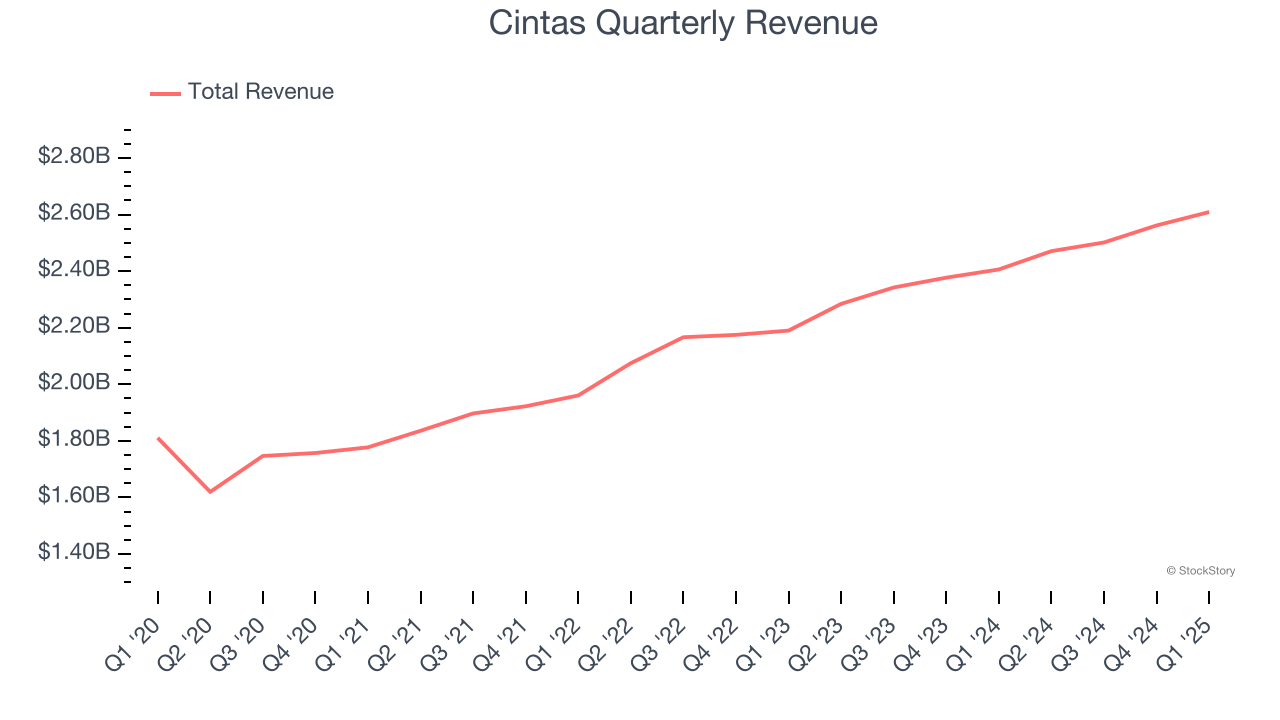

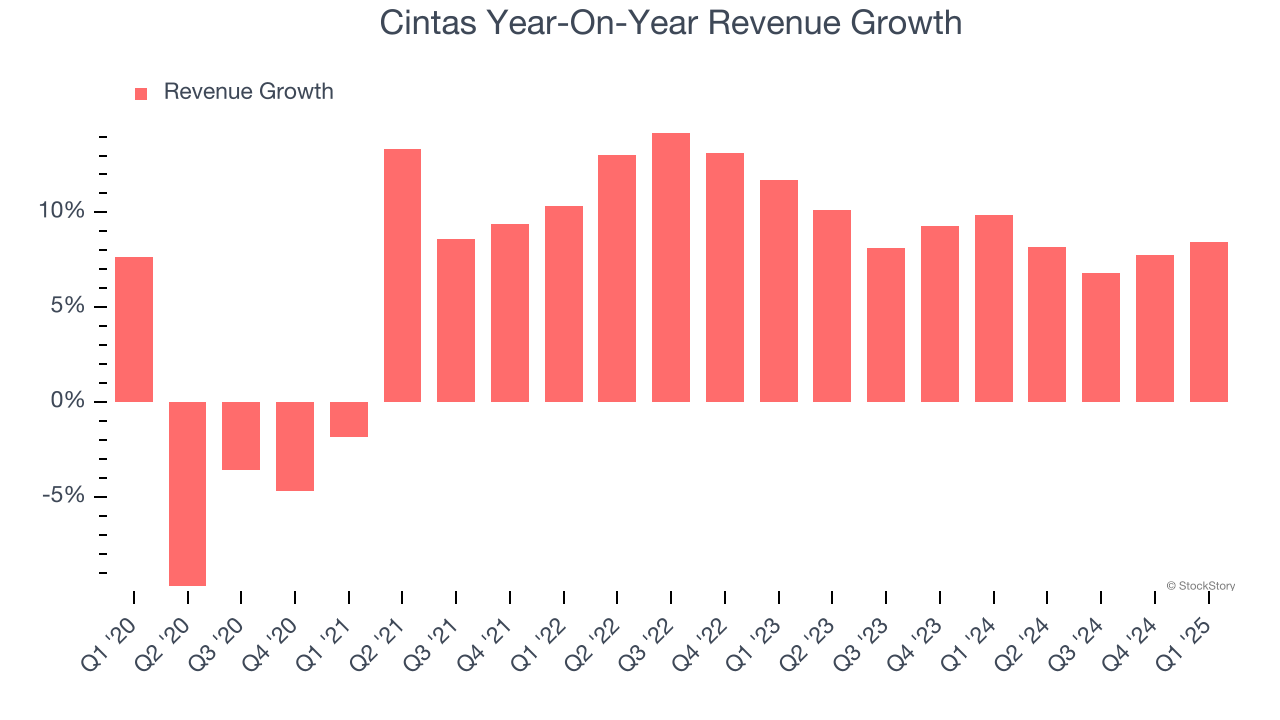

Uniform and facility services provider Cintas (NASDAQ: CTAS) met Wall Street’s revenue expectations in Q1 CY2025, with sales up 8.4% year on year to $2.61 billion. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $10.29 billion at the midpoint. Its GAAP profit of $1.13 per share was 7.1% above analysts’ consensus estimates.

