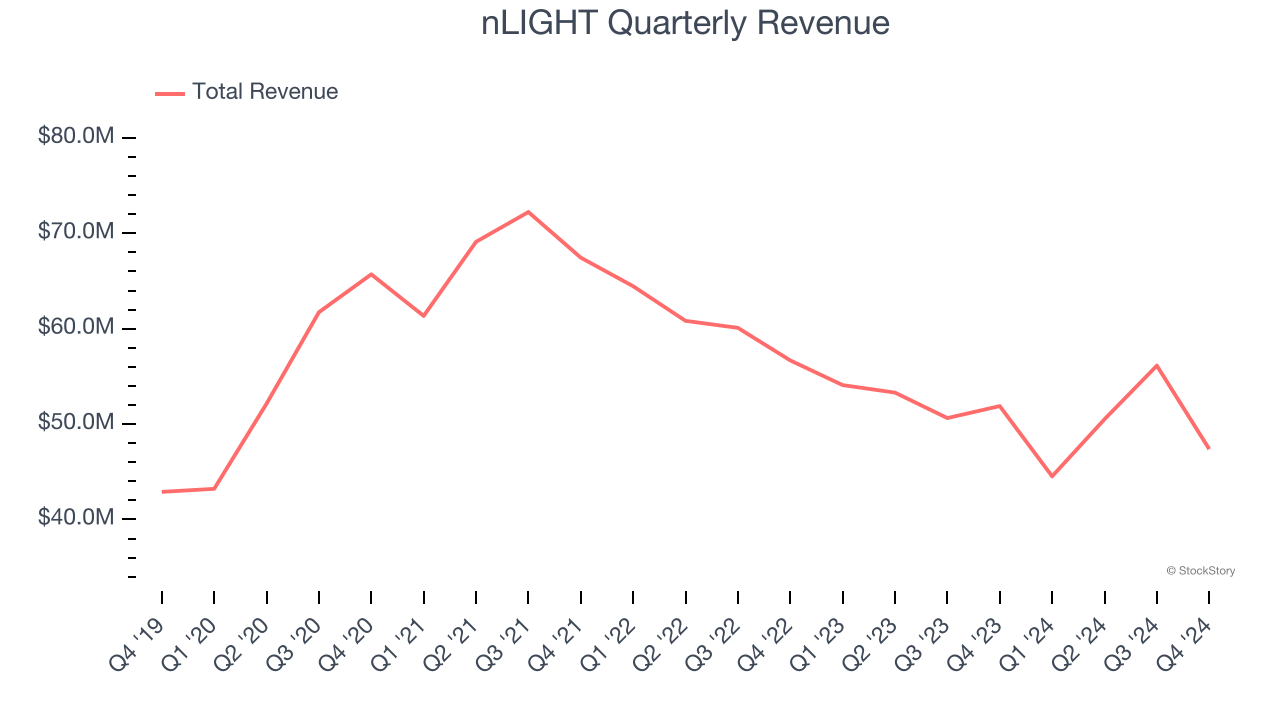

Laser company nLIGHT (NASDAQ: LASR) missed Wall Street’s revenue expectations in Q4 CY2024, with sales falling 8.7% year on year to $47.38 million. On the other hand, the company expects next quarter’s revenue to be around $48 million, close to analysts’ estimates. Its non-GAAP loss of $0.30 per share was 51.9% below analysts’ consensus estimates.

Is now the time to buy nLIGHT? Find out by accessing our full research report, it’s free.

nLIGHT (LASR) Q4 CY2024 Highlights:

- Revenue: $47.38 million vs analyst estimates of $49.19 million (8.7% year-on-year decline, 3.7% miss)

- Adjusted EPS: -$0.30 vs analyst expectations of -$0.20 (51.9% miss)

- Adjusted EBITDA: -$11.3 million vs analyst estimates of -$5.99 million (-23.9% margin, 88.8% miss)

- Revenue Guidance for Q1 CY2025 is $48 million at the midpoint, roughly in line with what analysts were expecting

