Pet products provider Bark (NYSE: BARK) met Wall Street’s revenue expectations in Q4 CY2024, with sales up 1.1% year on year to $126.4 million. On the other hand, next quarter’s revenue guidance of $126.2 million was less impressive, coming in 1.9% below analysts’ estimates. Its non-GAAP loss of $0.02 per share was in line with analysts’ consensus estimates.

Is now the time to buy Bark? Find out by accessing our full research report, it’s free.

Bark (BARK) Q4 CY2024 Highlights:

- Revenue: $126.4 million vs analyst estimates of $126.4 million (1.1% year-on-year growth, in line)

- Adjusted EPS: -$0.02 vs analyst estimates of -$0.02 (in line)

- Adjusted EBITDA: -$1.56 million vs analyst estimates of -$1.57 million (-1.2% margin, relatively in line)

- Revenue Guidance for Q1 CY2025 is $126.2 million at the midpoint, below analyst estimates of $128.6 million

- EBITDA guidance for the full year is $3 million at the midpoint, below analyst estimates of $3.53 million

- Operating Margin: -9.7%, up from -11.2% in the same quarter last year

- Free Cash Flow was -$1.96 million, down from $13.26 million in the same quarter last year

- Market Capitalization: $330.5 million

"We closed 2024 on a high note, exceeding our revenue expectations and delivering our tenth consecutive year-over-year improvement in Adjusted EBITDA," said Matt Meeker, Co-Founder and Chief Executive Officer.

Company Overview

Making a name for itself with the BarkBox, Bark (NYSE: BARK) specializes in subscription-based, personalized pet products.

Toys and Electronics

The toys and electronics industry presents both opportunities and challenges for investors. Established companies often enjoy strong brand recognition and customer loyalty while smaller players can carve out a niche if they develop a viral, hit new product. The downside, however, is that success can be short-lived because the industry is very competitive: the barriers to entry for developing a new toy are low, which can lead to pricing pressures and reduced profit margins, and the rapid pace of technological advancements necessitates continuous product updates, increasing research and development costs, and shortening product life cycles for electronics companies. Furthermore, these players must navigate various regulatory requirements, especially regarding product safety, which can pose operational challenges and potential legal risks.

