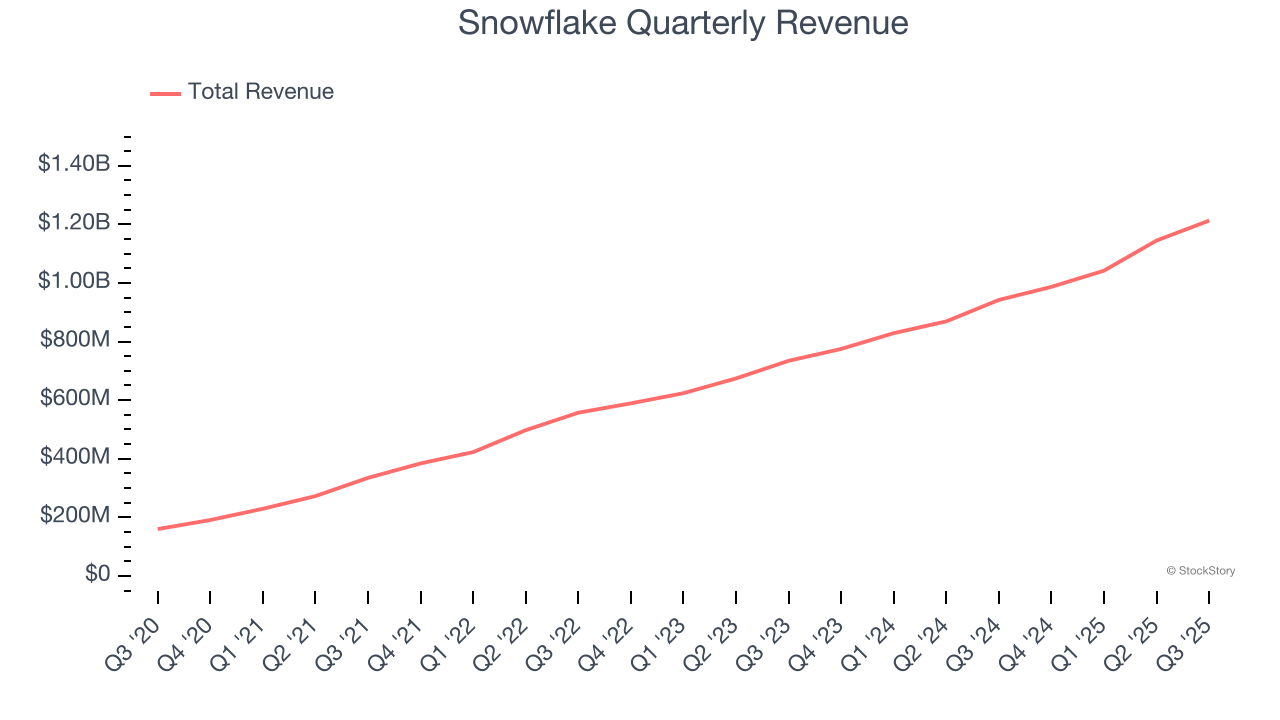

Cloud data platform provider Snowflake (NYSE: SNOW) reported revenue ahead of Wall Streets expectations in Q3 CY2025, with sales up 28.7% year on year to $1.21 billion. Its non-GAAP profit of $0.35 per share was 12.5% above analysts’ consensus estimates.

Is now the time to buy Snowflake? Find out by accessing our full research report, it’s free for active Edge members.

Snowflake (SNOW) Q3 CY2025 Highlights:

- Revenue: $1.21 billion vs analyst estimates of $1.18 billion (28.7% year-on-year growth, 2.4% beat)

- Adjusted EPS: $0.35 vs analyst estimates of $0.31 (12.5% beat)

- Adjusted Operating Income: $131.3 million vs analyst estimates of $108.2 million (10.8% margin, 21.3% beat)

