Over the last six months, Hillman shares have sunk to $8.52, producing a disappointing 19.3% loss - worse than the S&P 500’s 4.1% drop. This may have investors wondering how to approach the situation.

Is now the time to buy Hillman, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Despite the more favorable entry price, we're swiping left on Hillman for now. Here are three reasons why there are better opportunities than HLMN and a stock we'd rather own.

Why Is Hillman Not Exciting?

Established when Max Hillman purchased a franchise operation, Hillman (NASDAQ: HLMN) designs, manufactures, and sells industrial equipment and systems for various sectors.

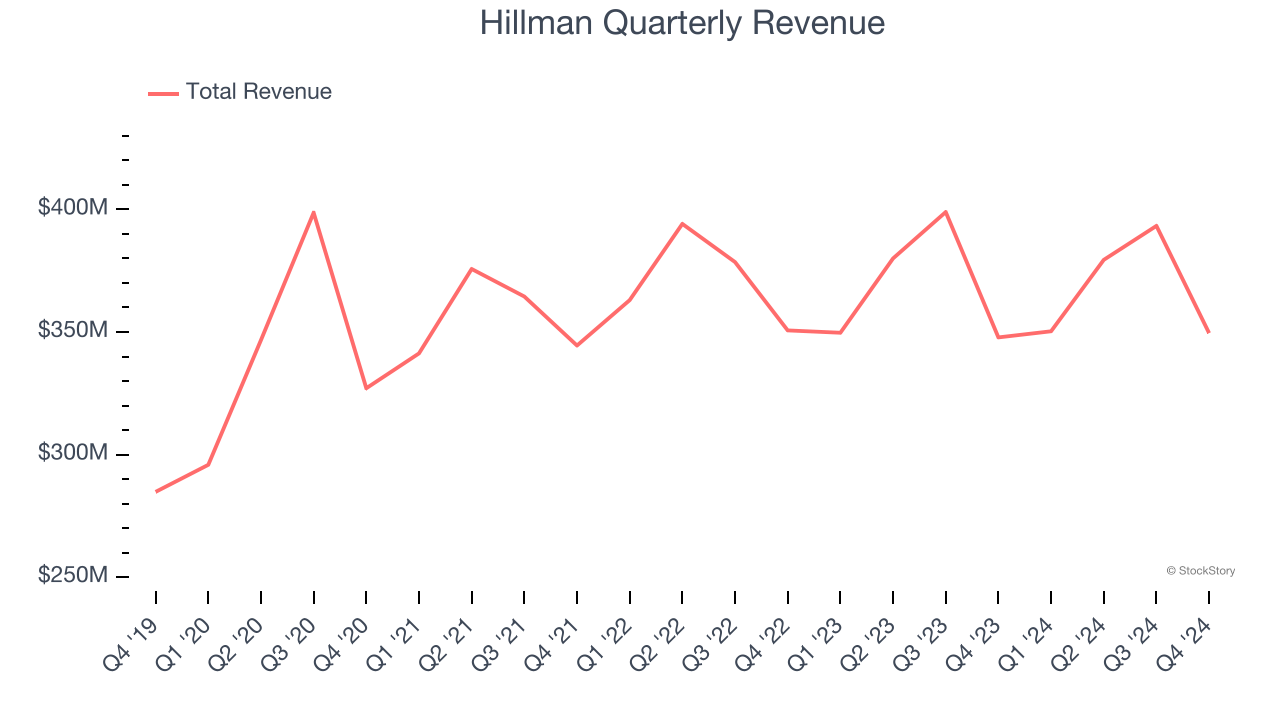

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Hillman’s 3.9% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the industrials sector.