Sales Growth

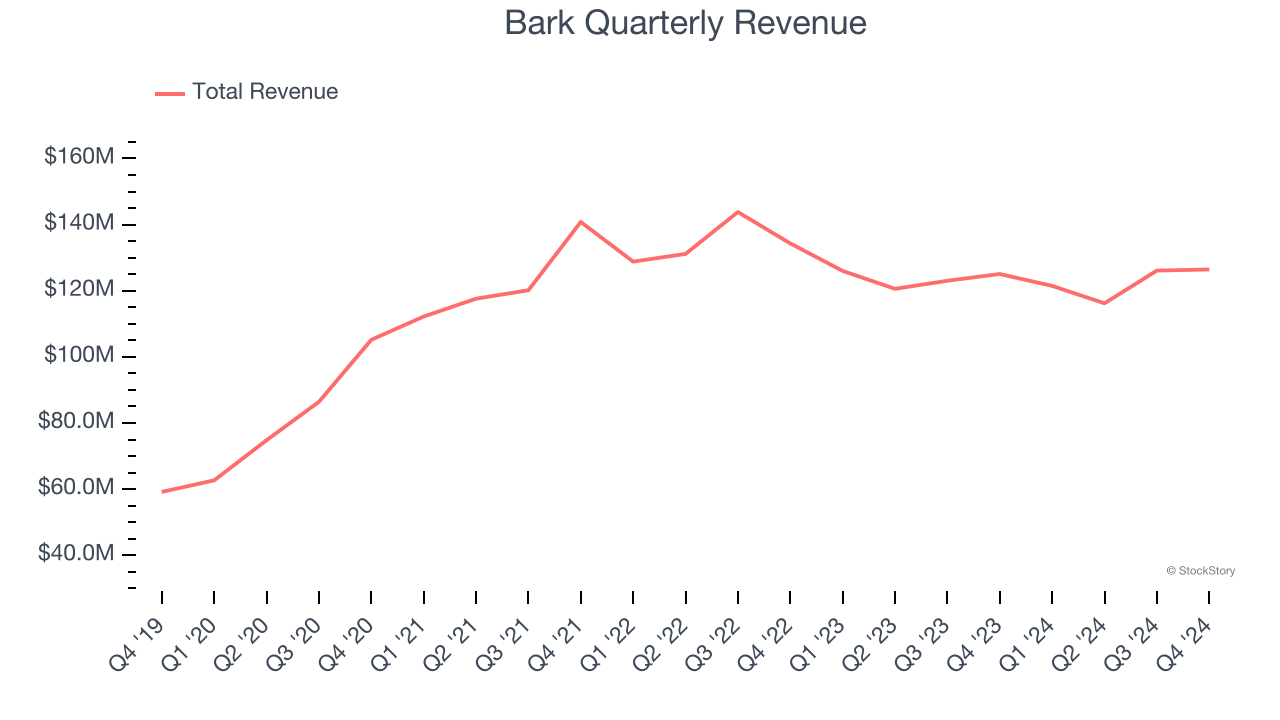

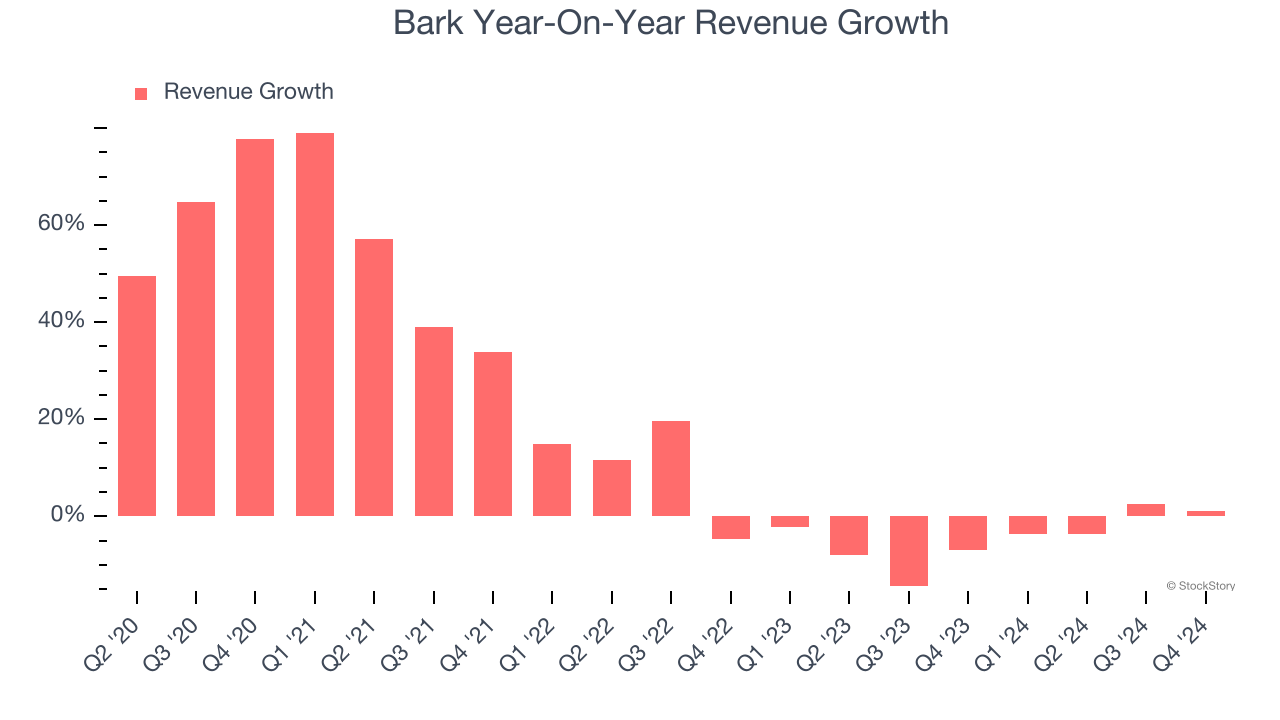

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Bark grew its sales at a decent 17.9% compounded annual growth rate. Its growth was slightly above the average consumer discretionary company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Bark’s recent history marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 4.6% over the last two years.

