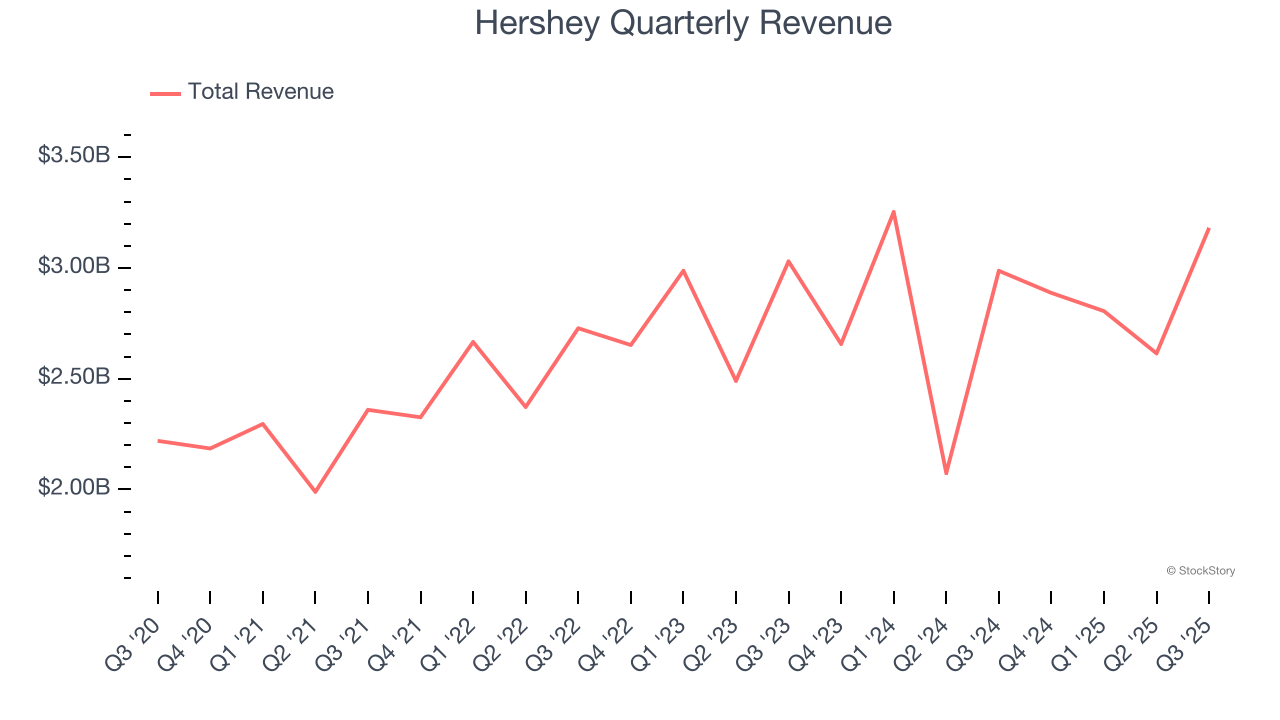

Chocolate company Hershey (NYSE: HSY) reported revenue ahead of Wall Streets expectations in Q3 CY2025, with sales up 6.5% year on year to $3.18 billion. Its non-GAAP profit of $1.30 per share was 22.2% above analysts’ consensus estimates.

Is now the time to buy Hershey? Find out by accessing our full research report, it’s free for active Edge members.

Hershey (HSY) Q3 CY2025 Highlights:

- Revenue: $3.18 billion vs analyst estimates of $3.11 billion (6.5% year-on-year growth, 2.2% beat)

- Adjusted EPS: $1.30 vs analyst estimates of $1.06 (22.2% beat)

- Adjusted EPS guidance for the full year is $5.95 at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 13.7%, down from 20.5% in the same quarter last year

