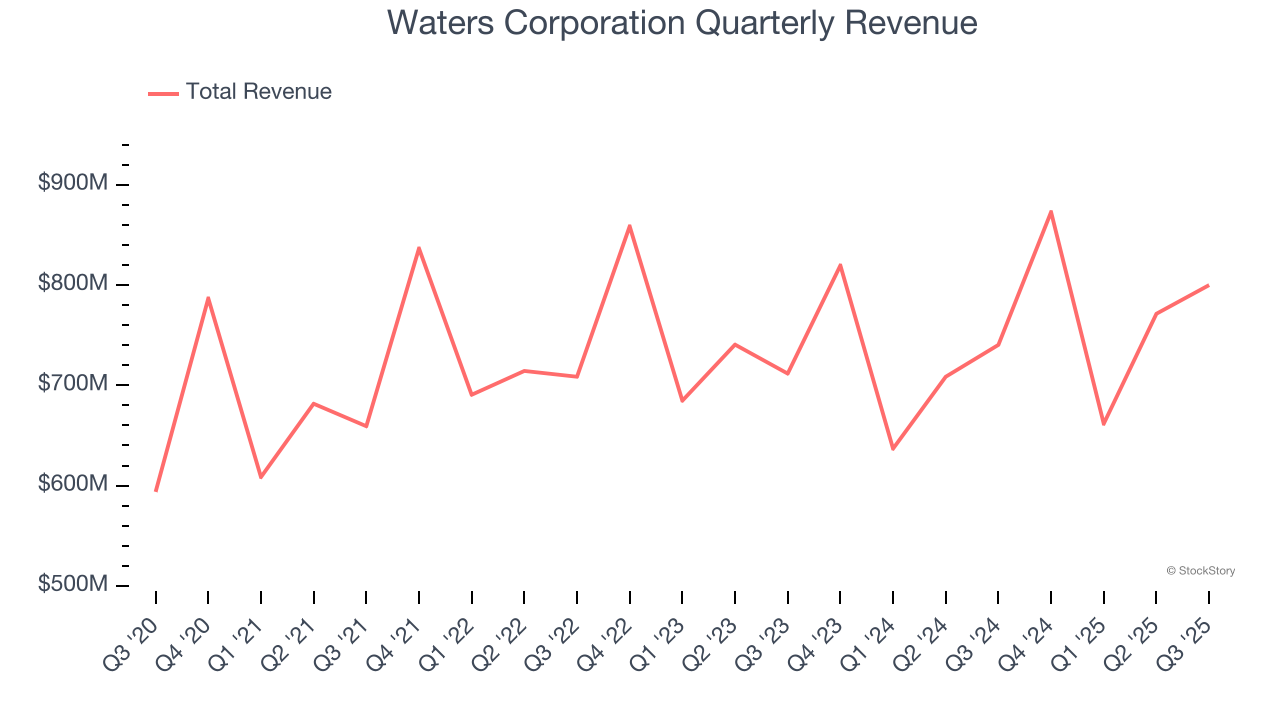

Scientific instruments company Waters Corporation (NYSE: WAT) reported Q3 CY2025 results topping the market’s revenue expectations, with sales up 8% year on year to $799.9 million. The company expects next quarter’s revenue to be around $926.8 million, close to analysts’ estimates. Its GAAP profit of $2.50 per share was 14.7% below analysts’ consensus estimates.

Is now the time to buy Waters Corporation? Find out by accessing our full research report, it’s free for active Edge members.

Waters Corporation (WAT) Q3 CY2025 Highlights:

- Revenue: $799.9 million vs analyst estimates of $781.4 million (8% year-on-year growth, 2.4% beat)

- EPS (GAAP): $2.50 vs analyst expectations of $2.93 (14.7% miss)

- Adjusted EBITDA: $258.4 million vs analyst estimates of $283.7 million (32.3% margin, 8.9% miss)

- Revenue Guidance for Q4 CY2025 is $926.8 million at the midpoint, roughly in line with what analysts were expecting