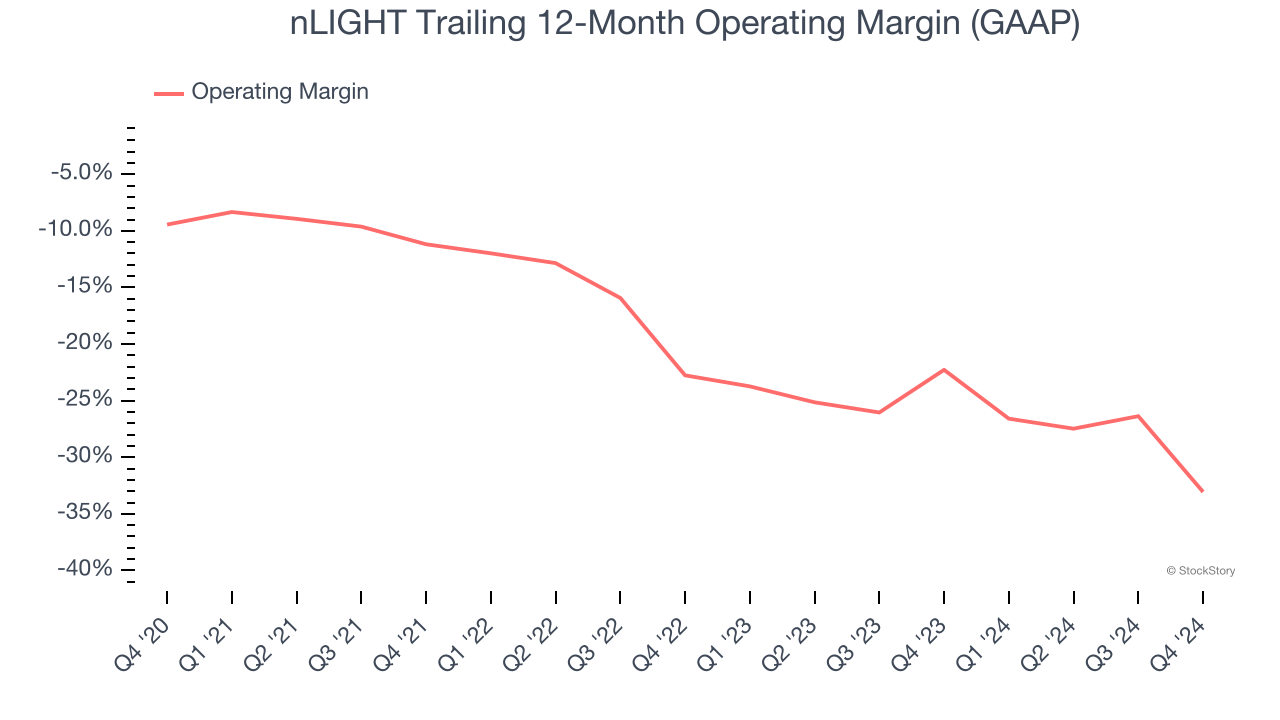

- Operating Margin: -55.8%, down from -27.6% in the same quarter last year

- Free Cash Flow was -$6.51 million compared to -$549,000 in the same quarter last year

- Market Capitalization: $476.1 million

“2024 was a transformative year for nLIGHT as our defense business began to scale, with revenue growing 20% year-over-year to $110 million and representing approximately 55% of our overall sales,” commented Scott Keeney, nLIGHT’s President and Chief Executive Officer.

Company Overview

Founded by a former CEO and Harvard-educated entrepreneur Scott Keeneyn, nLIGHT (NASDAQ: LASR) offers semiconductor and fiber lasers to the industrial, aerospace & defense, and medical sectors.

Electronic Components

Like many equipment and component manufacturers, electronic components companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include data centers and telecommunications, which can benefit companies whose optical and transceiver offerings fit those markets. But like the broader industrials sector, these companies are also at the whim of economic cycles. Consumer spending, for example, can greatly impact these companies’ volumes.