- Product Revenue Guidance for Q4 CY2025 is $1.20 billion at the midpoint

- Operating Margin: -27.2%, up from -38.8% in the same quarter last year

- Free Cash Flow Margin: 9.4%, up from 5.1% in the previous quarter

- Customers: 688 customers paying more than $1 million annually

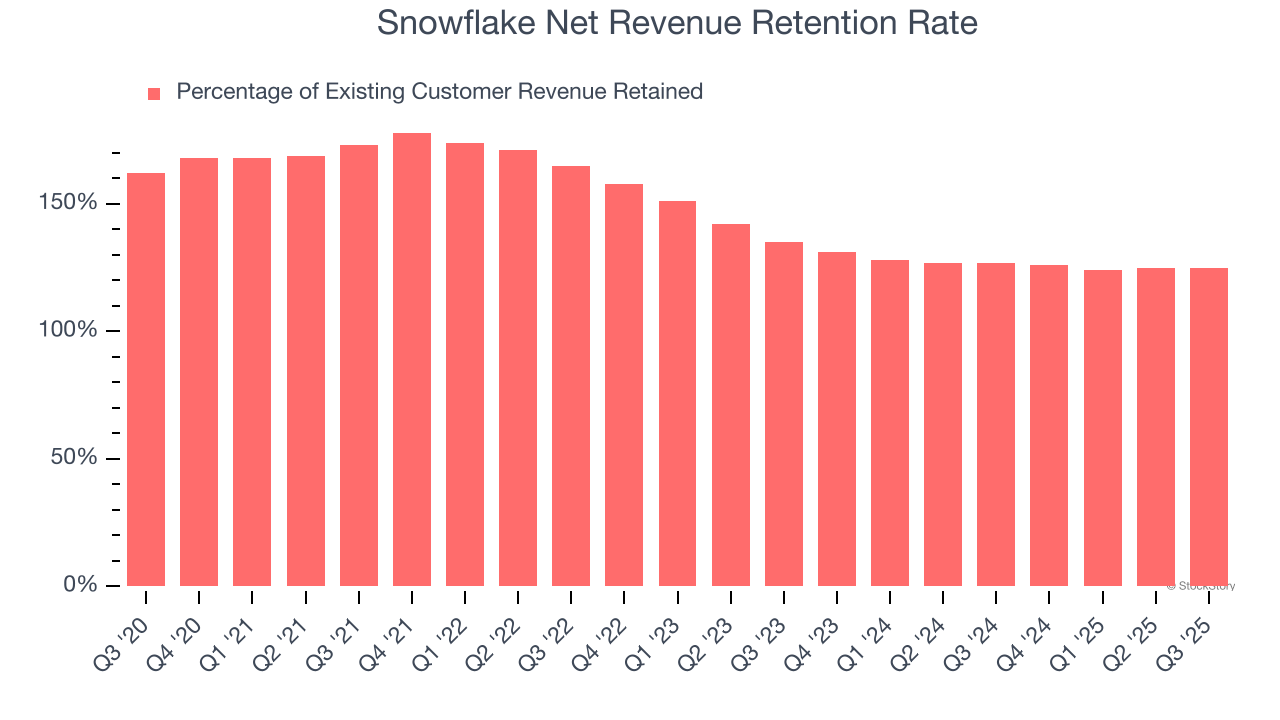

- Net Revenue Retention Rate: 125%, in line with the previous quarter

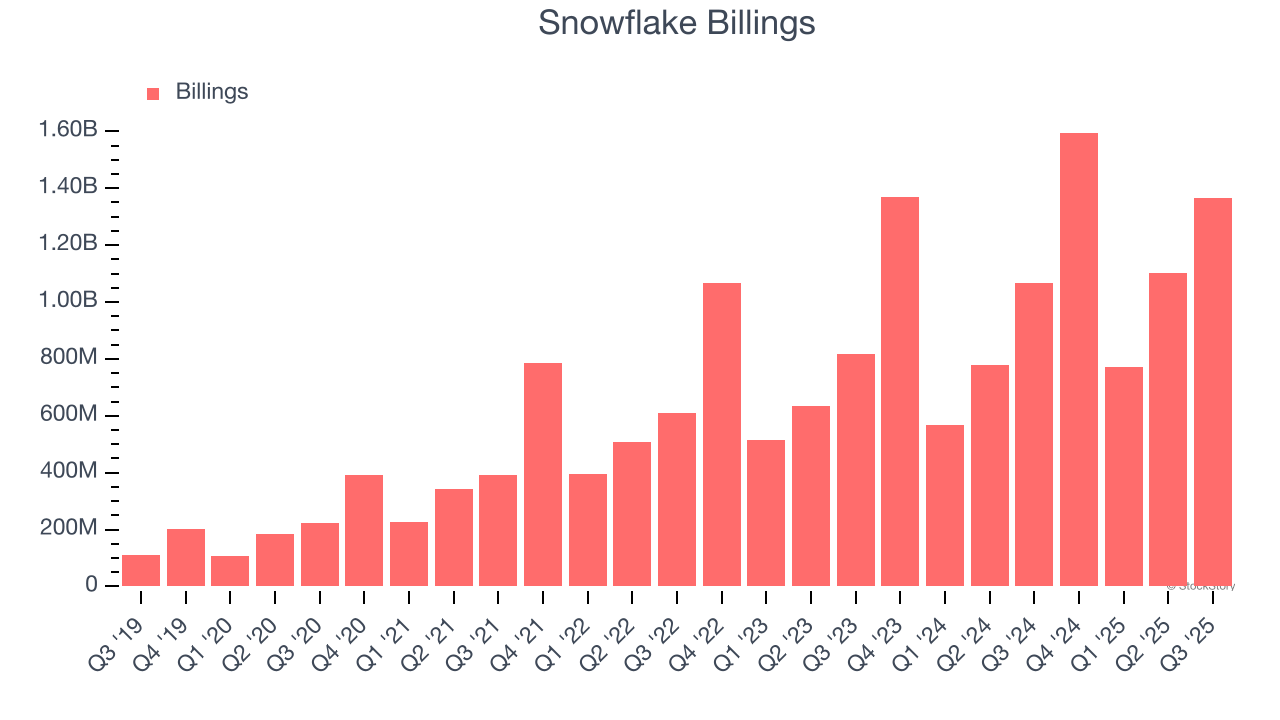

- Billings: $1.36 billion at quarter end, up 27.7% year on year

- Market Capitalization: $87.97 billion

Company Overview

Named after the unique architecture of its data warehouse which resembles a snowflake pattern, Snowflake (NYSE: SNOW) provides a cloud-based data platform that enables organizations to consolidate, analyze, and share data across multiple cloud providers.