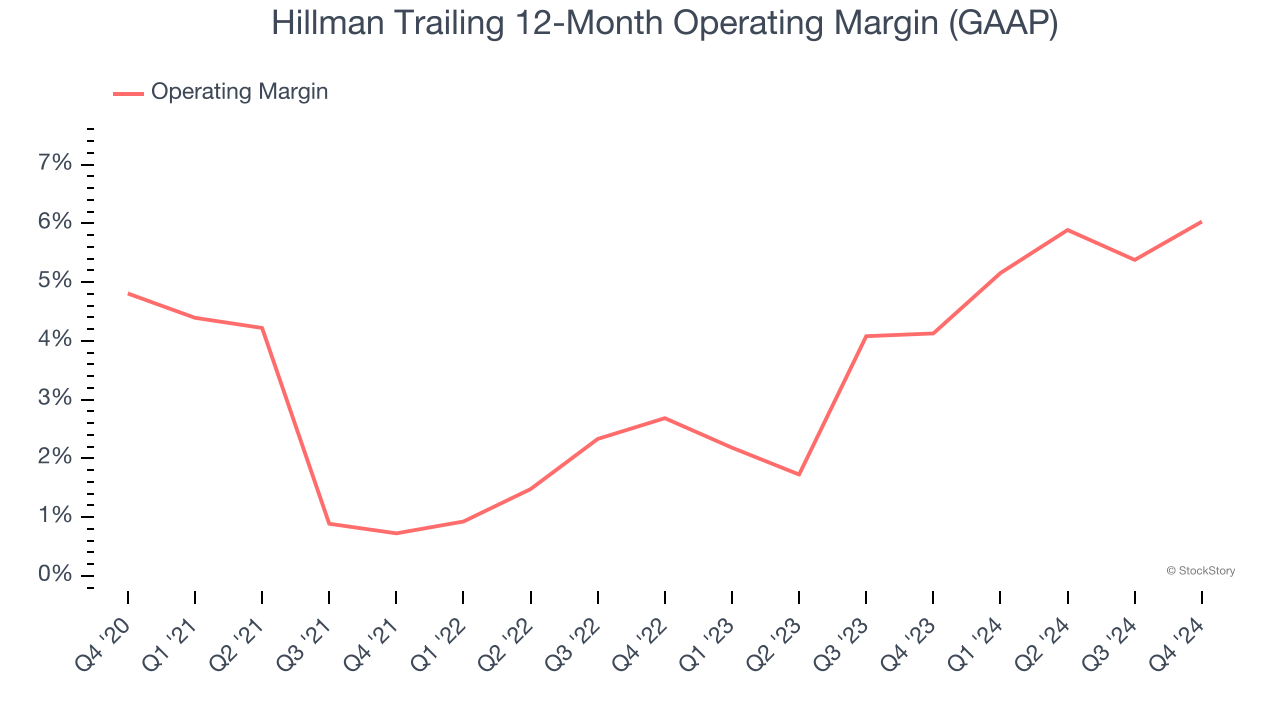

2. Weak Operating Margin Could Cause Trouble

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Hillman was profitable over the last five years but held back by its large cost base. Its average operating margin of 3.7% was weak for an industrials business. This result is surprising given its high gross margin as a starting point.

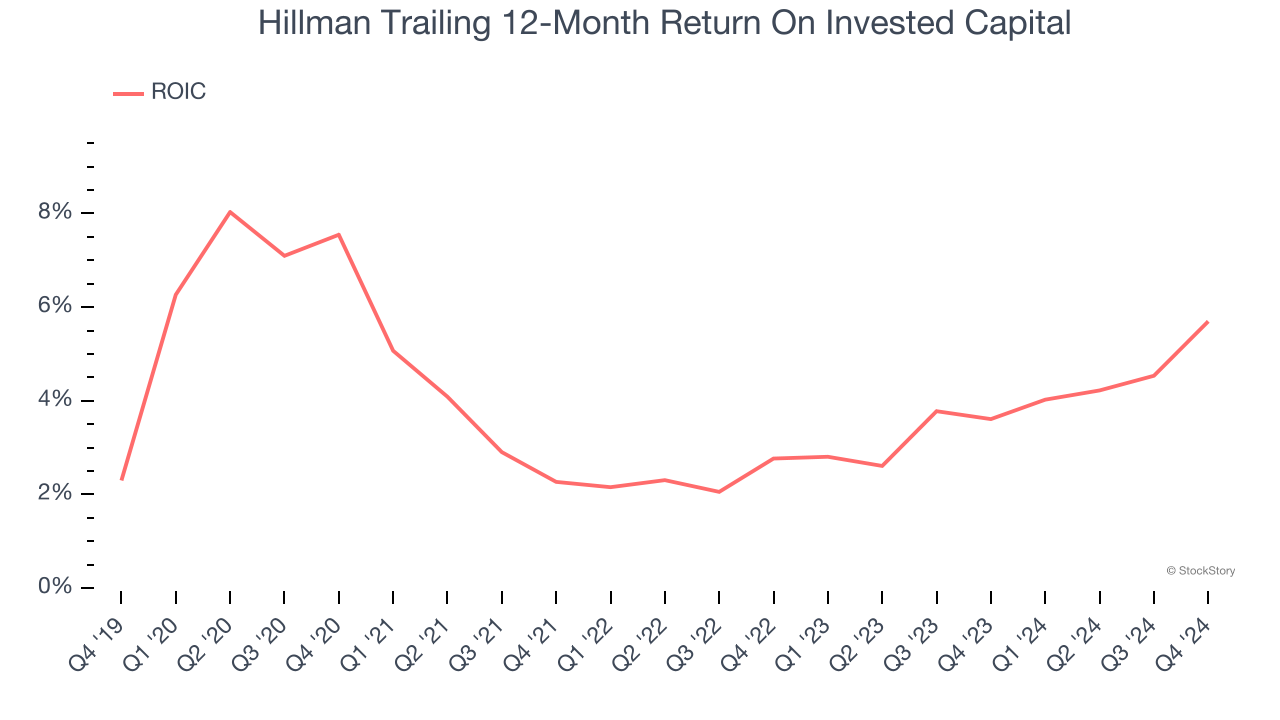

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Hillman historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 4.4%, lower than the typical cost of capital (how much it costs to raise money) for industrials companies.

Final Judgment

Hillman isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 15.5× forward price-to-earnings (or $8.52 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere. We’d suggest looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of Hillman

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.