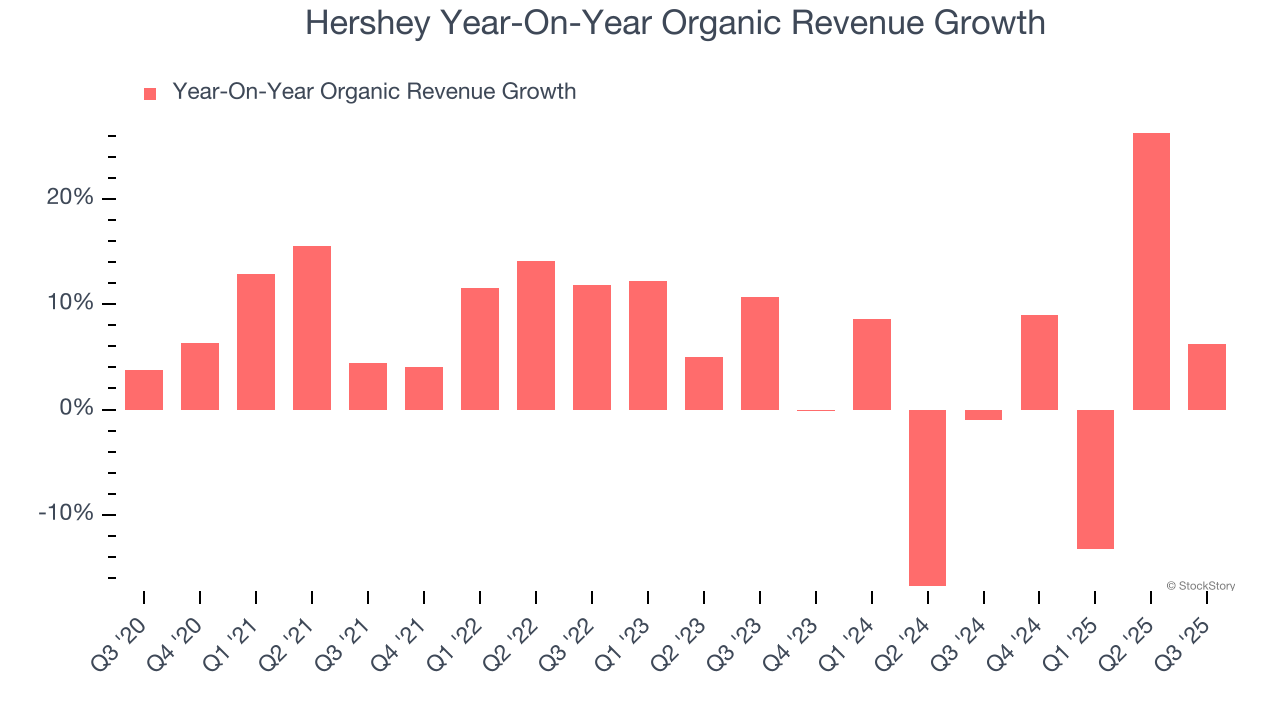

- Organic Revenue rose 6.2% year on year vs analyst estimates of 4% growth (224 basis point beat)

- Market Capitalization: $35.53 billion

"Third quarter results surpassed expectations, as strong innovation, strategic brand investments, and market leading execution drove momentum across business segments," said Kirk Tanner, The Hershey Company President and Chief Executive Officer.

Company Overview

Best known for its milk chocolate bar and Hershey's Kisses, Hershey (NYSE: HSY) is an iconic company known for its chocolate products.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years.

With $11.49 billion in revenue over the past 12 months, Hershey is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of major retail partners, placing a ceiling on its growth. To accelerate sales, Hershey likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, Hershey grew its sales at a tepid 4.4% compounded annual growth rate over the last three years as consumers bought less of its products. We’ll explore what this means in the "Volume Growth" section.

This quarter, Hershey reported year-on-year revenue growth of 6.5%, and its $3.18 billion of revenue exceeded Wall Street’s estimates by 2.2%.

Looking ahead, sell-side analysts expect revenue to grow 3.1% over the next 12 months, similar to its three-year rate. This projection is underwhelming and suggests its products will see some demand headwinds.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Hershey’s products has been stable over the last eight quarters but fell behind the broader sector. On average, the company has posted feeble year-on-year organic revenue growth of 2.4%.

In the latest quarter, Hershey’s organic sales rose by 6.2% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

Key Takeaways from Hershey’s Q3 Results

We enjoyed seeing Hershey beat analysts’ organic revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, gross margin continues to slip due to input costs. Overall, we think this quarter featured some key areas of upside versus expectations. The stock remained flat at $175 immediately after reporting.

Big picture, is Hershey a buy here and now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.