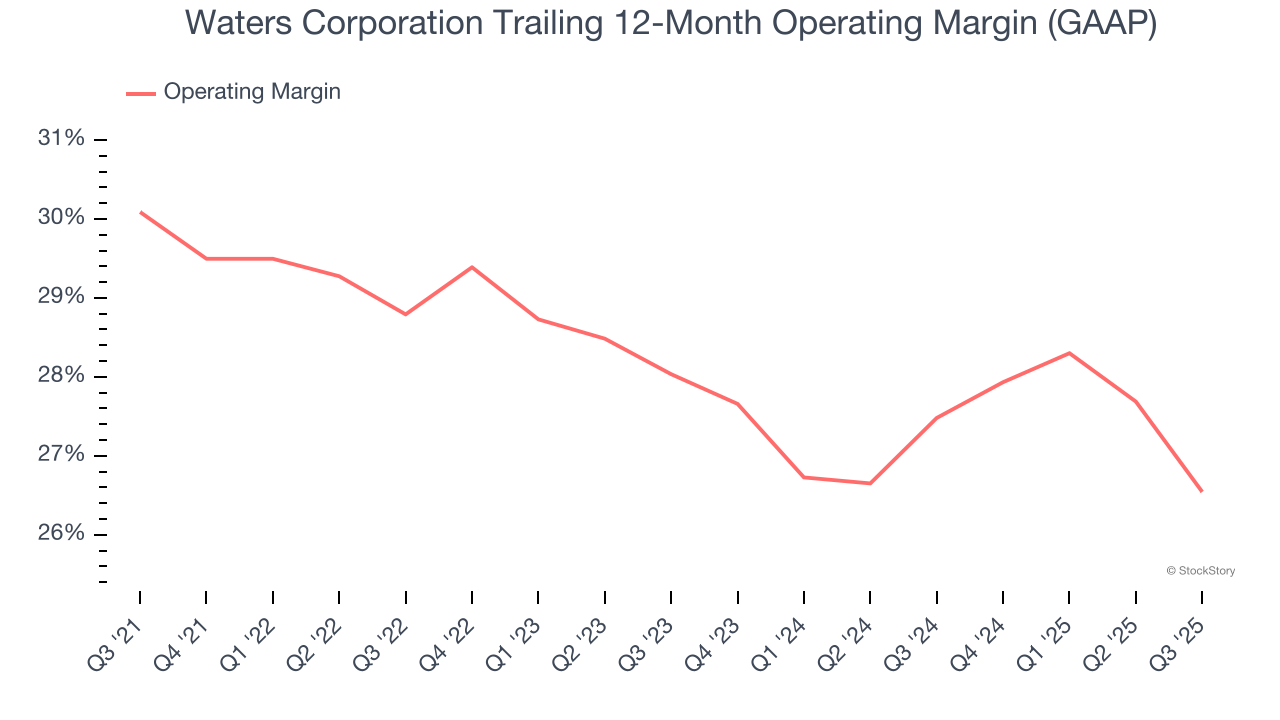

- Operating Margin: 24%, down from 28.5% in the same quarter last year

- Free Cash Flow Margin: 20.2%, down from 24.2% in the same quarter last year

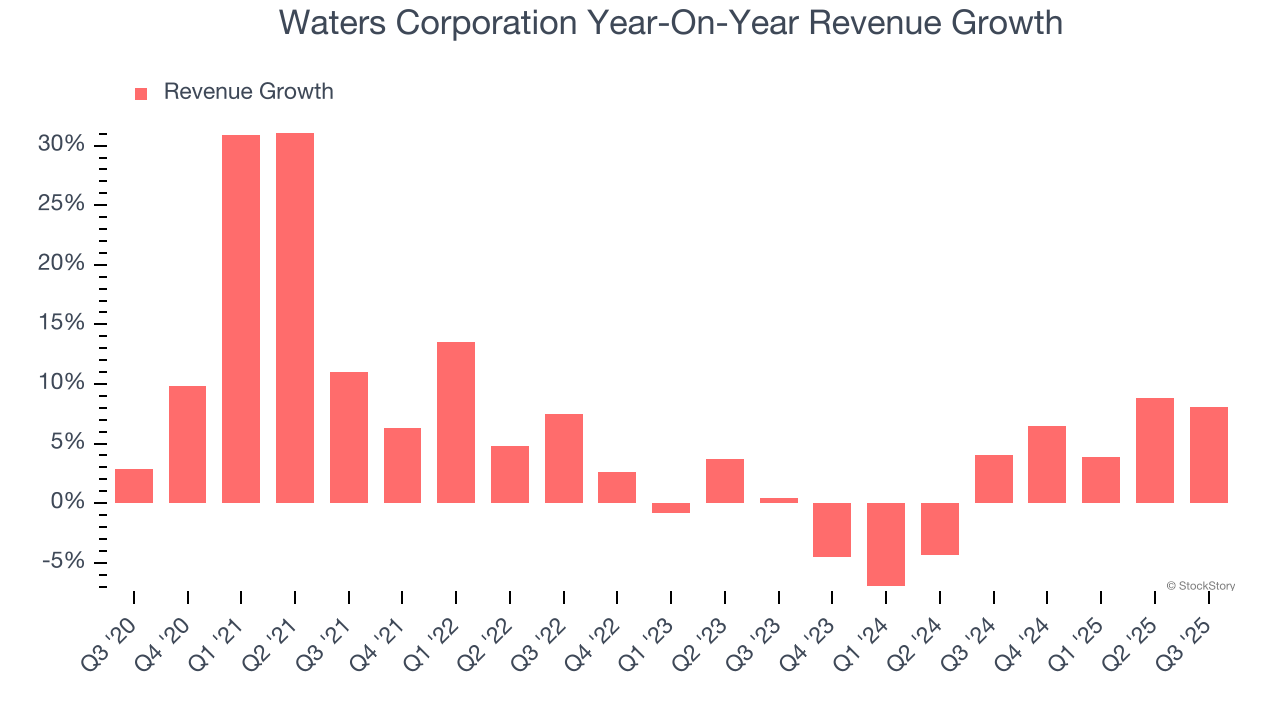

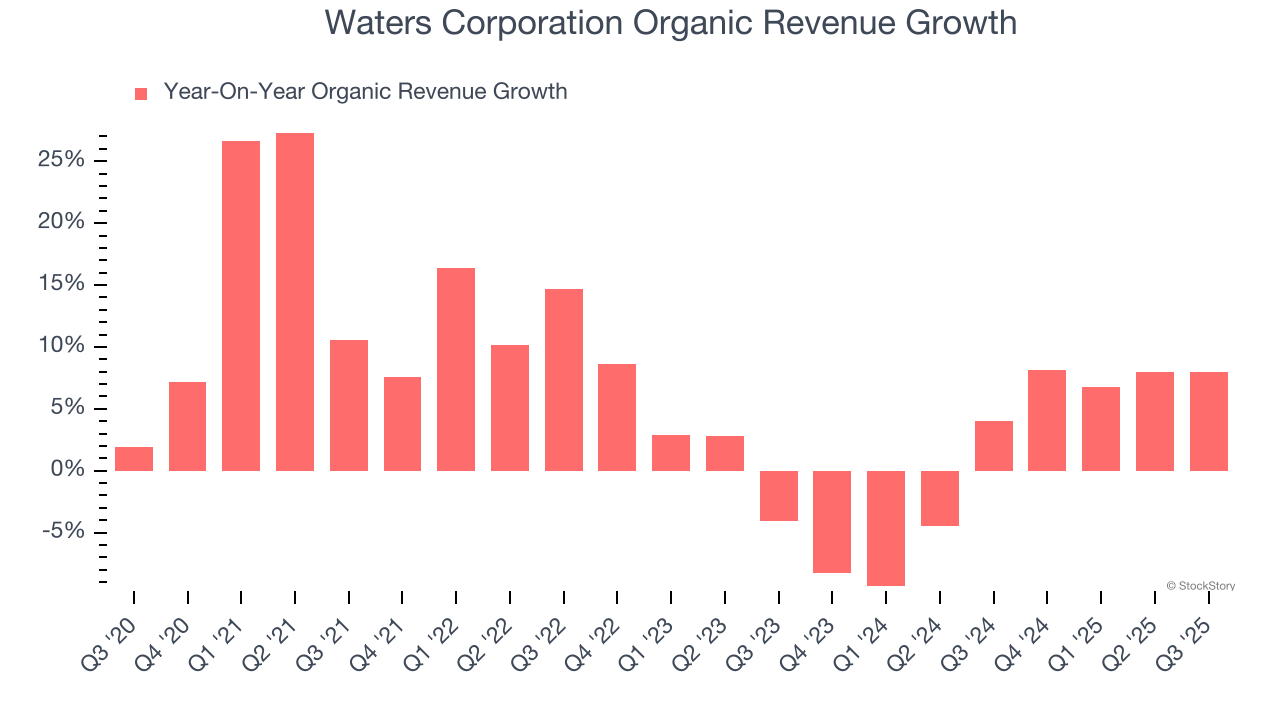

- Organic Revenue rose 8% year on year vs analyst estimates of 6% growth (200.9 basis point beat)

- Market Capitalization: $20.57 billion

"Our team yet again delivered outstanding results, driven by strong execution and our differentiated product portfolio. Pharma grew double digits as the instrument replacement cycle entered its second year, and new LC-MS and chemistry products captured opportunities from the growing share of biologics and novel modalities in the pharma pipeline," said Dr. Udit Batra, President & CEO of Waters Corporation.

