Over the past six months, Genco has been a great trade, beating the S&P 500 by 8%. Its stock price has climbed to $17.76, representing a healthy 25.7% increase. This run-up might have investors contemplating their next move.

Is now the time to buy Genco, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Genco Not Exciting?

We’re happy investors have made money, but we don't have much confidence in Genco. Here are three reasons you should be careful with GNK and a stock we'd rather own.

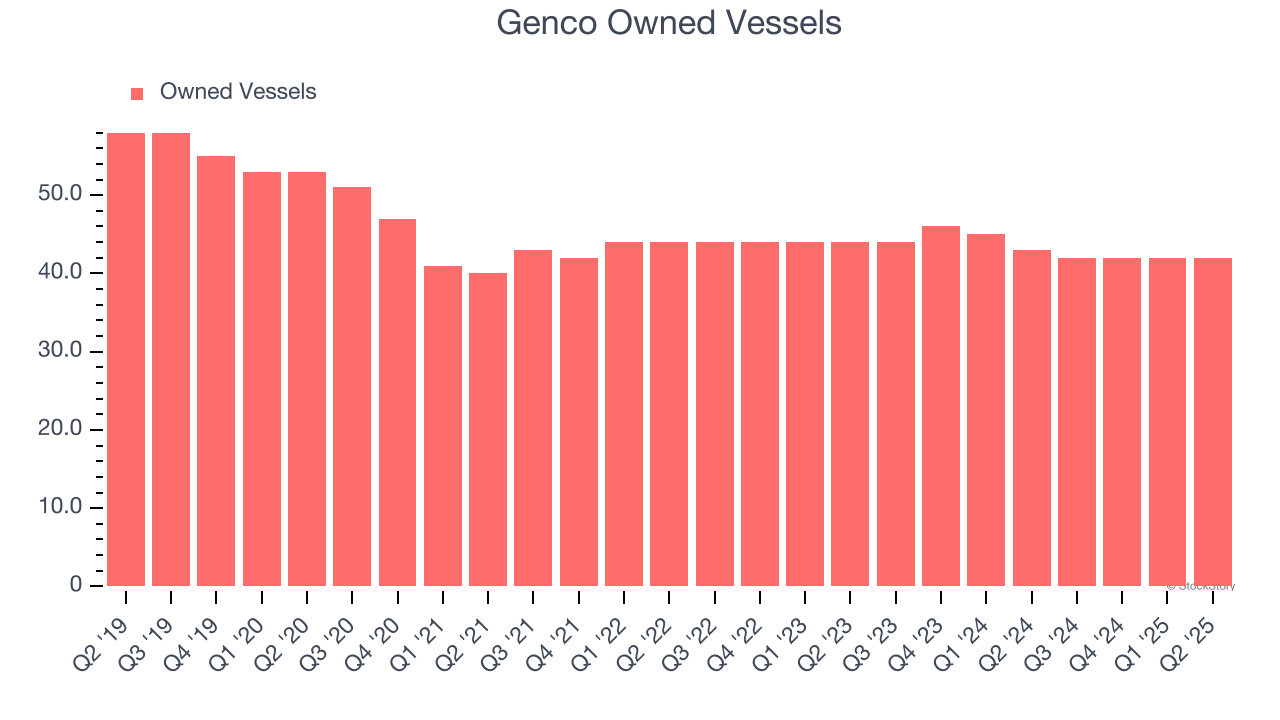

1. Decline in owned vessels Points to Weak Demand

Revenue growth can be broken down into changes in price and volume (for companies like Genco, our preferred volume metric is owned vessels). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Genco’s owned vessels came in at 42 in the latest quarter, and over the last two years, averaged 2.2% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Genco might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

