Thinking about investing in PepsiCo? PepsiCo (NASDAQ: PEP) is the world’s 2nd largest consumer food company behind Nestle. It is the US's largest consumer food company, growing domestically and internationally. It is an attractive stock for many reasons.

The company's deeply rooted history began with a pharmacy in New Bern, North Carolina, in 1898. Since then, the brand has become world-recognized and is the #2 soda brand behind Coca-Cola. The difference between PepsiCo today and then and PepsiCo and its largest competitor, The Coca-Cola Company (NYSE: KO), is diversification. Diversification efforts began in 1965 when the company merged with Frito-Lay and continue to this day.

PepsiCo is a diversified multinational packed food conglomerate focused on beverages, snacking, and breakfast. Its primary operating categories are PepsiCo Beverages North America, Frito-Lay North America, Quaker Foods North America, and the four international segments Europe, Latin America, AMS (Africa, Middle-East, and Southeast Asia), and APAC.

Growth in 2023 was underpinned by pricing actions, strength in core segments, and the international markets. Pricing actions resulted from inflationary pressures between 2021 and 2023, which aided margin and growth. The strongest segment was the emerging market in Latin America, with a 19% gain, followed by 7% growth in PepsiCo North America and a 5% increase in Frito-Lay North America.

The weakest segments in 2023 were AMS and Quaker Foods North America, but mitigating factors will turn these segments into tailwinds in 2024 and 2025. In Africa, results were impacted by discontinuing non-productive businesses that aided margin improvement. Operating profit increased 21% despite the 5% decline in revenue. Quaker Foods North America contracted by 2% due to tough comps to prior years caused by pantry-loading and social distancing. Segment growth is expected to return by the end of the current fiscal year.

Understanding PepsiCo's Business Model

PepsiCo business strategy operates on efficient management and brand loyalty. Efficient management includes a top-light executive structure aided by digitization and logistics improvements. Brand loyalty is driven by its diverse portfolio of well-loved brands, innovation, and customer engagement.

The company’s diverse brands include Pepsi and related beverages, Gatorade, Doritos, Fritos, and Quaker Oats. Products are delivered to consumers via numerous channels, including direct-to-store, warehouse distributors, digital, and “Other” channels. The primary business units focus on domestic and North American sales and international markets globally. PepsiCo products can be found in vending machines, retail food outlets, and food service establishments.

The company can drive growth via expanded markets, deepening penetration of existing markets, and product innovations. Product innovations focus on packaging and design, and the two factors that count most, flavor and new products. Among the many historical innovations is Crystal Pepsi.

Crystal Pepsi was a flop but provided deep insight into product innovation, including how to launch best and monetize new items. Other innovations include Gluten-Free labeling for Quaker Products and The Walking Taco. A Walking Taco is a single-serving bag of Fritos, Tostitos or other chips loaded with taco or salad toppings, turning a snack into a meal.

Financial Performance Review

[content-module:CompanyOverview|NASDAQ: PEP]

PepsiCo revenue growth topped 6% in 2023. This is down from double-digit levels the previous year but impacted by tough comps with the year earlier and the elasticity associated with rising prices. The company slipped into YOY contraction in Q4 2023 but is already expected to emerge from the slump. Growth is forecasted for Q1 2024 and the year, with the top-line projected to rise by a mid-single-digit figure and earnings to grow at double the pace.

PepsiCo financial performance is good and improving. PepsiCo widened its gross and operating margin for 2023 and is expected to improve performance again in 2024. The adjusted operating margin in 2023 was just over 13.0% compared to The Coca-Cola Company’s 21% and 7% average for consumer staples stocks. The Coca-Cola Company is a pure beverage player and can sustain higher margins.

PepsiCo financial health is good. The rock-solid balance sheet provides ample flexibility to invest in growth while returning capital to shareholders. At the end of 2023, the balance sheet highlights include the cash position nearly doubled, current and total assets up, and equity up nearly 8%. Capital returns include the dividend, increased for the 51st consecutive year, and share repurchases. Share repurchases are not robust, but they offset the dilutive impacts of share-based compensation and reduced the count by 0.3% on average last year.

PepsiCo is a highly-valued stock trading at 21X this year’s and 20X next year’s earnings, but it is also valuable for shareholders. The P/E aligns with The Coca-Cola Company; both trade below historical averages. PepsiCo’s P/E averaged over 25X over the last ten years, peaking above 30X during the pandemic.

Market Trends Impacting PepsiCo Stock

Industry competition is fierce for PepsiCo, but its diversified nature helps alleviate some of the impact. The company’s biggest competitor is The Coca-Cola Company, and their long-standing rivalry is more of a tailwind than not, boosting recognition and spurring consumers to drink. The two primary influences on the business today are industry normalization and inflation.

The consumer staples sector saw a significant surge in growth due to pantry-loading and social distancing that is only now returning to normalized levels. The post-COVID period is marked by slowing and sluggish growth, but a turning point is at hand. The tough comps are exiting the picture, paving the way for the industry to resume growth and for market leaders like PepsiCo to outperform.

Likewise, inflation impacted the business by squeezing margins, but the company flexed its considerable pricing power and sustained profit levels. The problem now is elasticity, offset by brand loyalty and growth efforts. The company is forecasting steady growth aligning with long-term targets for 2024, compounded by wider margins.

