What a brutal six months it’s been for Varonis. The stock has dropped 25.4% and now trades at $41.11, rattling many shareholders. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Varonis, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Even though the stock has become cheaper, we're swiping left on Varonis for now. Here are three reasons why we avoid VRNS and a stock we'd rather own.

Why Is Varonis Not Exciting?

Founded by a duo of former Israeli Defense Forces cyber warfare engineers, Varonis (NASDAQ: VRNS) offers software-as-service that helps customers protect data from cyber threats and gain visibility into how enterprise data is being used.

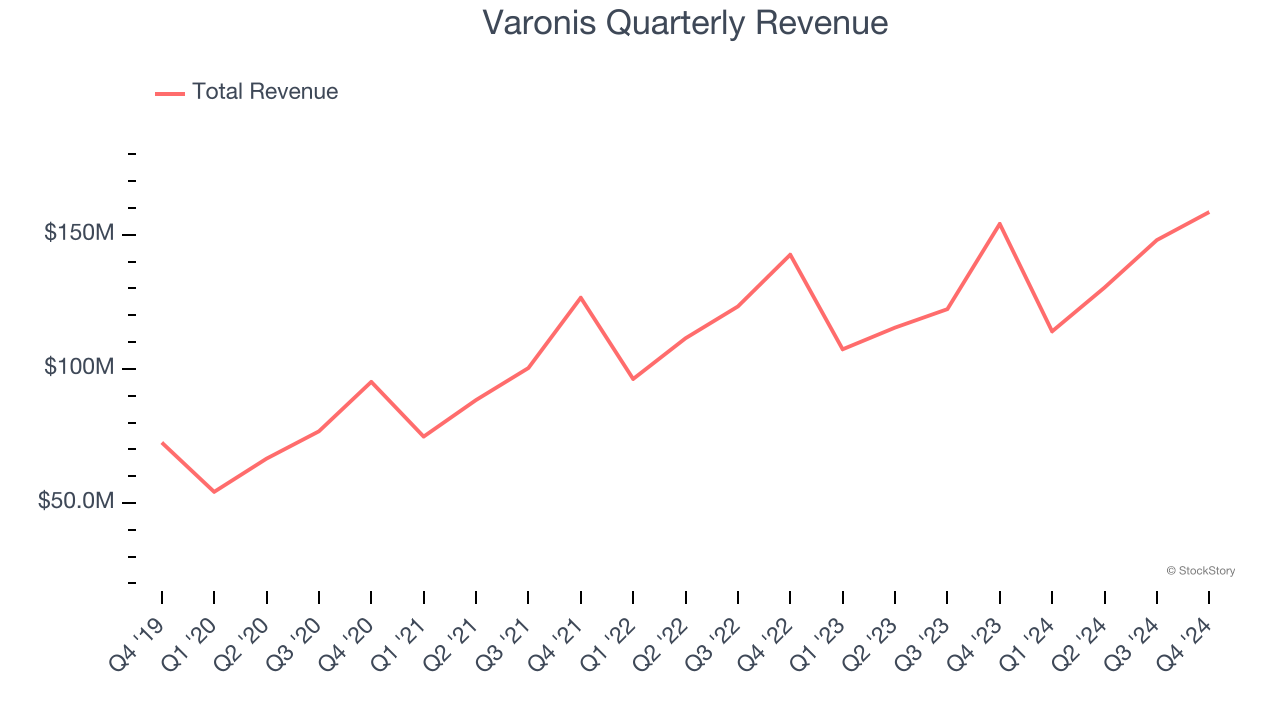

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, Varonis grew its sales at a 12.2% annual rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the software sector, which enjoys a number of secular tailwinds.

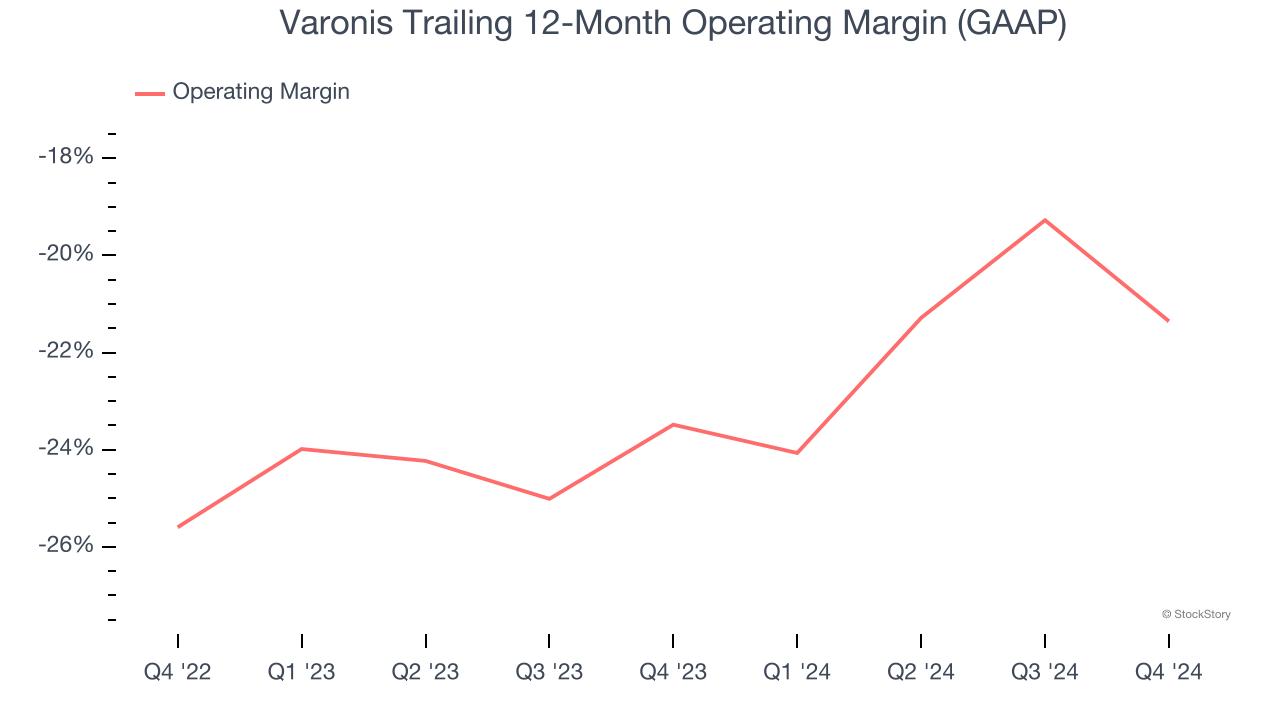

2. Operating Losses Sound the Alarms

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Varonis’s expensive cost structure has contributed to an average operating margin of negative 21.4% over the last year. Unprofitable software companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked well so far, and it’s unclear what would happen if Varonis reeled back its investments. Despite this, Wall Street seems to be optimistic about its growth prospects. We tend to have the same view.

3. High Debt Levels Increase Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Varonis’s $743.6 million of debt exceeds the $568.4 million of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $27.04 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Varonis could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Varonis can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

Varonis’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 7.5× forward price-to-sales (or $41.11 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now. Let us point you toward our favorite semiconductor picks and shovels play.

Stocks We Would Buy Instead of Varonis

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.