Biopharma manufacturing company Repligen Corporation (NASDAQ: RGEN) reported Q1 CY2025 results beating Wall Street’s revenue expectations, with sales up 10.4% year on year to $169.2 million. The company’s full-year revenue guidance of $707.5 million at the midpoint came in 1% above analysts’ estimates. Its non-GAAP profit of $0.39 per share was 11.4% above analysts’ consensus estimates.

Is now the time to buy Repligen? Find out by accessing our full research report, it’s free.

Repligen (RGEN) Q1 CY2025 Highlights:

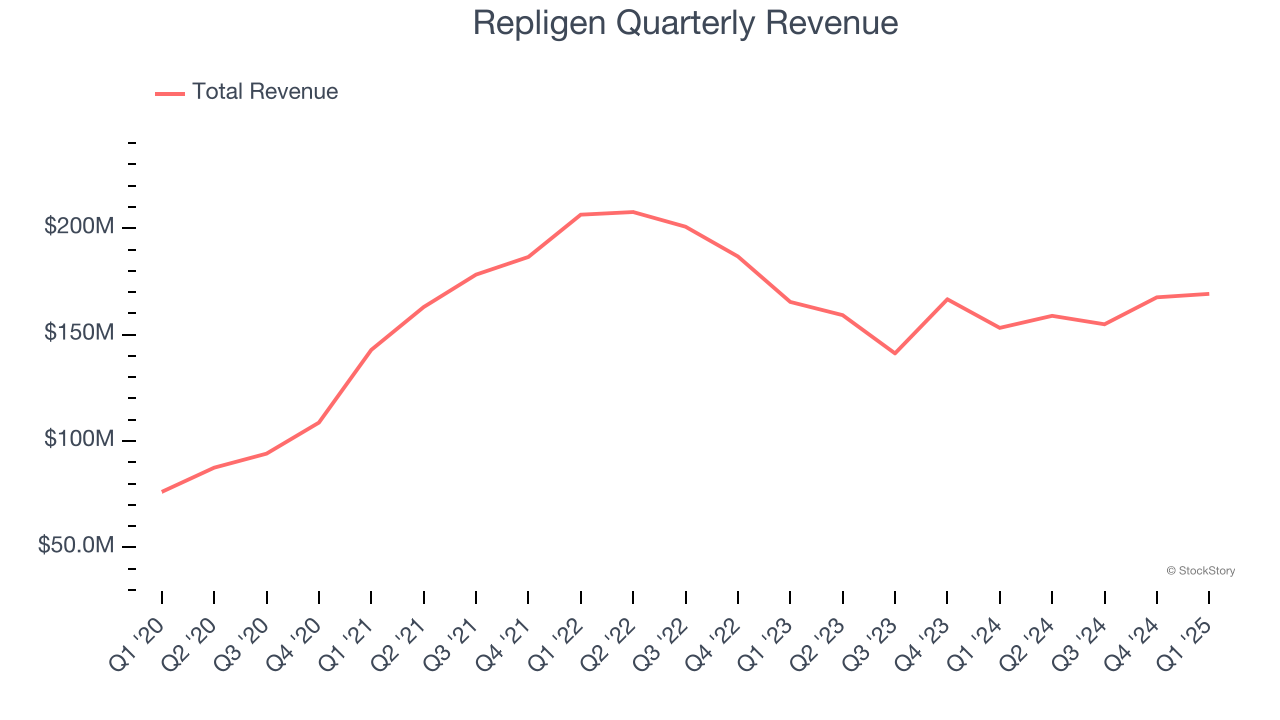

- Revenue: $169.2 million vs analyst estimates of $164.3 million (10.4% year-on-year growth, 3% beat)

- Adjusted EPS: $0.39 vs analyst estimates of $0.35 (11.4% beat)

- Adjusted EBITDA: $25 million vs analyst estimates of $28.78 million (14.8% margin, 13.2% miss)

- The company lifted its revenue guidance for the full year to $707.5 million at the midpoint from $697.5 million, a 1.4% increase

- Management lowered its full-year Adjusted EPS guidance to $1.67 at the midpoint, a 2.3% decrease

