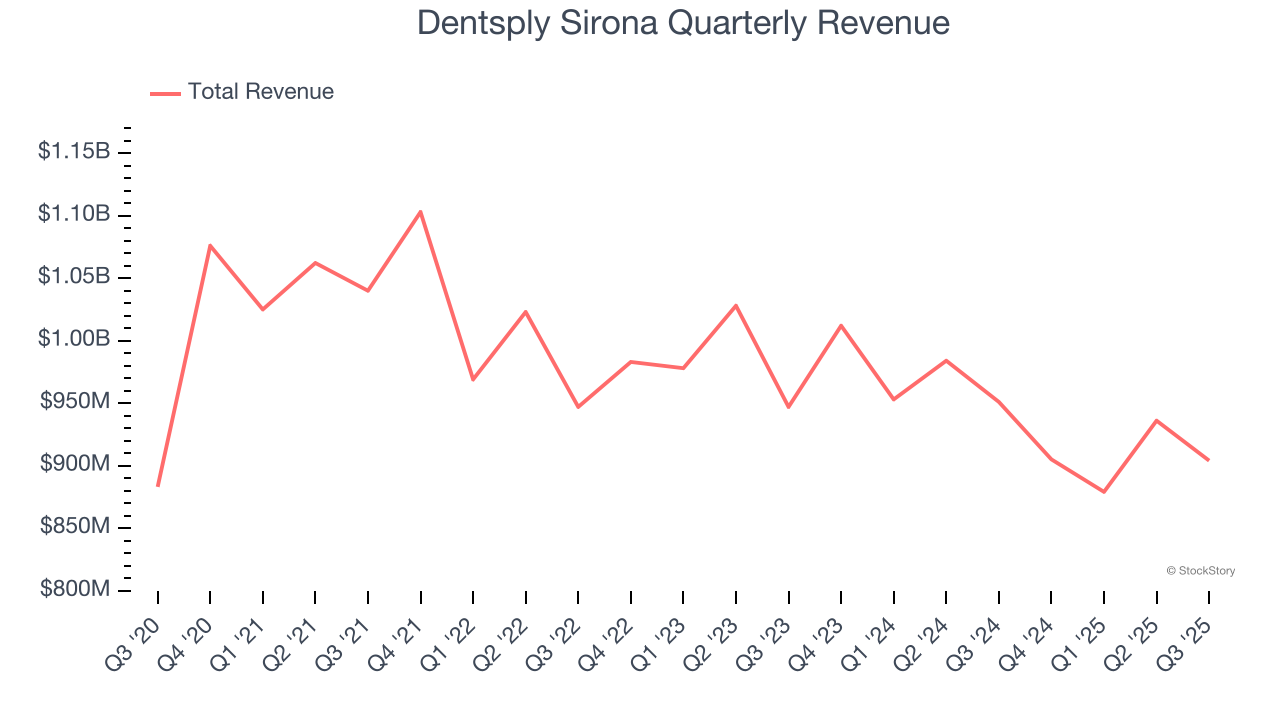

Dental products company Dentsply Sirona (NASDAQ: XRAY) reported revenue ahead of Wall Streets expectations in Q3 CY2025, but sales fell by 4.9% year on year to $904 million. The company expects the full year’s revenue to be around $3.65 billion, close to analysts’ estimates. Its non-GAAP profit of $0.37 per share was 17.7% below analysts’ consensus estimates.

Is now the time to buy Dentsply Sirona? Find out by accessing our full research report, it’s free for active Edge members.

Dentsply Sirona (XRAY) Q3 CY2025 Highlights:

- Revenue: $904 million vs analyst estimates of $899.5 million (4.9% year-on-year decline, 0.5% beat)

- Adjusted EPS: $0.37 vs analyst expectations of $0.45 (17.7% miss)

- Adjusted EBITDA: $167 million vs analyst estimates of $171.1 million (18.5% margin, 2.4% miss)

- The company reconfirmed its revenue guidance for the full year of $3.65 billion at the midpoint

- Management lowered its full-year Adjusted EPS guidance to $1.60 at the midpoint, a 15.8% decrease