Is now the time to buy Cintas? Find out by accessing our full research report, it’s free.

Cintas (CTAS) Q1 CY2025 Highlights:

- Revenue: $2.61 billion vs analyst estimates of $2.6 billion (8.4% year-on-year growth, in line)

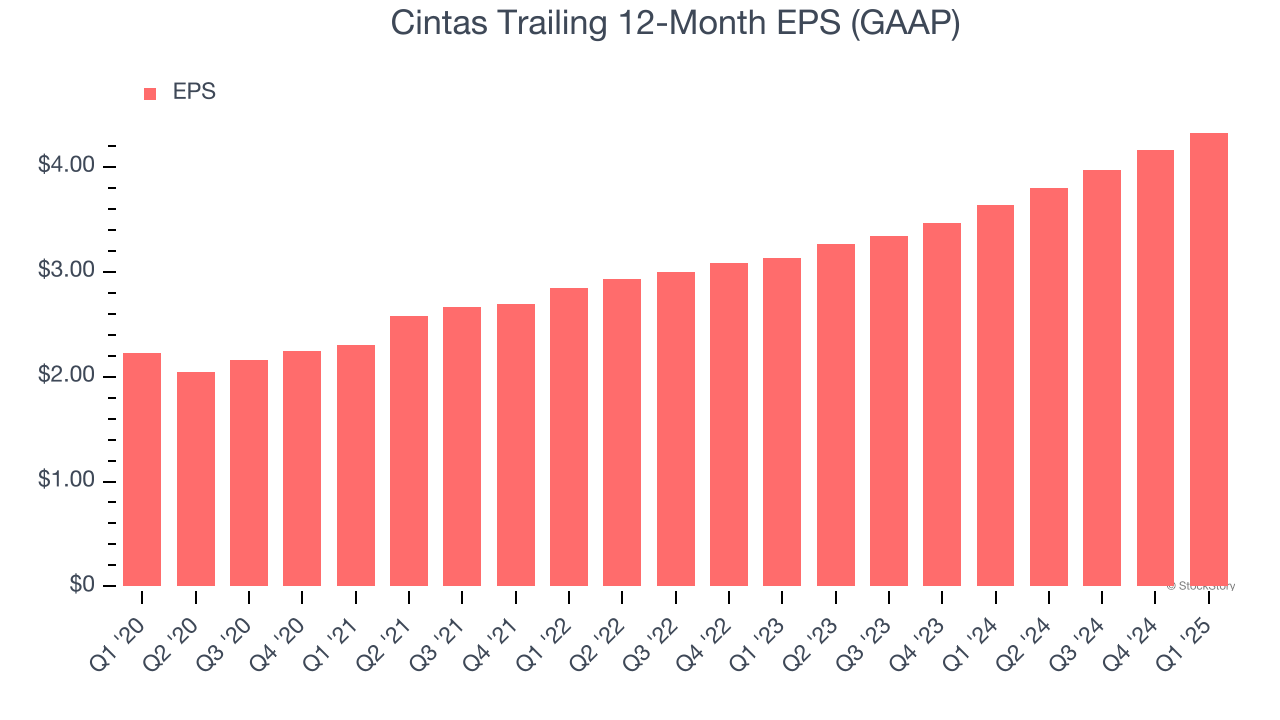

- EPS (GAAP): $1.13 vs analyst estimates of $1.06 (7.1% beat)