- Operating Margin: 3.9%, up from 2.4% in the same quarter last year

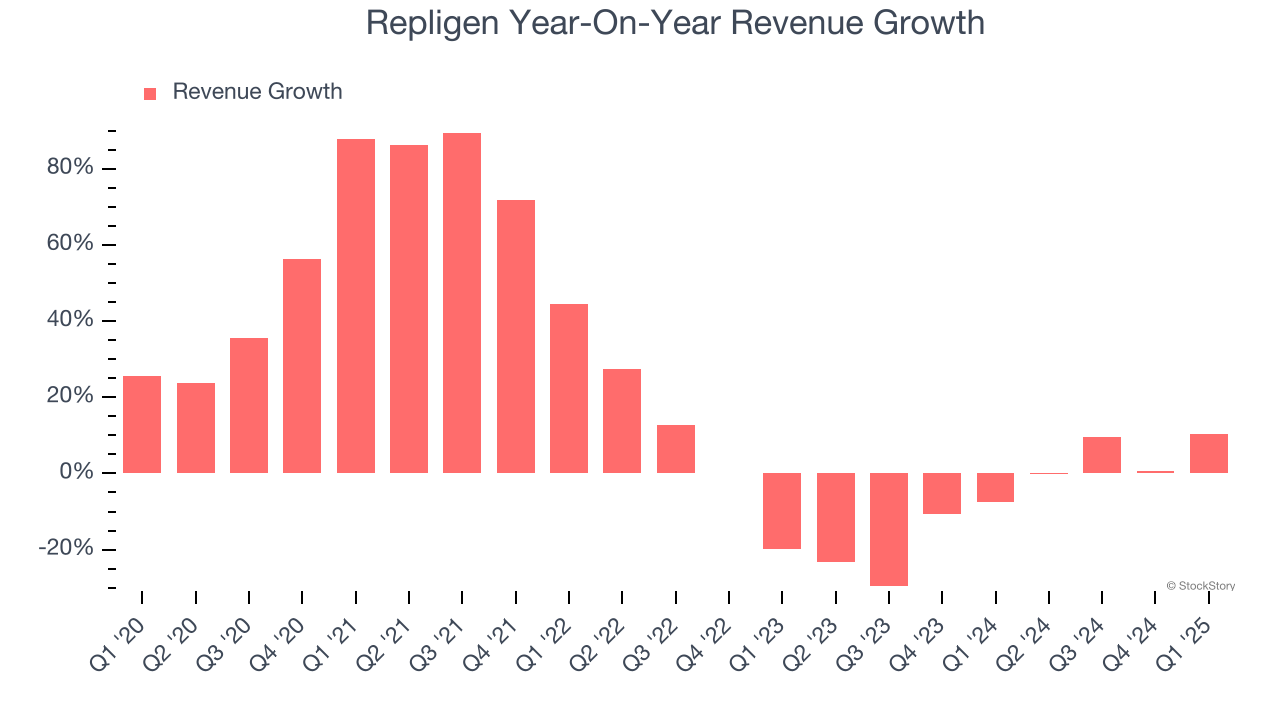

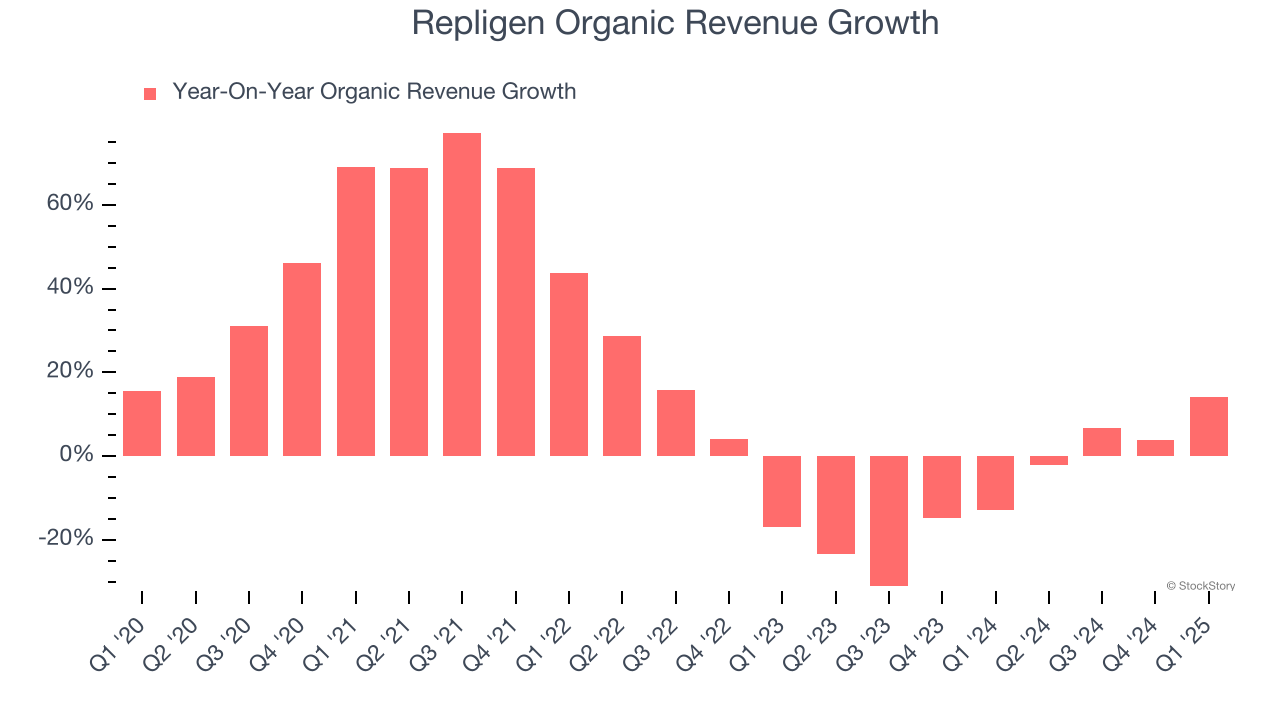

- Organic Revenue rose 14% year on year (-12.9% in the same quarter last year)

- Market Capitalization: $8.07 billion

Olivier Loeillot, President and Chief Executive Officer of Repligen said, “We had a strong start to the year with $169 million of revenue, which represented 14% organic non-COVID growth and helped drive meaningful adjusted operating margin expansion. Total orders grew nearly 20%, with all four franchises growing double-digits, highlighting the momentum in our business. As a result, we are confident in our organic growth outlook for the full year. Strategically, we strengthened our Analytics franchise with the acquisition of 908’s bioprocessing portfolio. Finally, we are working to navigate through the current economic environment and at this point in time, we see minimal impact from tariffs on our EPS.”

Company Overview

With over 13 strategic acquisitions since 2012 to build its comprehensive bioprocessing portfolio, Repligen (NASDAQ: RGEN) develops and manufactures specialized technologies that improve the efficiency and flexibility of biological drug manufacturing processes.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Repligen’s sales grew at an impressive 17.9% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Repligen’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 7.5% over the last two years.

Repligen also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Repligen’s organic revenue averaged 7.5% year-on-year declines. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Repligen reported year-on-year revenue growth of 10.4%, and its $169.2 million of revenue exceeded Wall Street’s estimates by 3%.

Looking ahead, sell-side analysts expect revenue to grow 11.8% over the next 12 months, an improvement versus the last two years. This projection is healthy and indicates its newer products and services will spur better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

