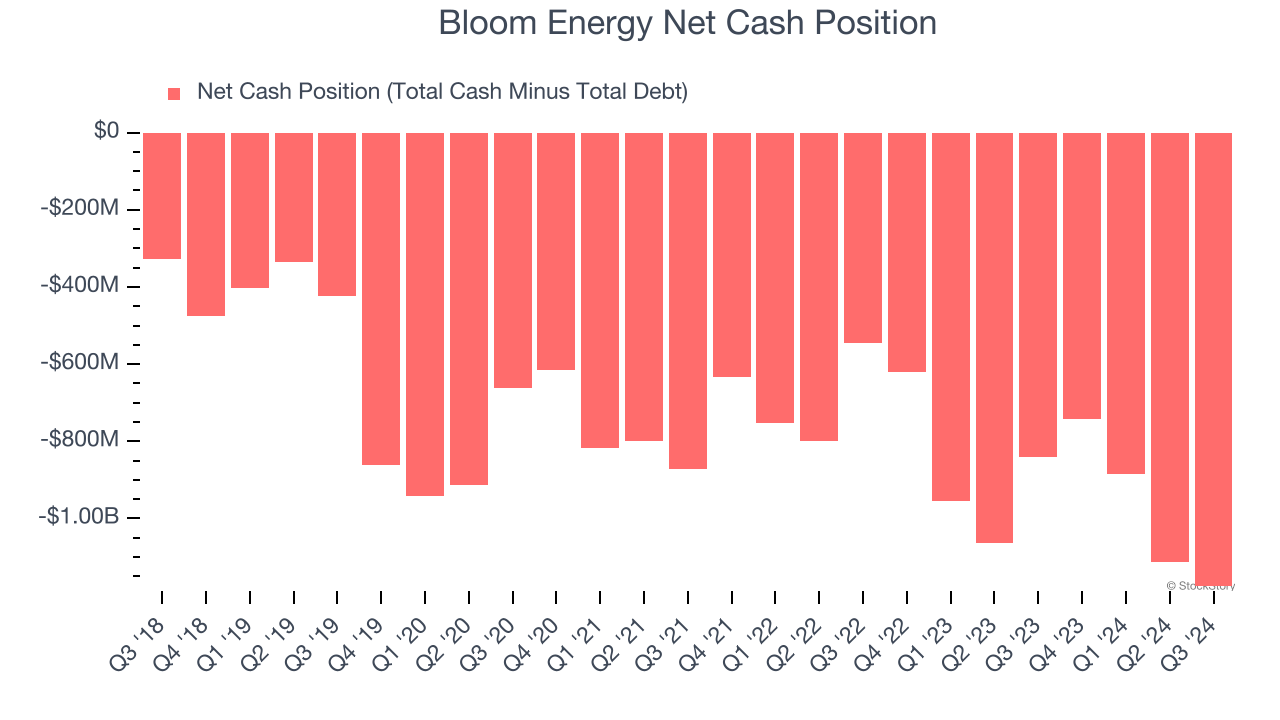

3. Short Cash Runway Exposes Shareholders to Potential Dilution

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Bloom Energy burned through $334.4 million of cash over the last year, and its $1.69 billion of debt exceeds the $518.2 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Bloom Energy’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Bloom Energy until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

Final Judgment

Bloom Energy isn’t a terrible business, but it doesn’t pass our quality test. After the recent surge, the stock trades at 68× forward price-to-earnings (or $24.38 per share). This valuation tells us a lot of optimism is priced in - we think there are better investment opportunities out there. We’d suggest looking at Chipotle, which surprisingly still has a long runway for growth.

Stocks We Would Buy Instead of Bloom Energy

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.