Company Overview

Founded in 1958 and pioneering innovations in laboratory analysis for over six decades, Waters (NYSE: WAT) develops and manufactures analytical instruments, software, and consumables for liquid chromatography, mass spectrometry, and thermal analysis used in scientific research and quality testing.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Waters Corporation’s sales grew at a mediocre 6.2% compounded annual growth rate over the last five years. This fell short of our benchmark for the healthcare sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Waters Corporation’s recent performance shows its demand has slowed as its annualized revenue growth of 1.8% over the last two years was below its five-year trend.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Waters Corporation’s organic revenue averaged 1.6% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Waters Corporation reported year-on-year revenue growth of 8%, and its $799.9 million of revenue exceeded Wall Street’s estimates by 2.4%. Company management is currently guiding for a 6.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.8% over the next 12 months, an improvement versus the last two years. This projection is admirable and implies its newer products and services will fuel better top-line performance.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Operating Margin

Waters Corporation has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 28.1%.

Analyzing the trend in its profitability, Waters Corporation’s operating margin decreased by 3.5 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 1.5 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q3, Waters Corporation generated an operating margin profit margin of 24%, down 4.5 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

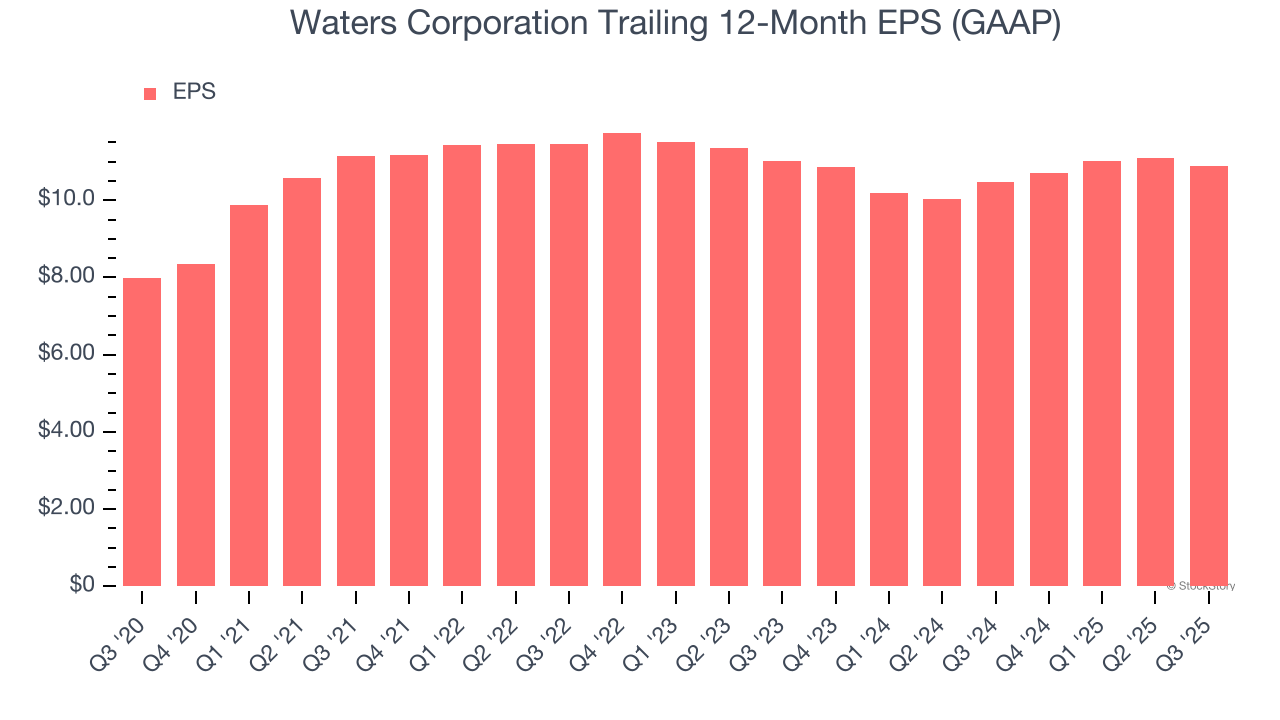

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Waters Corporation’s decent 6.4% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q3, Waters Corporation reported EPS of $2.50, down from $2.71 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Waters Corporation’s full-year EPS of $10.88 to grow 17.7%.

Key Takeaways from Waters Corporation’s Q3 Results

We enjoyed seeing Waters Corporation beat analysts’ organic revenue expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its EPS missed. Zooming out, we think this was a mixed quarter. The stock remained flat at $344.95 immediately following the results.

So should you invest in Waters Corporation right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.