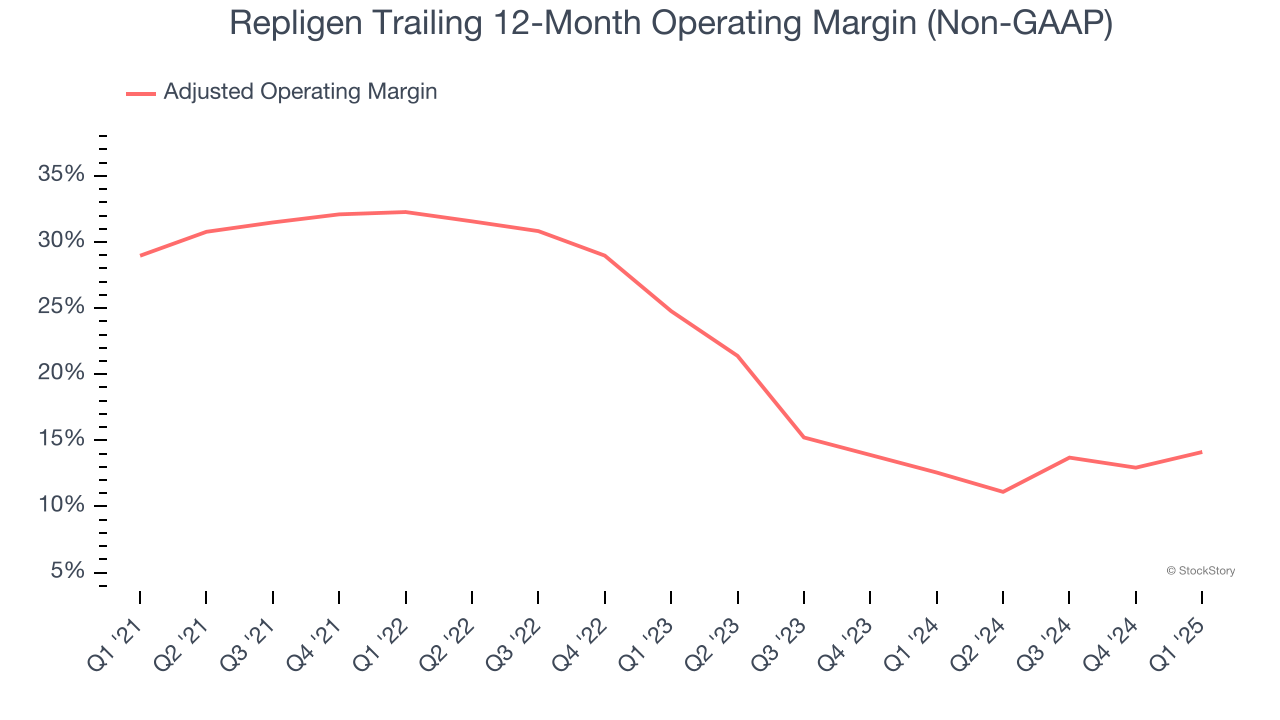

Repligen has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average adjusted operating margin of 22.5%.

Looking at the trend in its profitability, Repligen’s adjusted operating margin decreased by 14.8 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 10.7 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q1, Repligen generated an adjusted operating profit margin of 13.8%, up 4.9 percentage points year on year. This increase was a welcome development and shows it was more efficient.

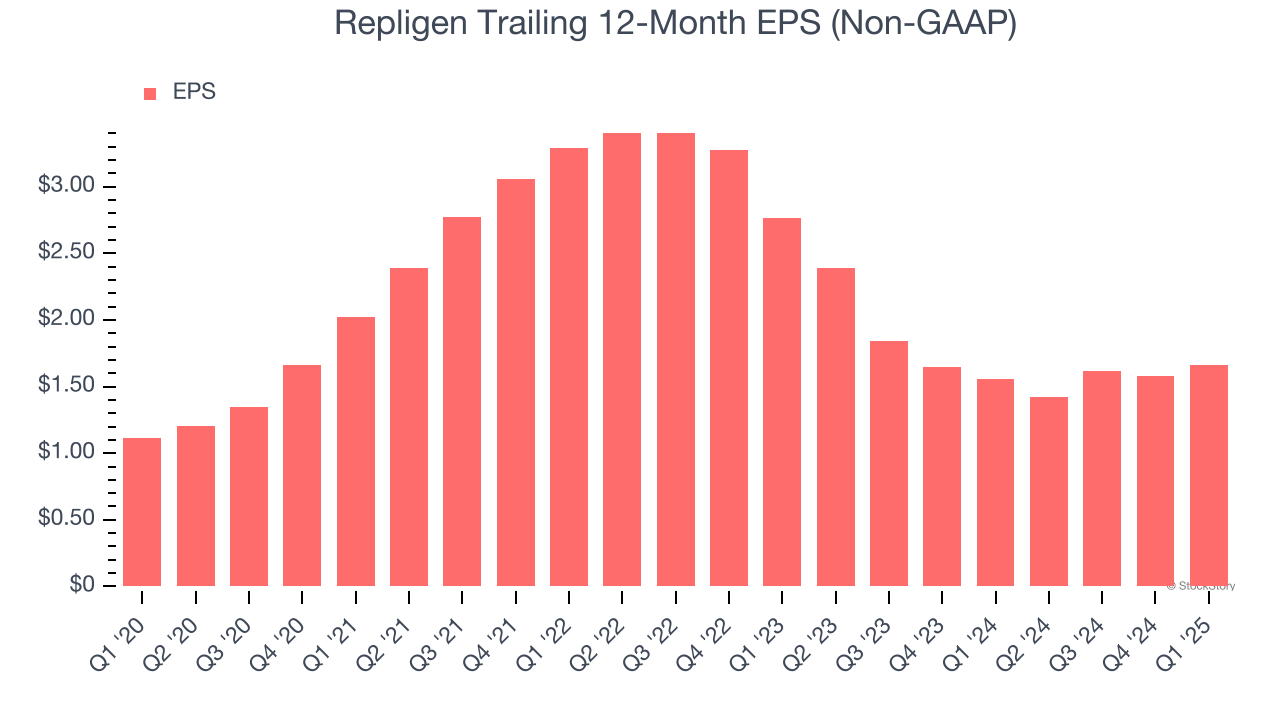

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Repligen’s EPS grew at a solid 8.4% compounded annual growth rate over the last five years. However, this performance was lower than its 17.9% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded.

