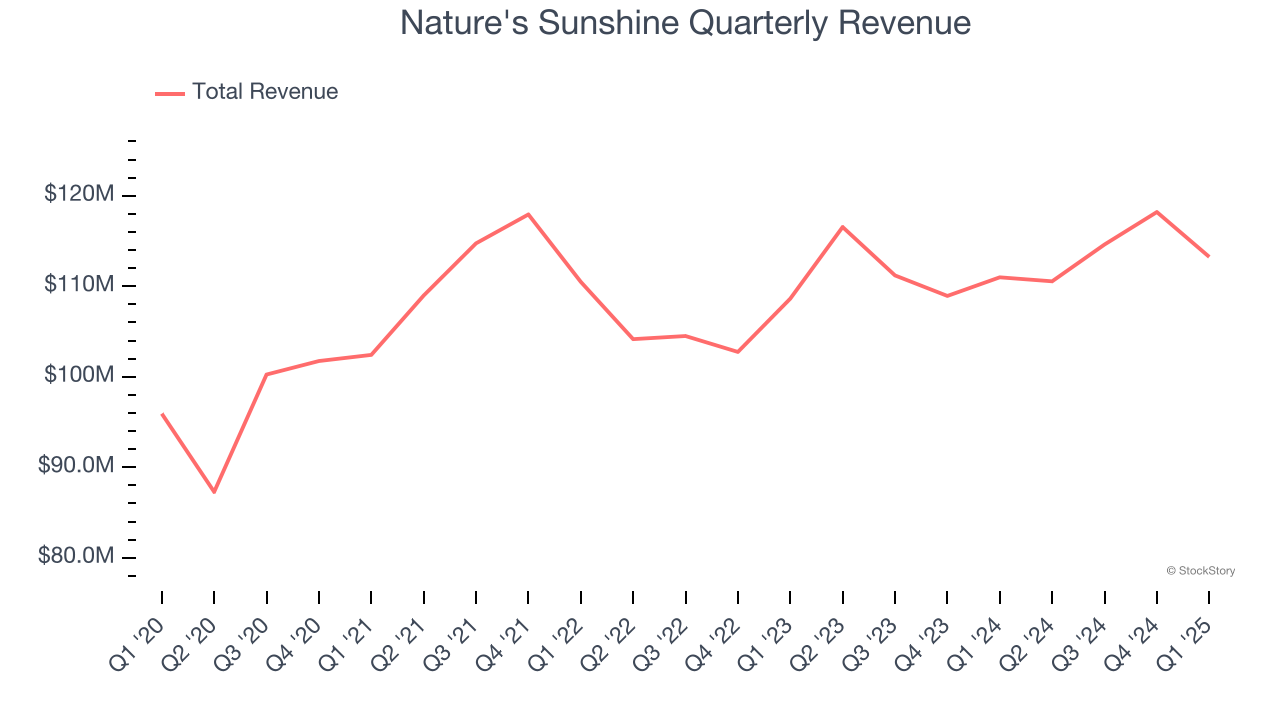

Wellness products company Nature’s Sunshine (NASDAQ: NATR) reported Q1 CY2025 results beating Wall Street’s revenue expectations, with sales up 2% year on year to $113.2 million. The company expects the full year’s revenue to be around $457.5 million, close to analysts’ estimates. Its GAAP profit of $0.25 per share was 51.5% above analysts’ consensus estimates.

Is now the time to buy Nature's Sunshine? Find out by accessing our full research report, it’s free.

Nature's Sunshine (NATR) Q1 CY2025 Highlights:

- Revenue: $113.2 million vs analyst estimates of $109.3 million (2% year-on-year growth, 3.6% beat)

- EPS (GAAP): $0.25 vs analyst estimates of $0.17 (51.5% beat)

- Adjusted EBITDA: $10.97 million vs analyst estimates of $9.75 million (9.7% margin, 12.5% beat)

- The company reconfirmed its revenue guidance for the full year of $457.5 million at the midpoint

- EBITDA guidance for the full year is $41 million at the midpoint, below analyst estimates of $42.98 million

- Operating Margin: 5.4%, up from 4.2% in the same quarter last year

- Free Cash Flow was $1.50 million, up from -$1.50 million in the same quarter last year

- Market Capitalization: $231 million

“2025 got off to a strong start, as first quarter revenue came in at $113 million, up 5% on a constant currency basis, and adjusted EBITDA came in at $11 million, up 20% versus prior year,” said Terrence Moorehead, CEO of Nature’s Sunshine.