Sales Growth

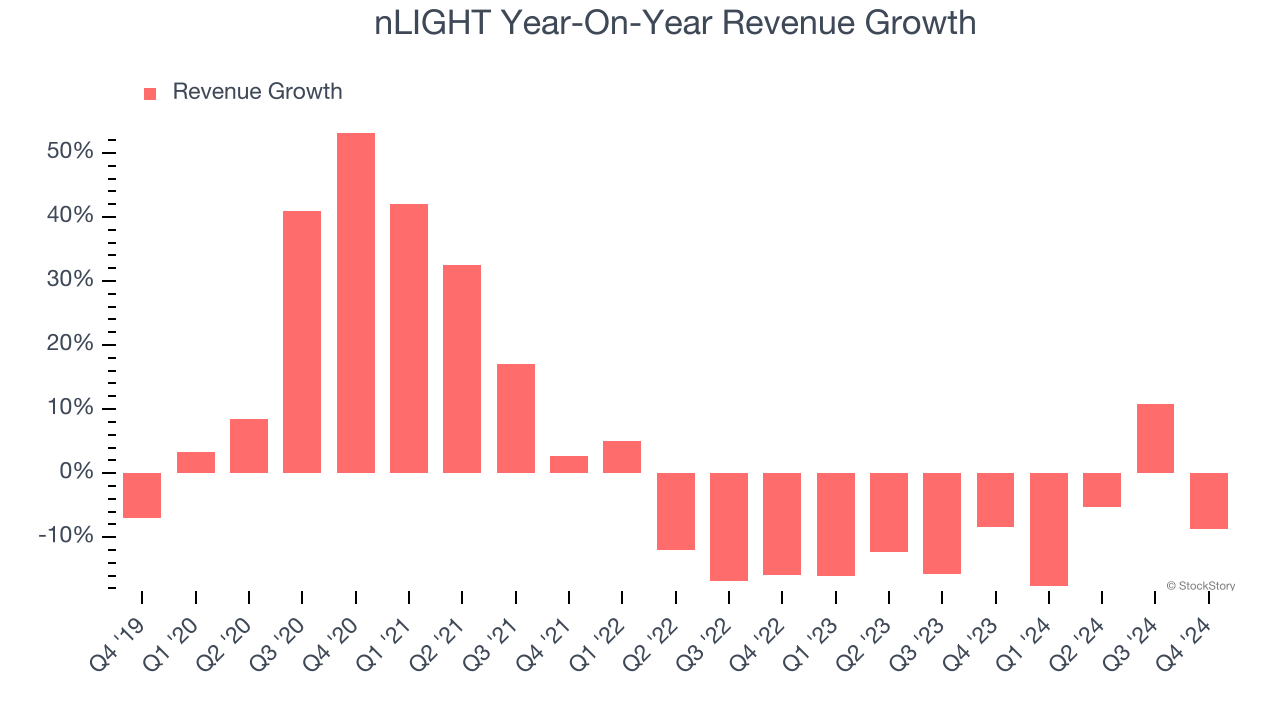

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, nLIGHT’s 2.4% annualized revenue growth over the last five years was sluggish. This was below our standards and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. nLIGHT’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 9.4% annually. nLIGHT isn’t alone in its struggles as the Electronic Components industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Laser Products and Advanced Developments, which are 66.9% and 33.1% of revenue. Over the last two years, nLIGHT’s Laser Products revenue (lasers, amplifiers, and directed energy products) averaged 15.6% year-on-year declines. On the other hand, its Advanced Developments revenue (R&D contracts) averaged 12.3% growth.

This quarter, nLIGHT missed Wall Street’s estimates and reported a rather uninspiring 8.7% year-on-year revenue decline, generating $47.38 million of revenue. Company management is currently guiding for a 7.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.1% over the next 12 months, an improvement versus the last two years. This projection is admirable and indicates its newer products and services will catalyze better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

nLIGHT’s high expenses have contributed to an average operating margin of negative 19.1% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, nLIGHT’s operating margin decreased by 23.6 percentage points over the last five years. This raises an eyebrow about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. . nLIGHT’s performance was poor no matter how you look at it - it shows costs were rising and that it couldn’t pass them onto its customers.

