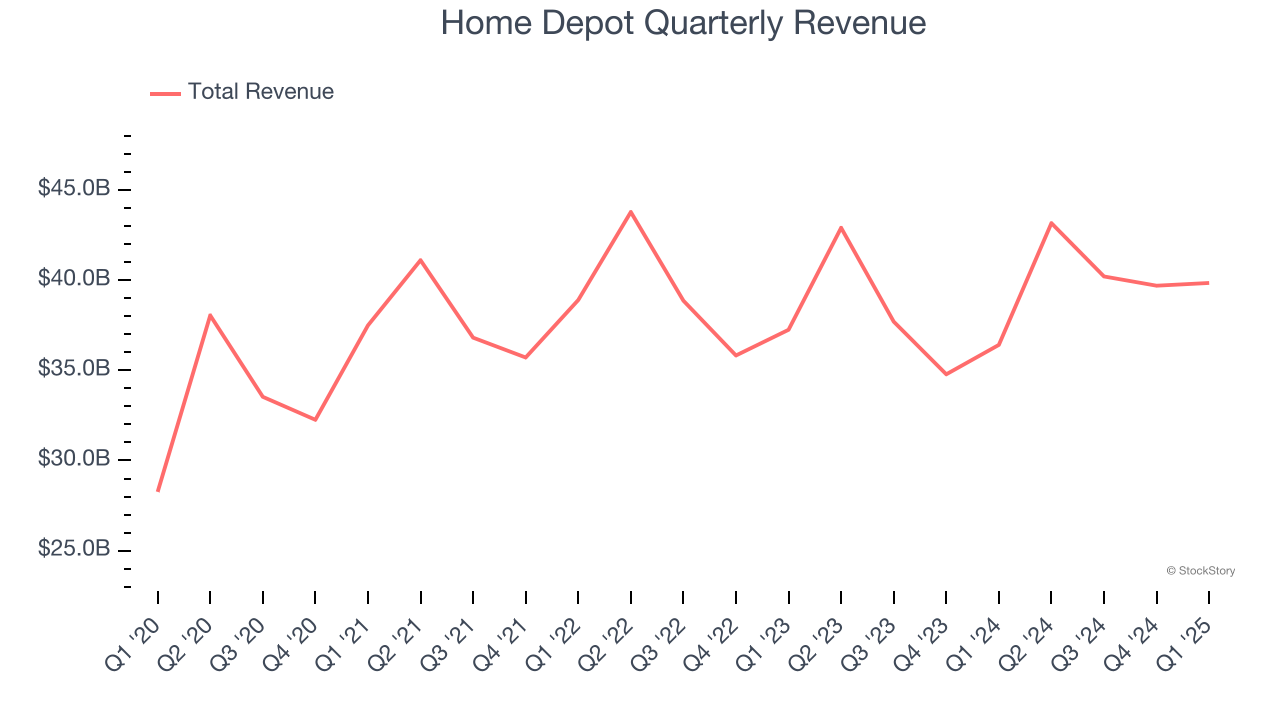

Home improvement retail giant Home Depot (NYSE: HD) reported Q1 CY2025 results beating Wall Street’s revenue expectations, with sales up 9.4% year on year to $39.86 billion. Its non-GAAP profit of $3.56 per share was 0.8% below analysts’ consensus estimates.

Is now the time to buy Home Depot? Find out by accessing our full research report, it’s free.

Home Depot (HD) Q1 CY2025 Highlights:

- Revenue: $39.86 billion vs analyst estimates of $39.24 billion (9.4% year-on-year growth, 1.6% beat)

- Adjusted EPS: $3.56 vs analyst expectations of $3.59 (0.8% miss)

- Reaffirmed fiscal 2025 guidance (2.8% sales growth, 2% decline in adjusted EPS)