Company Overview

Started on a kitchen table in Utah, Nature’s Sunshine (NASDAQ: NATR) manufactures and sells nutritional and personal care products.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $456.6 million in revenue over the past 12 months, Nature's Sunshine is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Nature's Sunshine struggled to increase demand as its $456.6 million of sales for the trailing 12 months was close to its revenue three years ago. This shows demand was soft, a poor baseline for our analysis.

This quarter, Nature's Sunshine reported modest year-on-year revenue growth of 2% but beat Wall Street’s estimates by 3.6%.

Looking ahead, sell-side analysts expect revenue to grow 1.6% over the next 12 months, similar to its three-year rate. While this projection implies its newer products will fuel better top-line performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

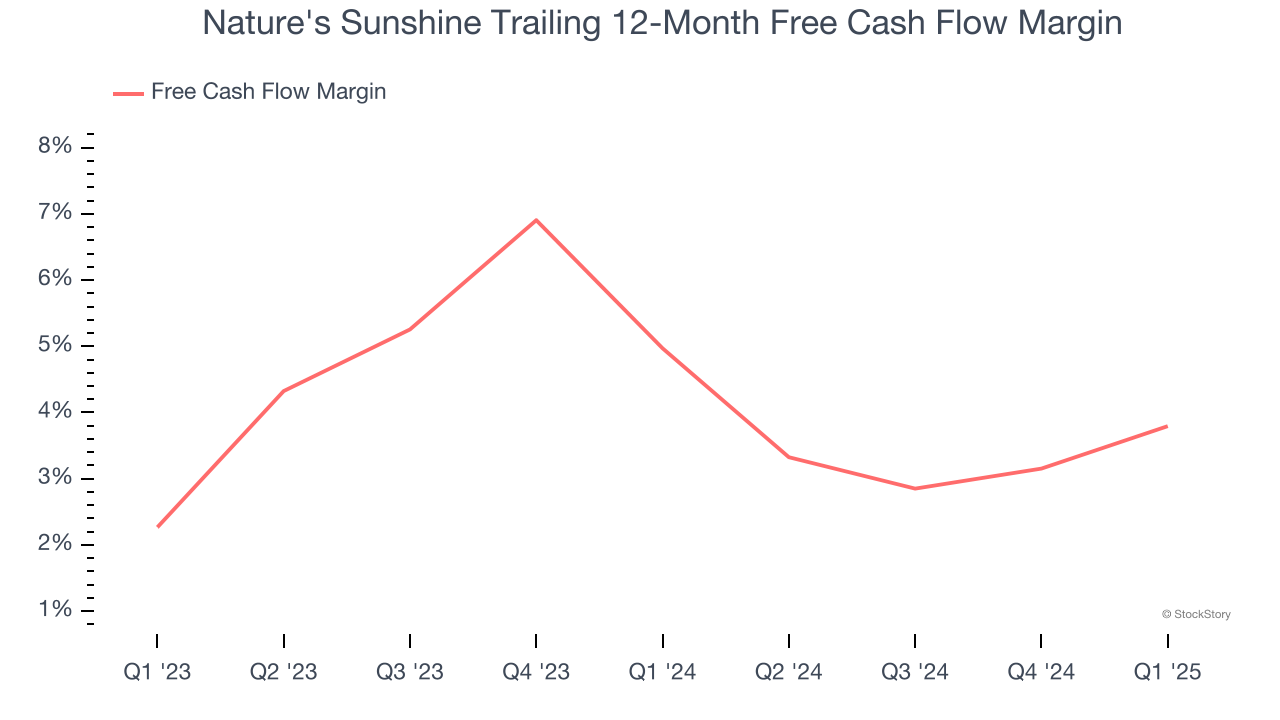

Nature's Sunshine has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.4%, subpar for a consumer staples business.

Taking a step back, we can see that Nature's Sunshine’s margin dropped by 1.2 percentage points over the last year. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s in the middle of an investment cycle.

Nature's Sunshine’s free cash flow clocked in at $1.50 million in Q1, equivalent to a 1.3% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

Key Takeaways from Nature's Sunshine’s Q1 Results

We were impressed by how significantly Nature's Sunshine blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. On the other hand, its full-year EBITDA guidance missed. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 4.3% to $12.99 immediately following the results.

Nature's Sunshine put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.