Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at Chegg (NYSE: CHGG) and its peers.

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

The 8 consumer subscription stocks we track reported a mixed Q2. As a group, revenues beat analysts’ consensus estimates by 2.5% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 7.3% on average since the latest earnings results.

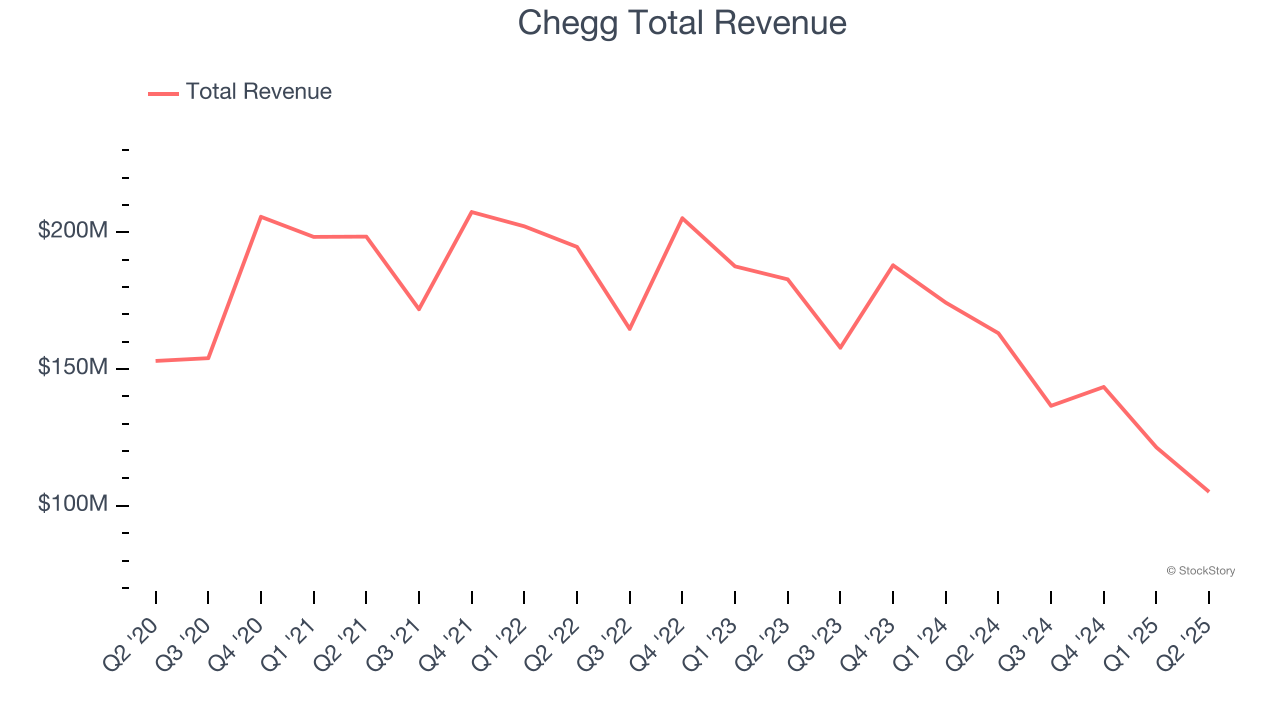

Chegg (NYSE: CHGG)

Started as a physical textbook rental service, Chegg (NYSE: CHGG) is now a digital platform addressing student pain points by providing study and academic assistance.

Chegg reported revenues of $105.1 million, down 35.6% year on year. This print exceeded analysts’ expectations by 3.8%. Despite the top-line beat, it was still a slower quarter for the company with a decline in its users and a significant miss of analysts’ number of services subscribers estimates.

Chegg delivered the slowest revenue growth of the whole group. The company reported 2.62 million users, down 39.9% year on year. Interestingly, the stock is up 35.9% since reporting and currently trades at $1.74.

Read our full report on Chegg here, it’s free.