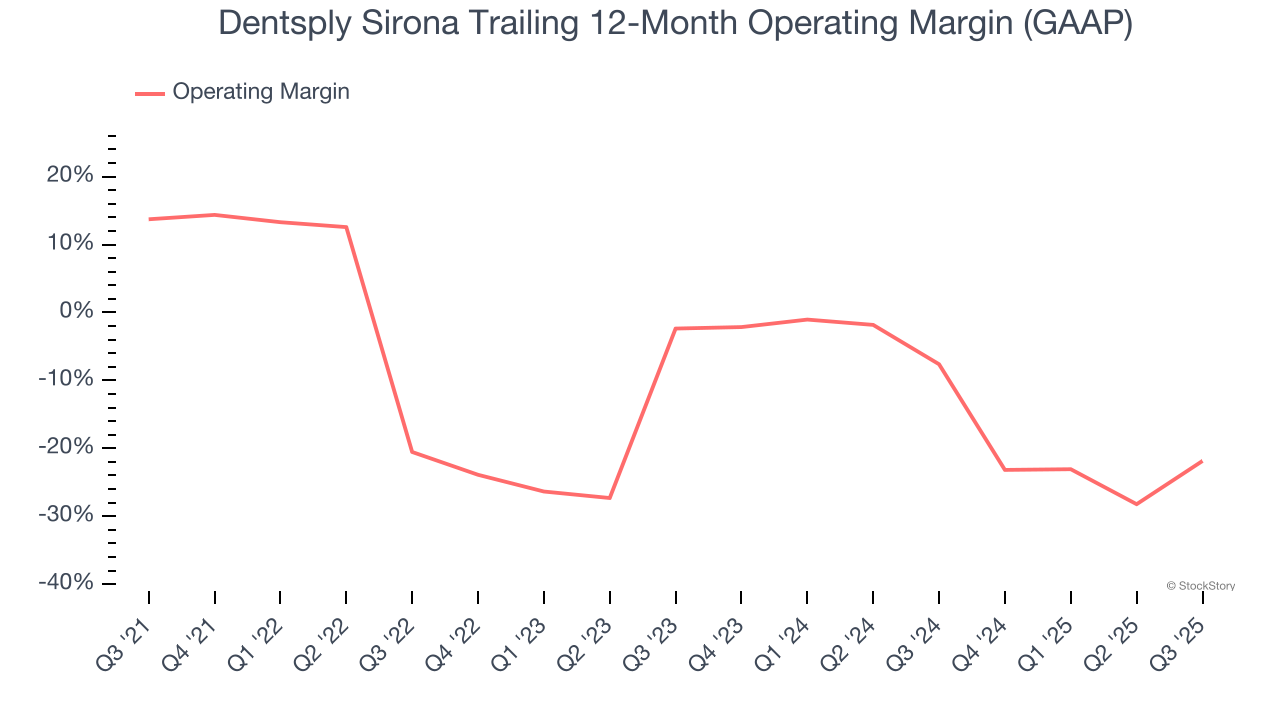

- Operating Margin: -24.1%, up from -48.6% in the same quarter last year

- Free Cash Flow Margin: 4.4%, down from 10.3% in the same quarter last year

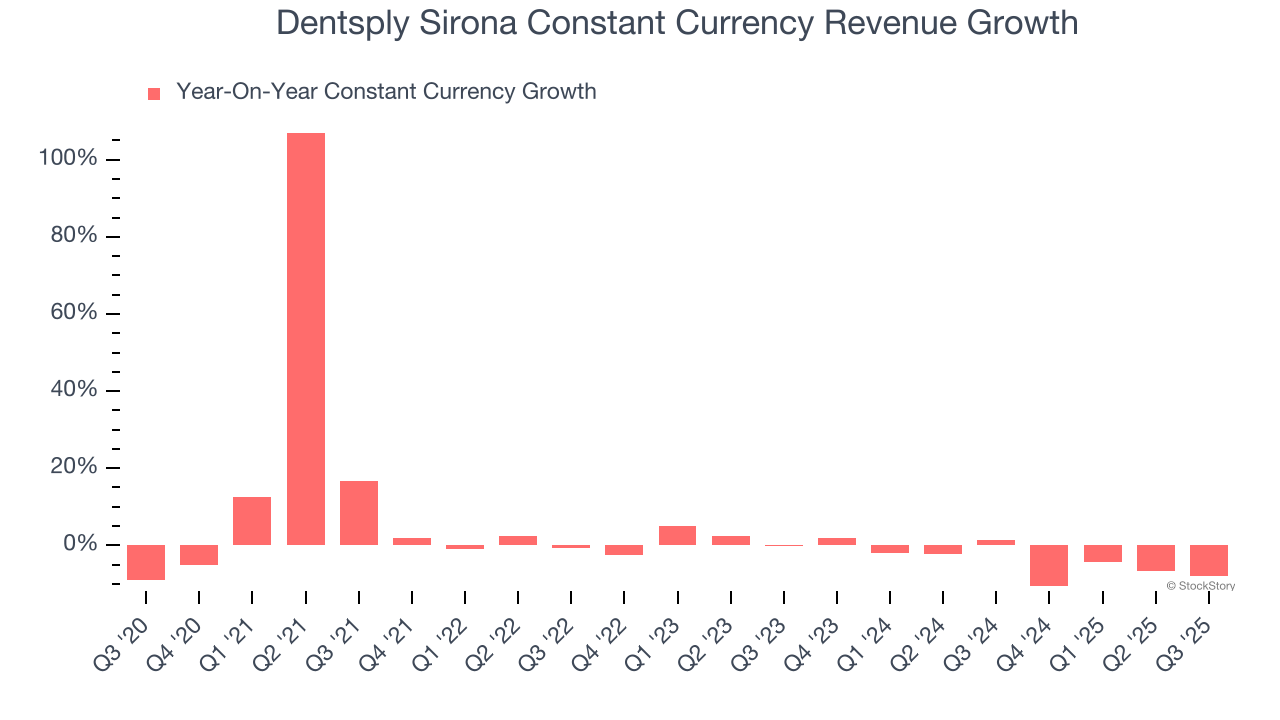

- Constant Currency Revenue fell 8% year on year (1.3% in the same quarter last year)

- Market Capitalization: $2.52 billion

"Third quarter results fell short of our expectations and reflect the operational and strategic challenges facing the business," said Dan Scavilla, President and Chief Executive Officer.