- The company slightly lifted its revenue guidance for the full year to $10.29 billion at the midpoint from $10.29 billion

- EPS (GAAP) guidance for the full year is $4.38 at the midpoint, beating analyst estimates by 1.3%

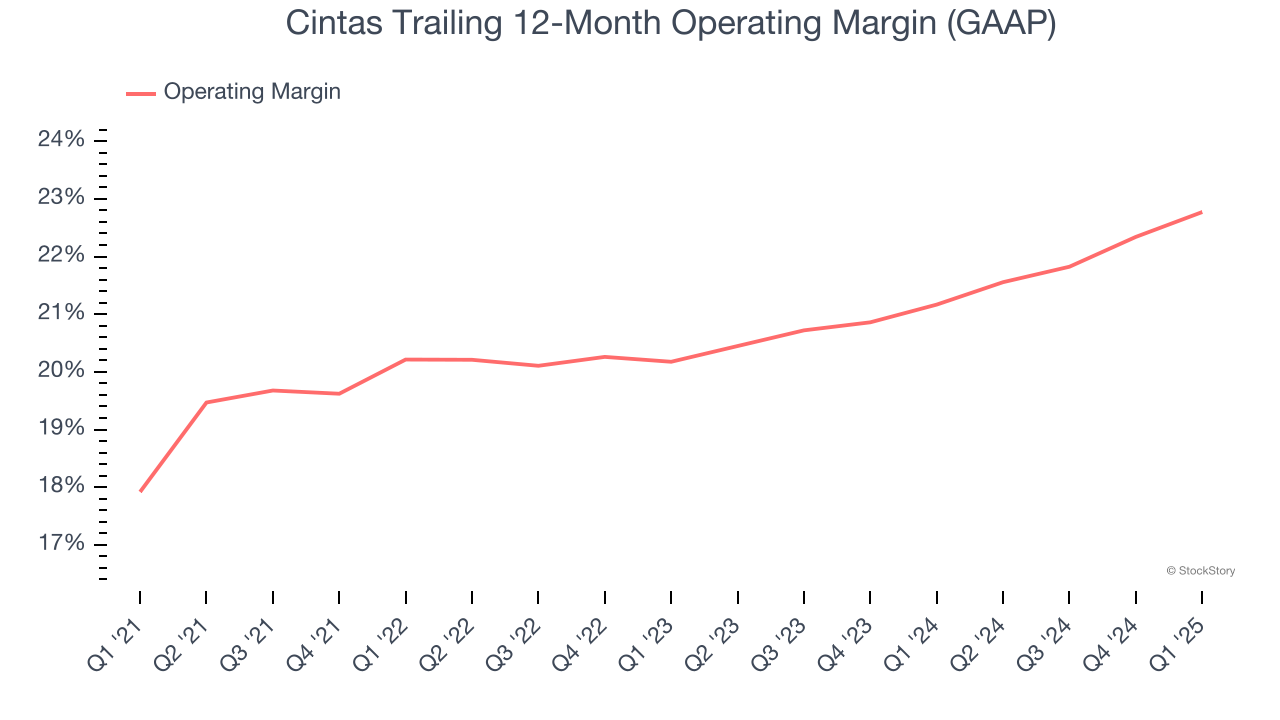

- Operating Margin: 23.4%, up from 21.6% in the same quarter last year

- Free Cash Flow Margin: 20%, down from 22.9% in the same quarter last year

- Market Capitalization: $78.07 billion

Company Overview

Starting as a family business collecting and cleaning shop rags in Cincinnati, Cintas (NASDAQ: CTAS) provides corporate identity uniforms, facility services, and safety products to over one million businesses across North America.

Industrial & Environmental Services

Growing regulatory pressure on environmental compliance and increasing corporate ESG commitments should buoy the sector for years to come. On the other hand, environmental regulations continue to evolve, and this may require costly upgrades, volatility in commodity waste and recycling markets, and labor shortages in industrial services. As for digitization, a theme that is impacting nearly every industry, the increasing use of data, analytics, and automation will give rise to improved efficiency of operations. Conversely, though, the benefits of digitization also come with challenges of integrating new technologies into legacy systems.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $10.14 billion in revenue over the past 12 months, Cintas is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

As you can see below, Cintas’s sales grew at a decent 6.9% compounded annual growth rate over the last five years. This shows its offerings generated slightly more demand than the average business services company, a helpful starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Cintas’s annualized revenue growth of 8.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Cintas grew its revenue by 8.4% year on year, and its $2.61 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6.8% over the next 12 months, a slight deceleration versus the last two years. We still think its growth trajectory is satisfactory given its scale and implies the market is forecasting success for its products and services.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Cintas has been a well-oiled machine over the last five years. It demonstrated elite profitability for a business services business, boasting an average operating margin of 20.7%.