In Q4, nLIGHT generated a negative 55.8% operating margin. The company's consistent lack of profits raise a flag.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

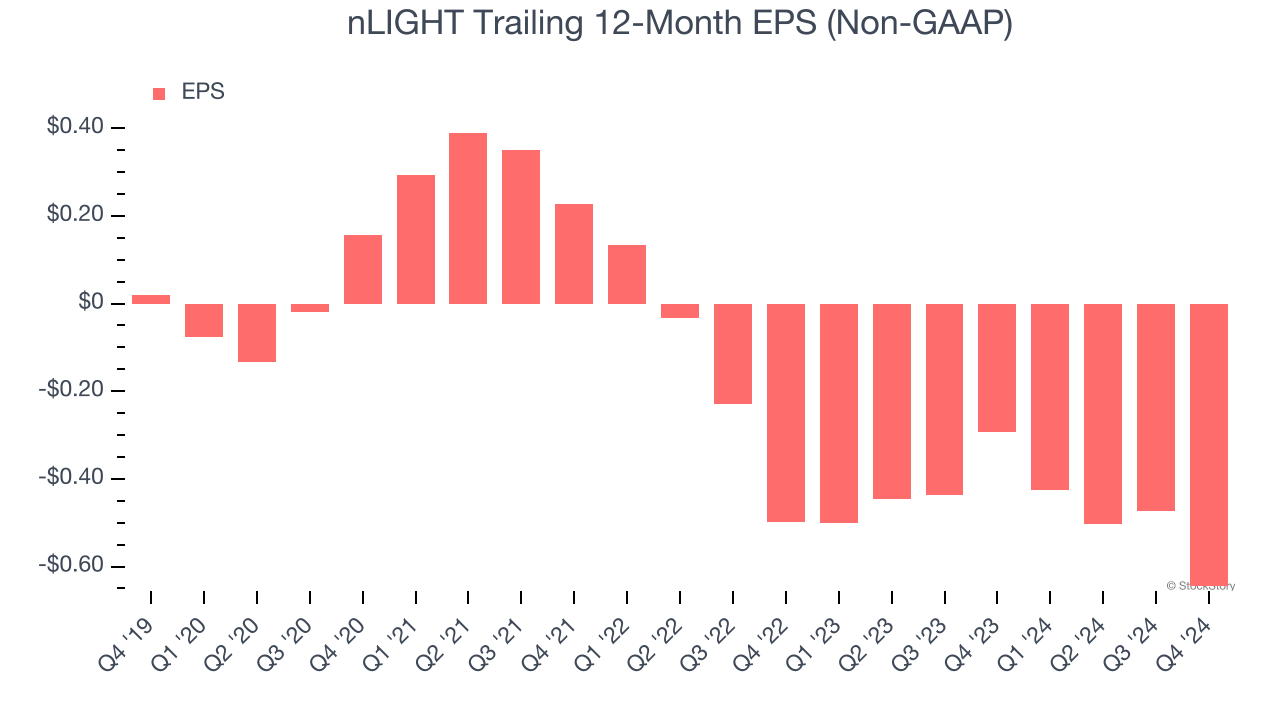

Sadly for nLIGHT, its EPS declined by 102% annually over the last five years while its revenue grew by 2.4%. This tells us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into nLIGHT’s earnings to better understand the drivers of its performance. As we mentioned earlier, nLIGHT’s operating margin declined by 23.6 percentage points over the last five years. Its share count also grew by 29.6%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For nLIGHT, its two-year annual EPS declines of 13.9% show it’s still underperforming. These results were bad no matter how you slice the data.

In Q4, nLIGHT reported EPS at negative $0.30, down from negative $0.13 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast nLIGHT’s full-year EPS of negative $0.65 will reach break even.

Key Takeaways from nLIGHT’s Q4 Results

We struggled to find many positives in these results as its revenue, EPS, and EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $9 immediately following the print.

nLIGHT didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.