This quarter, Bark grew its revenue by 1.1% year on year, and its $126.4 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 3.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Cash Is King

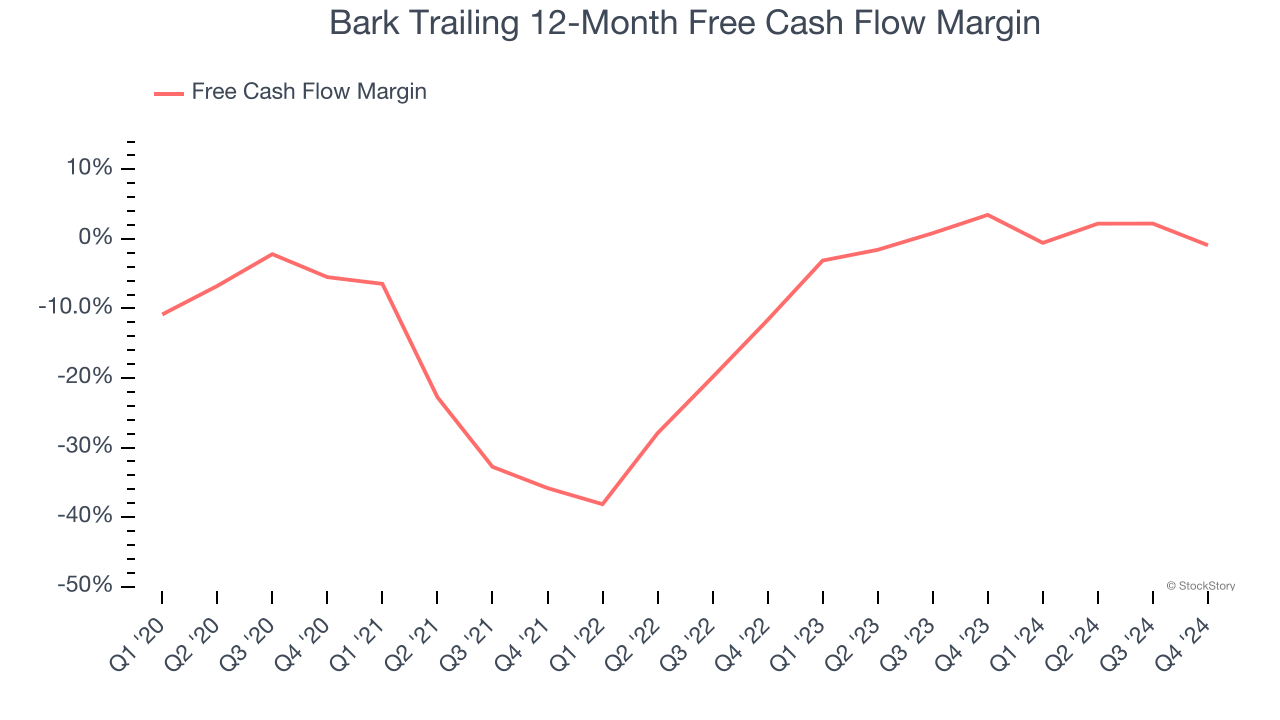

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Bark has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1.3%, lousy for a consumer discretionary business.

Bark burned through $1.96 million of cash in Q4, equivalent to a negative 1.6% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Key Takeaways from Bark’s Q4 Results

We enjoyed seeing Bark exceed analysts’ EPS expectations this quarter. On the other hand, its full-year EBITDA guidance missed significantly and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 7.9% to $1.80 immediately following the results.

Bark’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.