Looking at the trend in its profitability, Cintas’s operating margin rose by 4.9 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Cintas generated an operating profit margin of 23.4%, up 1.7 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Cintas’s EPS grew at a spectacular 14.2% compounded annual growth rate over the last five years, higher than its 6.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

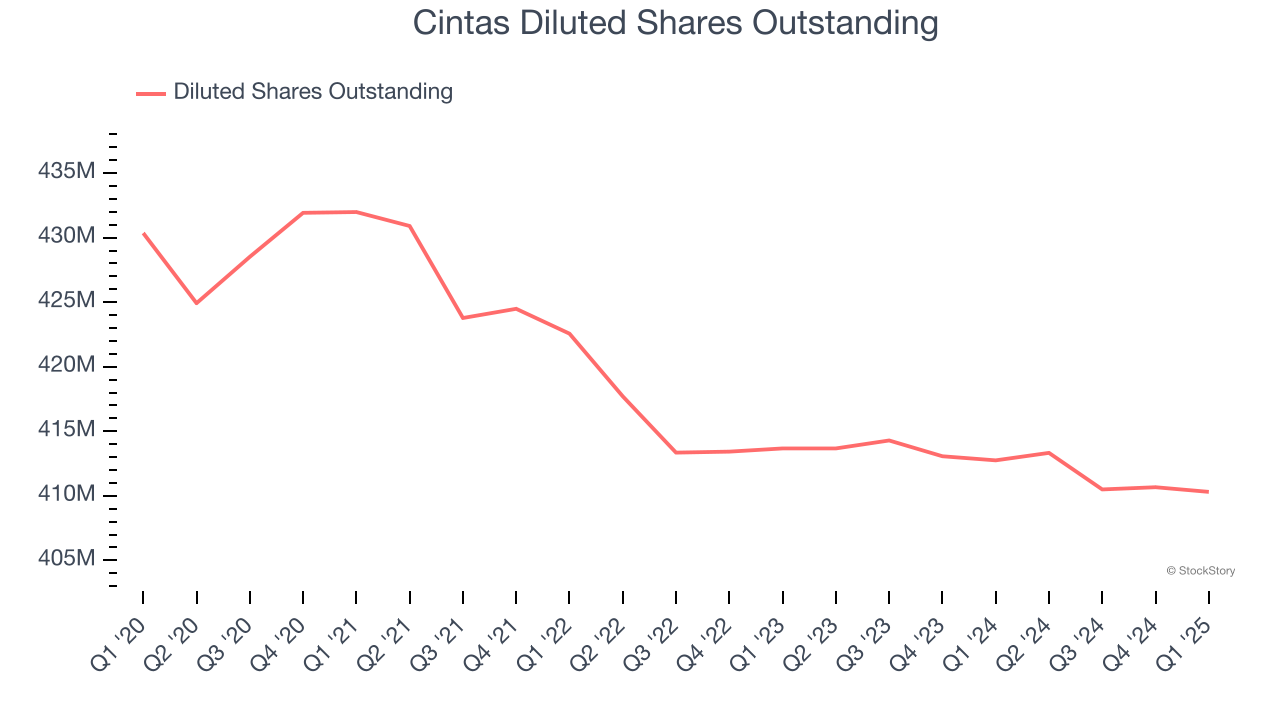

We can take a deeper look into Cintas’s earnings to better understand the drivers of its performance. As we mentioned earlier, Cintas’s operating margin expanded by 4.9 percentage points over the last five years. On top of that, its share count shrank by 4.7%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q1, Cintas reported EPS at $1.13, up from $0.96 in the same quarter last year. This print beat analysts’ estimates by 7.1%. Over the next 12 months, Wall Street expects Cintas’s full-year EPS of $4.33 to grow 7.4%.

Key Takeaways from Cintas’s Q1 Results

It was encouraging to see Cintas beat analysts’ EPS expectations this quarter. We were also happy its full-year EPS guidance narrowly outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance was in line. Overall, this quarter had some key positives. The stock traded up 4.7% to $202.66 immediately after reporting.

Should you buy the stock or not? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.