Company Overview

With roots dating back to 1877 when it introduced the first dental electric drill, Dentsply Sirona (NASDAQ: XRAY) manufactures and sells professional dental equipment, technologies, and consumable products used by dentists and specialists worldwide.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Dentsply Sirona’s sales grew at a tepid 1.4% compounded annual growth rate over the last five years. This was below our standards and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Dentsply Sirona’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 4% annually.

Dentsply Sirona also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 3.9% year-on-year declines. Because this number aligns with its normal revenue growth, we can see that Dentsply Sirona has properly hedged its foreign currency exposure.

This quarter, Dentsply Sirona’s revenue fell by 4.9% year on year to $904 million but beat Wall Street’s estimates by 0.5%.

Looking ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months. While this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Dentsply Sirona’s high expenses have contributed to an average operating margin of negative 7.3% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, Dentsply Sirona’s operating margin decreased by 35.6 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 19.5 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

Dentsply Sirona’s operating margin was negative 24.1% this quarter. The company's consistent lack of profits raise a flag.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

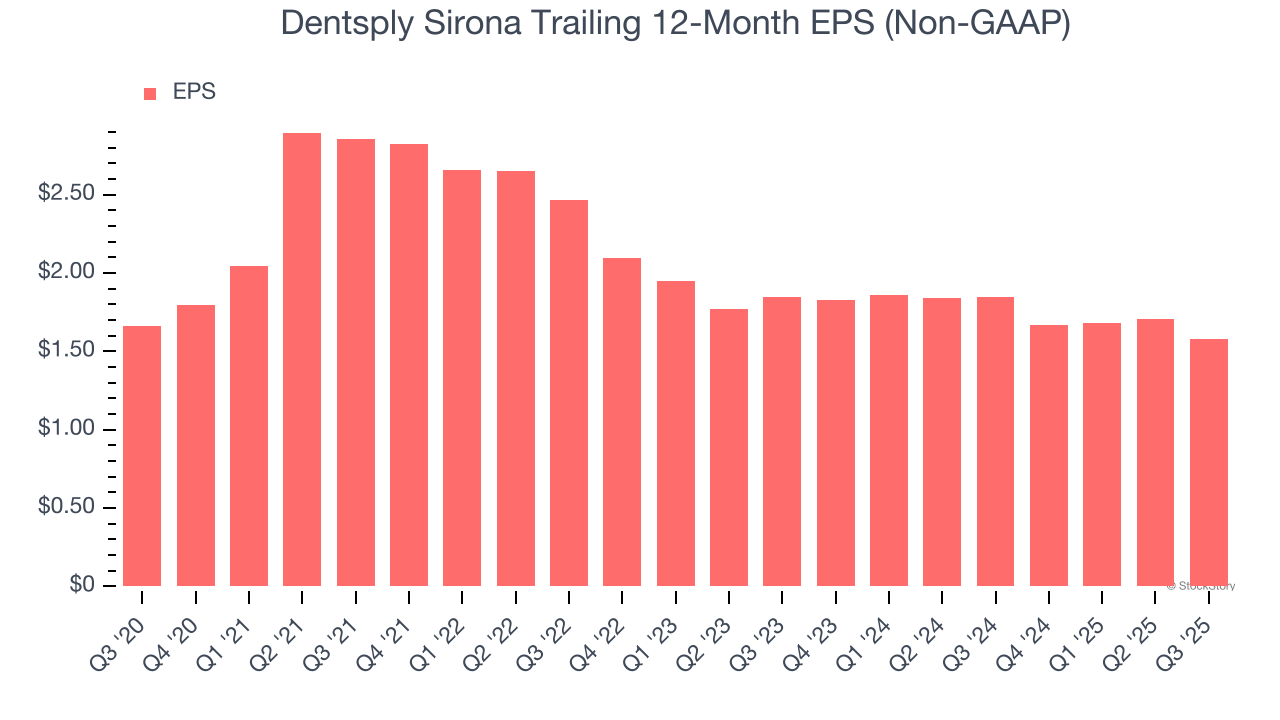

Dentsply Sirona’s flat EPS over the last five years was below its 1.4% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into the nuances of Dentsply Sirona’s earnings can give us a better understanding of its performance. As we mentioned earlier, Dentsply Sirona’s operating margin expanded this quarter but declined by 35.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q3, Dentsply Sirona reported adjusted EPS of $0.37, down from $0.50 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Dentsply Sirona’s full-year EPS of $1.58 to grow 24.4%.

Key Takeaways from Dentsply Sirona’s Q3 Results

It was good to see Dentsply Sirona narrowly top analysts’ revenue expectations this quarter. On the other hand, its full-year EPS guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 10% to $11.37 immediately following the results.

Dentsply Sirona’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.