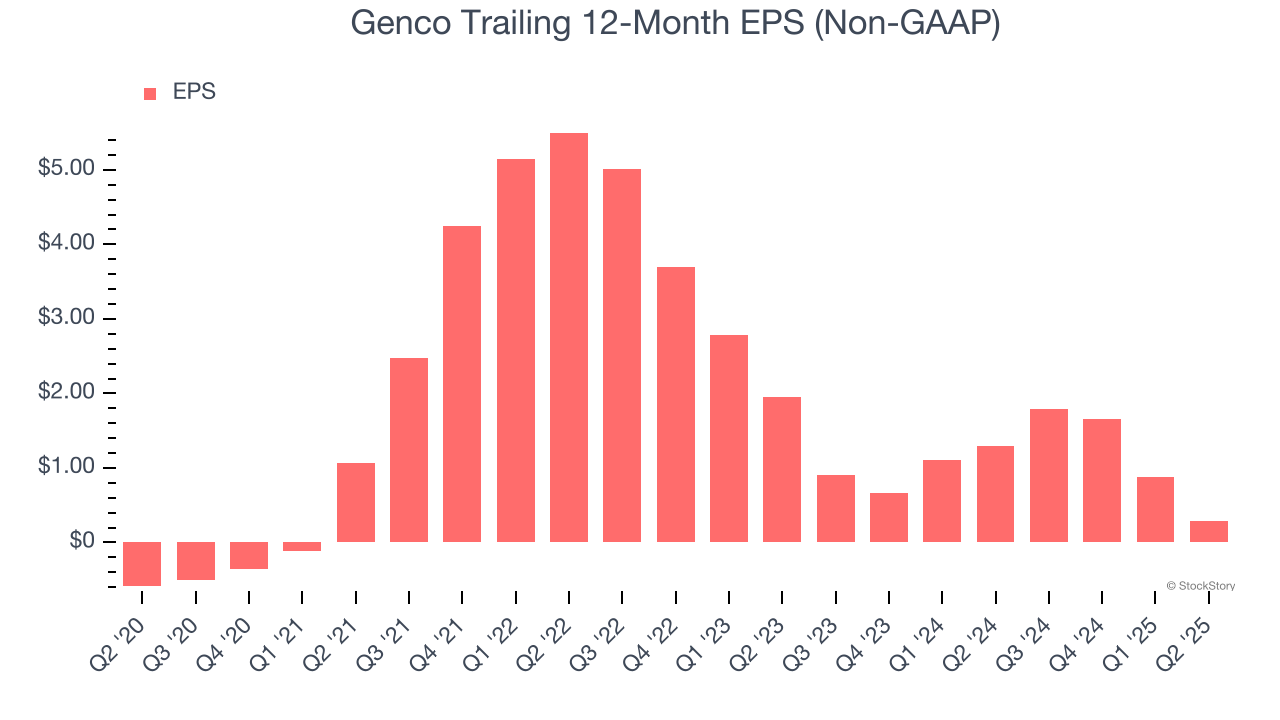

2. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Genco, its EPS declined by more than its revenue over the last two years, dropping 61.9%. This tells us the company struggled to adjust to shrinking demand.

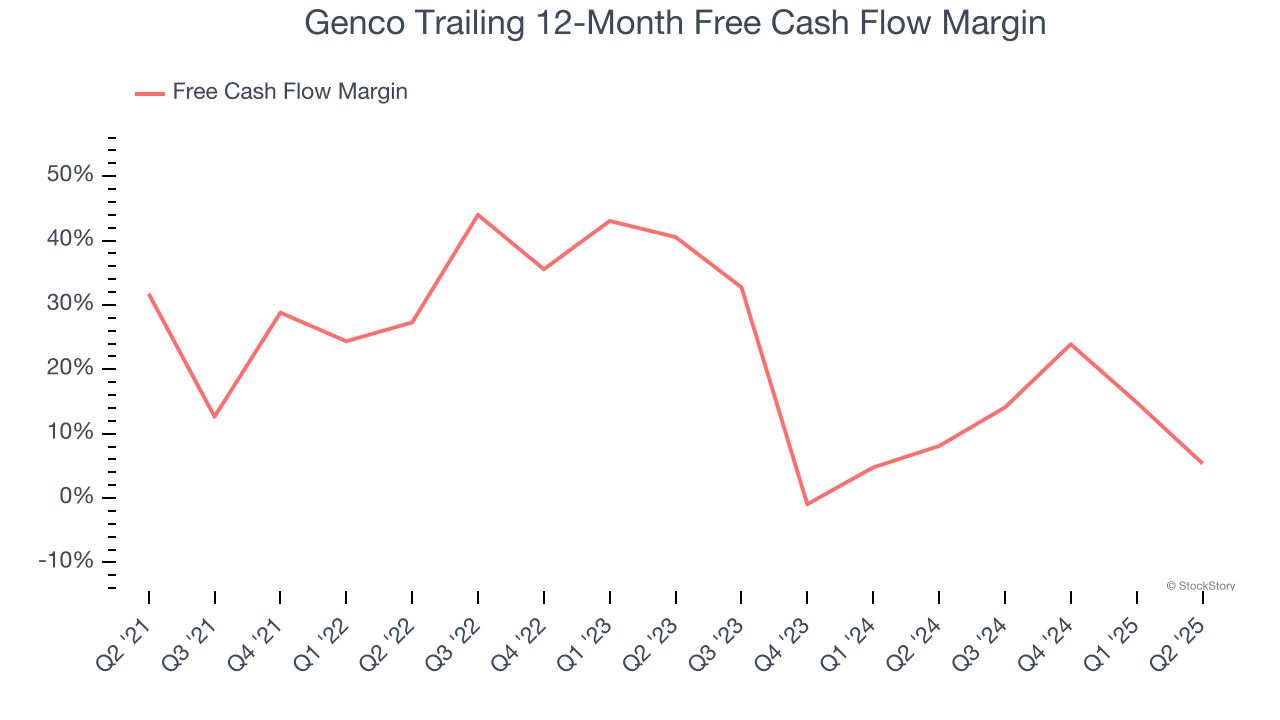

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Genco’s margin dropped by 26.4 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Genco’s free cash flow margin for the trailing 12 months was 5.4%.

Final Judgment

Genco isn’t a terrible business, but it doesn’t pass our bar. With its shares outperforming the market lately, the stock trades at 18.7× forward P/E (or $17.76 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward one of our top software and edge computing picks.

Stocks We Would Buy Instead of Genco

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.