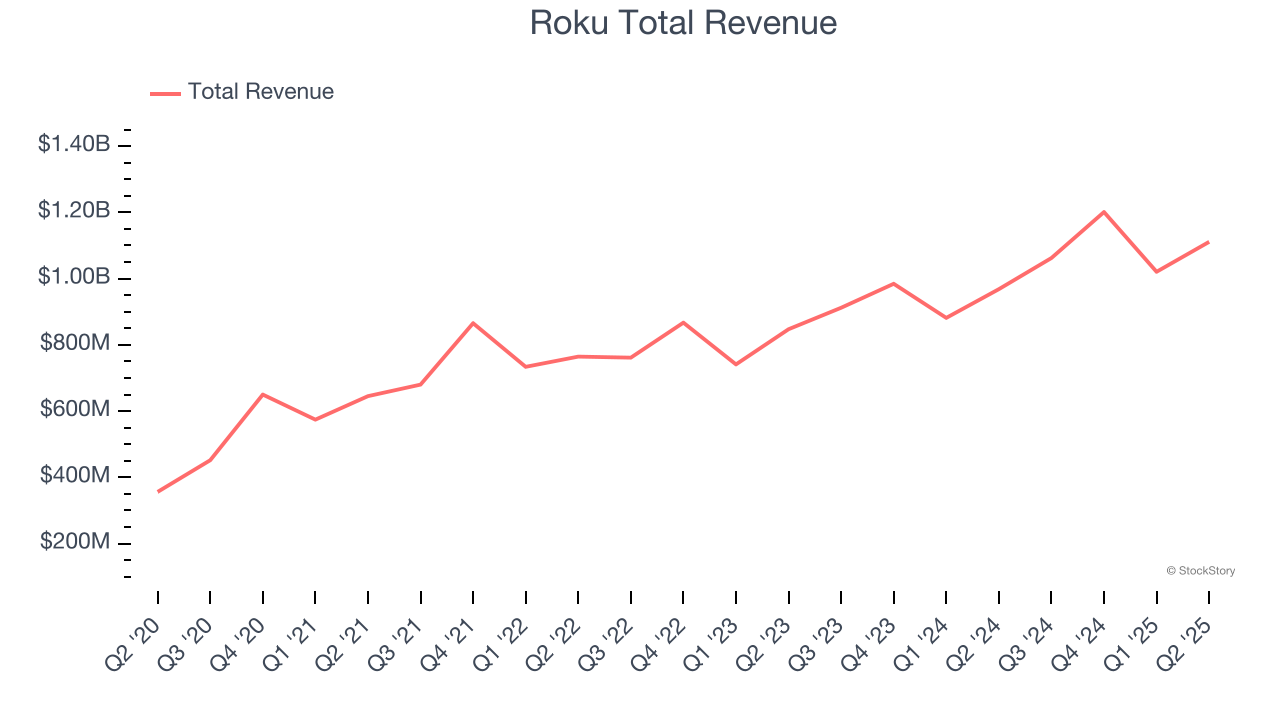

Best Q2: Roku (NASDAQ: ROKU)

With a name meaning six in Japanese because it was the founder's sixth company that he started, Roku (NASDAQ: ROKU) makes hardware players that offer access to various online streaming TV services.

Roku reported revenues of $1.11 billion, up 14.8% year on year, outperforming analysts’ expectations by 3.8%. The business had a very strong quarter with a solid beat of analysts’ EBITDA estimates and full-year EBITDA guidance exceeding analysts’ expectations.

The market seems content with the results as the stock is up 4.5% since reporting. It currently trades at $98.49.

Is now the time to buy Roku? Access our full analysis of the earnings results here, it’s free.

Match Group (NASDAQ: MTCH)

Originally started as a dial-up service before widespread internet adoption, Match (NASDAQ: MTCH) was an early innovator in online dating and today has a portfolio of apps including Tinder, Hinge, Archer, and OkCupid.

Match Group reported revenues of $863.7 million, flat year on year, exceeding analysts’ expectations by 1.2%. Still, it was a softer quarter as it posted a decline in its users and a slight miss of analysts’ number of payers estimates.

Interestingly, the stock is up 9.7% since the results and currently trades at $37.

Read our full analysis of Match Group’s results here.

Duolingo (NASDAQ: DUOL)

Founded by a Carnegie Mellon computer science professor and his Ph.D. student, Duolingo (NASDAQ: DUOL) is a mobile app helping people learn new languages.

Duolingo reported revenues of $252.3 million, up 41.5% year on year. This result surpassed analysts’ expectations by 4.8%. Overall, it was a strong quarter as it also put up a solid beat of analysts’ EBITDA estimates.

Duolingo achieved the biggest analyst estimates beat and fastest revenue growth among its peers. The company reported 128.3 million users, up 23.8% year on year. The stock is down 13% since reporting and currently trades at $299.50.

Read our full, actionable report on Duolingo here, it’s free.

Netflix (NASDAQ: NFLX)

Launched by Reed Hastings as a DVD mail rental company until its famous pivot to streaming in 2007, Netflix (NASDAQ: NFLX) is a pioneering streaming content platform.

Netflix reported revenues of $11.08 billion, up 15.9% year on year. This print was in line with analysts’ expectations. Zooming out, it was a satisfactory quarter as it also recorded EPS guidance for next quarter topping analysts’ expectations but number of global streaming paid memberships in line with analysts’ estimates.

Netflix had the weakest performance against analyst estimates among its peers. The company reported 310.5 million users, up 11.8% year on year. The stock is down 4.5% since reporting and currently trades at $1,218.

Read our full, actionable report on Netflix here, it’s free.

Market Update

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.