There is fear that consumers will be pinched in 2024, but the data does not support this. Wages grow above 4% on average monthly and underpin better-than-expected retail sales. Retail sales are up 0.7% in March and more than 1% in the first quarter. PepsiCo market trends are favorable.

Competitive Analysis

PepsiCo’s closest competitor is The Coca-Cola Company, but the comparison is imperfect. PepsiCo competitive advantage is its diversification. PepsiCo competes with The Coca-Cola Company domestically and internationally, but its business is far larger. Diversified PepsiCo brought in $10.95 billion in Q4, about 35% of what PepsiCo reported.

Breaking out the beverage segment and not including international sales, PepsiCo’s beverage business is roughly equal. Keurig Dr Pepper (NASDAQ: KDP) is also in the mix, but not a significant headwind for PepsiCo.

Packaged food competitors include Modelez (NASDAQ: MDLZ) and General Mills (NYSE: GIS). Both command significant brand appeal and loyalty, making growth in the North American segment difficult. Competition in international markets includes Kraft Heinz. Kraft Heinz (NASDAQ: KHC) is leaning into global markets as a source of growth. However, it focuses on flavors and meals more than snacks and beverages, so it only competes indirectly.

Future Outlook for PepsiCo Stock

[content-module:DividendStats|NASDAQ: PEP]

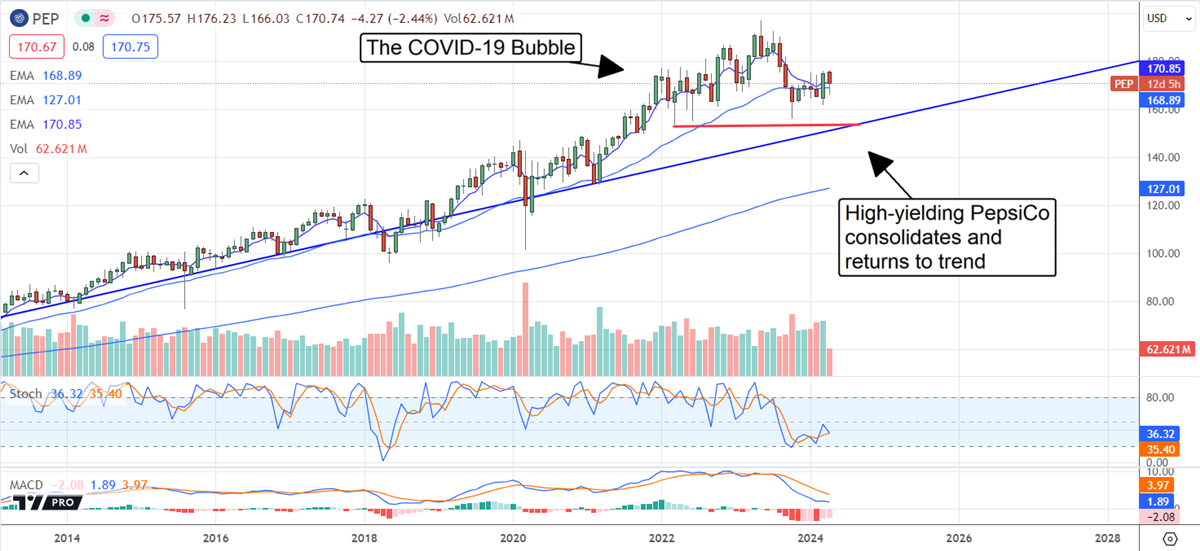

PepsiCo stock analysis shows the price was corrected in 2023 but is still well-supported by the market and in an uptrend. The uptrend is expected to continue due to the value-yield combination, projections for growth, and share repurchases. The stock trades at a historically low valuation while paying an above-average yield. The stock is also high-yielding at 3.0%, with shares near the long-term low.

The PepsiCo stock forecast is that price action may wallow near current levels in 2024 but should realign with the long-term trend line by the end of the year. The trend line should spur the market to upward movement.

There is some mixed analyst activity in the first four months of 2024, but the balance is bullish. Sentiment rose to Moderate Buy from Hold, and the price target remained steady—the consensus target forecasts a 10% upside, which puts the market near an all-time high. Because the company is growing and building shareholder value, analysts should lift their targets over time and drive the market to new heights.

Investment Recommendations

PepsiCo is a good buy for income and buy-and-hold investors. The company is a blue-chip quality consumer staple with the world’s second-largest operation. It still grows and widens margins, providing ample cash flow to sustain growth and pay distributions.

PepsiCo’s distribution is large, yielding about 3.0%, with shares near long-term lows and growing. PepsiCo is a Dividend King with more than 50 years of consecutive increases to its credit and the power to continue increasing for the foreseeable future.

PepsiCo is not without risks. It is in a tough industry with fierce competition, but its size, scale, and portfolio of brands mitigate the risk. There is never a guarantee that a stock’s price will appreciate. Still, this one trades at a discount to historical norms, near critical support at a significant uptrend line, with analysts' support. Analysts’ sentiment improved over the last six months and sees this market advancing at least 10%. The PepsiCo investment outlook is good.