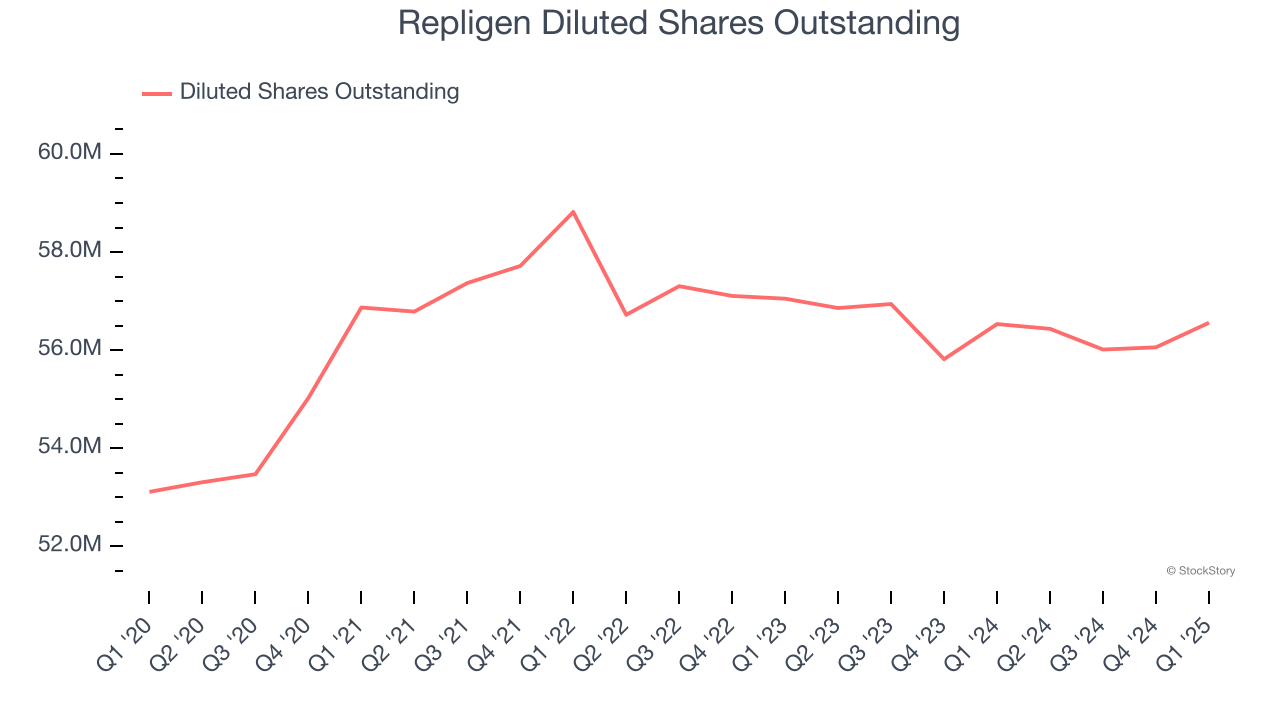

We can take a deeper look into Repligen’s earnings to better understand the drivers of its performance. As we mentioned earlier, Repligen’s adjusted operating margin improved this quarter but declined by 14.8 percentage points over the last five years. Its share count also grew by 6.5%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q1, Repligen reported EPS at $0.39, up from $0.30 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Repligen’s full-year EPS of $1.66 to grow 10.9%.

Key Takeaways from Repligen’s Q1 Results

We were impressed by how significantly Repligen blew past analysts’ organic revenue and EPS expectations this quarter. We were also glad it raised its full-year revenue guidance. On the other hand, its EBITDA missed and it lowered its full-year guidance. Overall, this quarter was mixed but still had some key positives. The stock remained flat at $143.63 immediately after reporting.

So do we think Repligen is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.