Revenue Growth

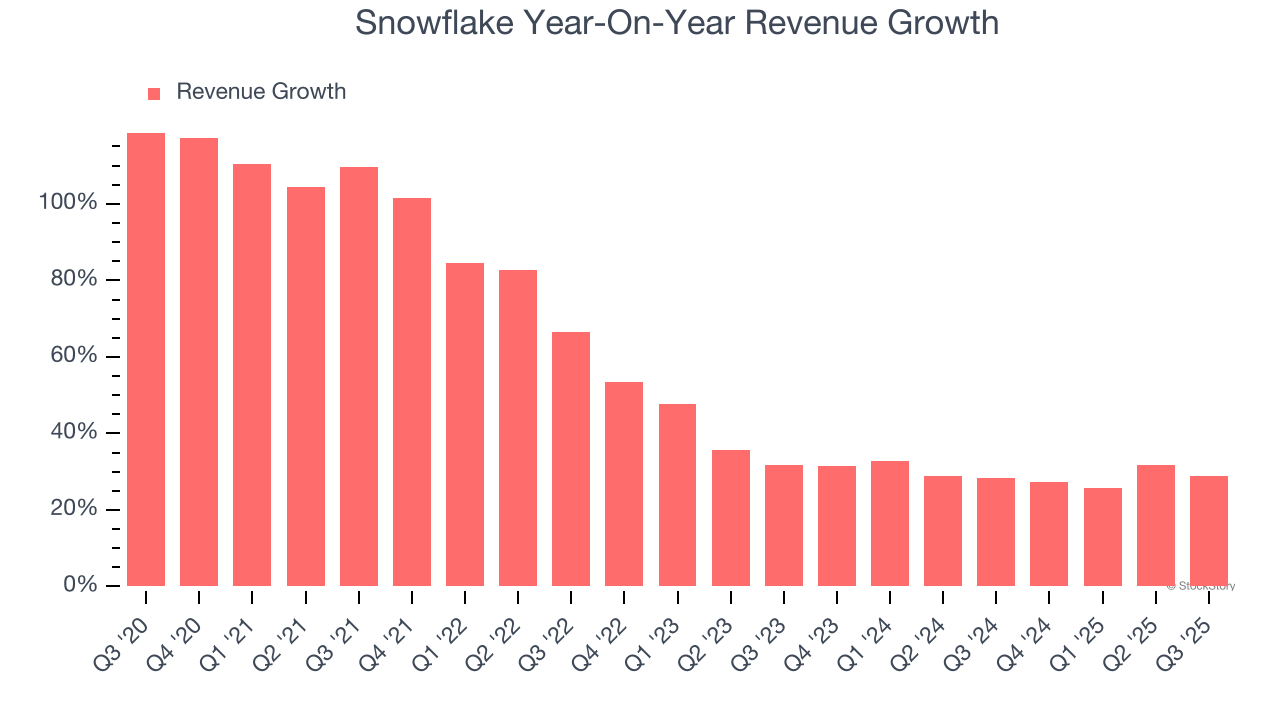

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Snowflake’s sales grew at an incredible 55.1% compounded annual growth rate over the last five years. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Snowflake’s annualized revenue growth of 29.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Snowflake reported robust year-on-year revenue growth of 28.7%, and its $1.21 billion of revenue topped Wall Street estimates by 2.4%.

Looking ahead, sell-side analysts expect revenue to grow 23.4% over the next 12 months, a deceleration versus the last two years. Still, this projection is commendable and implies the market is forecasting success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Snowflake’s billings punched in at $1.36 billion in Q3, and over the last four quarters, its growth was fantastic as it averaged 30.4% year-on-year increases. This performance aligned with its total sales growth, indicating robust customer demand. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Snowflake’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 125% in Q3. This means Snowflake would’ve grown its revenue by 25% even if it didn’t win any new customers over the last 12 months.

Snowflake has a good net retention rate, proving that customers are satisfied with its software and getting more value from it over time, which is always great to see.

Key Takeaways from Snowflake’s Q3 Results

It was encouraging to see Snowflake beat analysts’ revenue expectations this quarter. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 8.5% to $244.02 immediately after reporting.

Big picture, is Snowflake a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.