- Operating Margin: 12.9%, down from 13.9% in the same quarter last year

- Free Cash Flow Margin: 8.8%, down from 12.8% in the same quarter last year

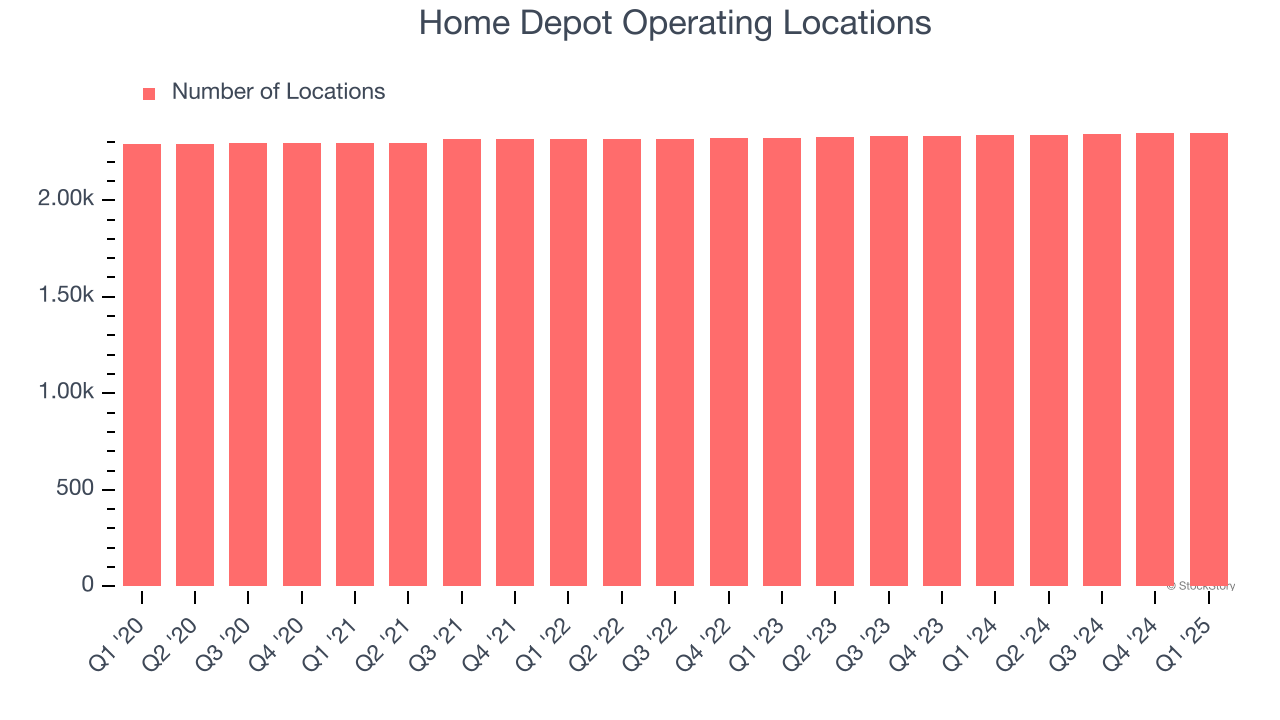

- Locations: 2,350 at quarter end, up from 2,337 in the same quarter last year

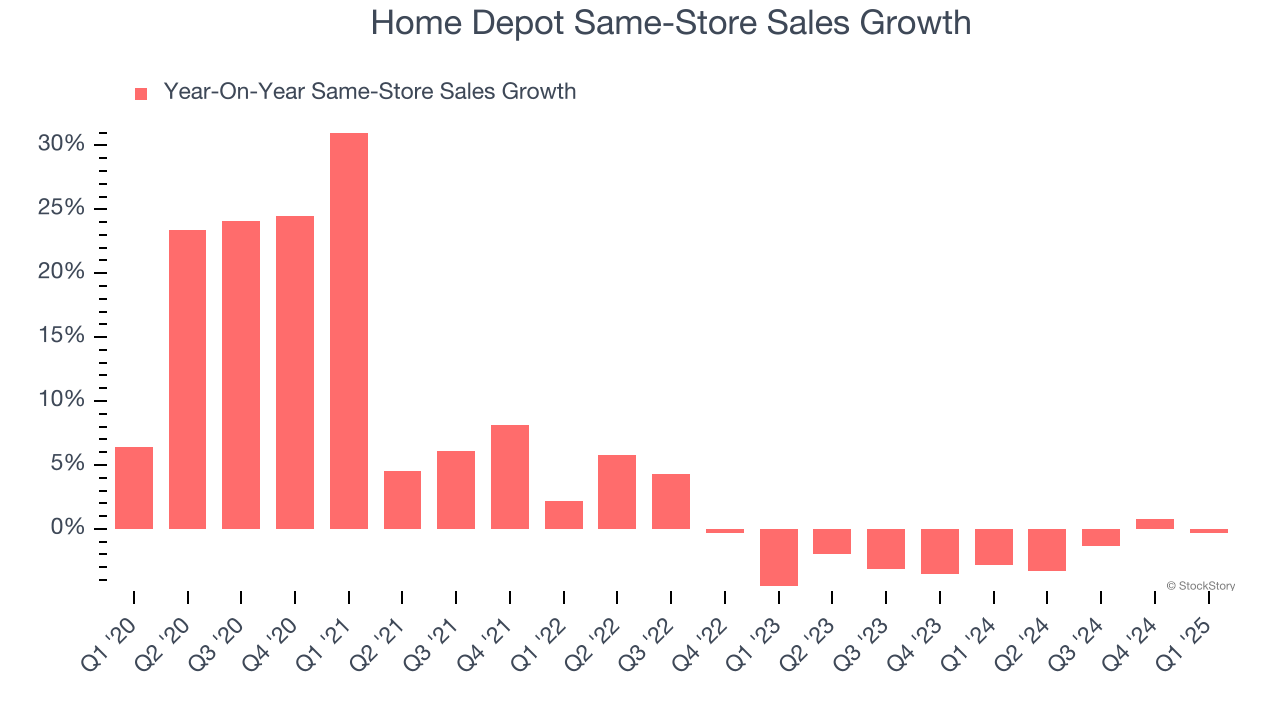

- Same-Store Sales were essentially flat, decreasing 0.3% year on year (-2.8% in the same quarter last year)

- Market Capitalization: $377.1 billion

"Our first quarter results were in line with our expectations as we saw continued customer engagement across smaller projects and in our spring events," said Ted Decker, chair, president and CEO.

Company Overview

Founded and headquartered in Atlanta, Georgia, Home Depot (NYSE: HD) is a home improvement retailer that sells everything from tools to building materials to appliances.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $163 billion in revenue over the past 12 months, Home Depot is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because there are only a finite number of places to build new stores, making it harder to find incremental growth. To expand meaningfully, Home Depot likely needs to tweak its prices or enter new markets.

As you can see below, Home Depot’s sales grew at a tepid 6.8% compounded annual growth rate over the last six years (we compare to 2019 to normalize for COVID-19 impacts) as it didn’t open many new stores.

This quarter, Home Depot reported year-on-year revenue growth of 9.4%, and its $39.86 billion of revenue exceeded Wall Street’s estimates by 1.6%.

Looking ahead, sell-side analysts expect revenue to grow 1.5% over the next 12 months, a deceleration versus the last six years. This projection doesn't excite us and suggests its products will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Store Performance

Number of Stores

Home Depot operated 2,350 locations in the latest quarter, and over the last two years, has kept its store count flat while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Home Depot’s demand has been shrinking over the last two years as its same-store sales have averaged 1.9% annual declines. This performance isn’t ideal, and we’d be concerned if Home Depot starts opening new stores to artificially boost revenue growth.

In the latest quarter, Home Depot’s year on year same-store sales were essentially flat, decreasing 0.3% year-on-year. This performance was a well-appreciated turnaround from its historical levels, showing the business is improving.

Key Takeaways from Home Depot’s Q1 Results

It was encouraging to see Home Depot beat analysts’ revenue expectations this quarter. On the other hand, its EBITDA slightly missed. Zooming out, we think this was a mixed quarter. The stock traded up 1.8% to $386 immediately after reporting.

So do we think Home Depot is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.