As the Q3 earnings season wraps, let’s dig into this quarter’s best and worst performers in the water infrastructure industry, including Xylem (NYSE:XYL) and its peers.

Trends towards conservation and reducing groundwater depletion are putting water infrastructure and treatment products front and center. Companies that can innovate and create solutions–especially automated or connected solutions–to address these thematic trends will create incremental demand and speed up replacement cycles. On the other hand, water infrastructure and treatment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 5 water infrastructure stocks we track reported a satisfactory Q3. As a group, revenues were in line with analysts’ consensus estimates.

In light of this news, share prices of the companies have held steady as they are up 4.9% on average since the latest earnings results.

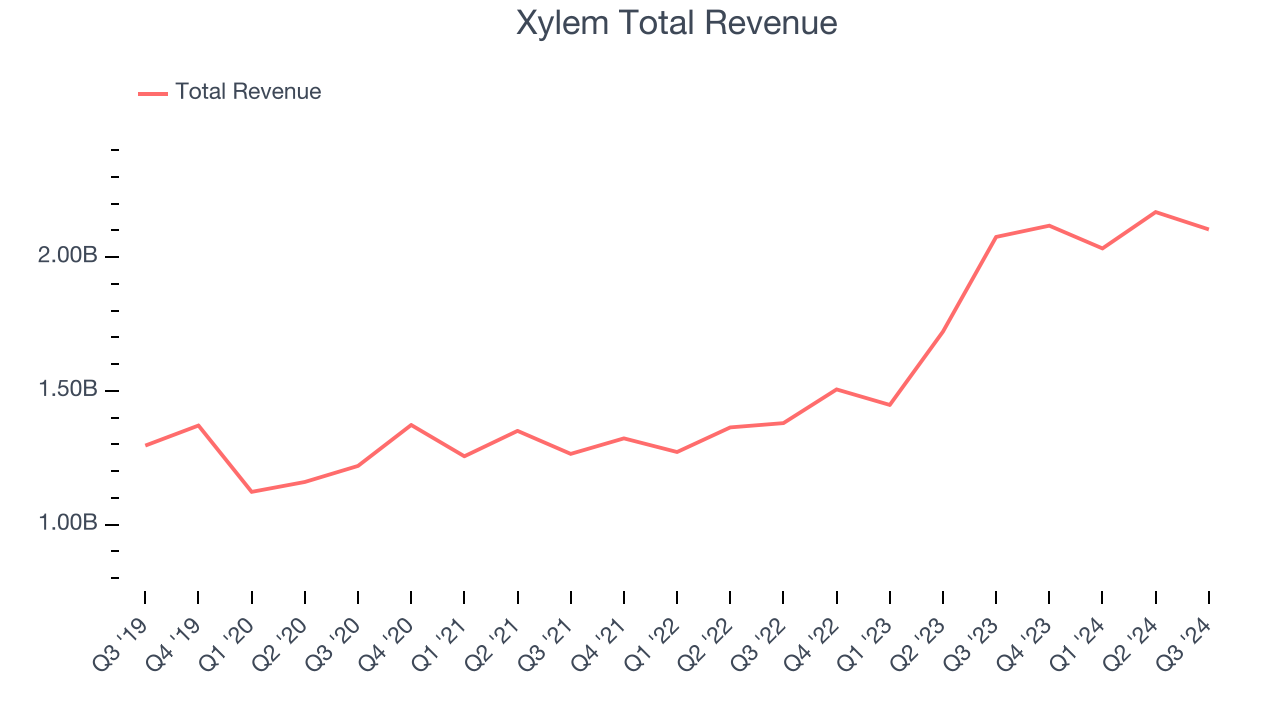

Xylem (NYSE:XYL)

Formed through a spinoff, Xylem (NYSE:XYL) manufactures and services engineered products across a wide variety of applications primarily in the water sector.

Xylem reported revenues of $2.10 billion, up 1.3% year on year. This print fell short of analysts’ expectations by 3.2%. Overall, it was a slower quarter for the company with a miss of analysts’ organic revenue and operating margin estimates.

“The team delivered strong results in the quarter, with earnings at the high end of guidance, and margin expansion beating our expectations,” said Matthew Pine, Xylem’s President and CEO.

Xylem delivered the weakest performance against analyst estimates, slowest revenue growth, and weakest full-year guidance update of the whole group. Unsurprisingly, the stock is down 6% since reporting and currently trades at $122.54.

Is now the time to buy Xylem? Access our full analysis of the earnings results here, it’s free.

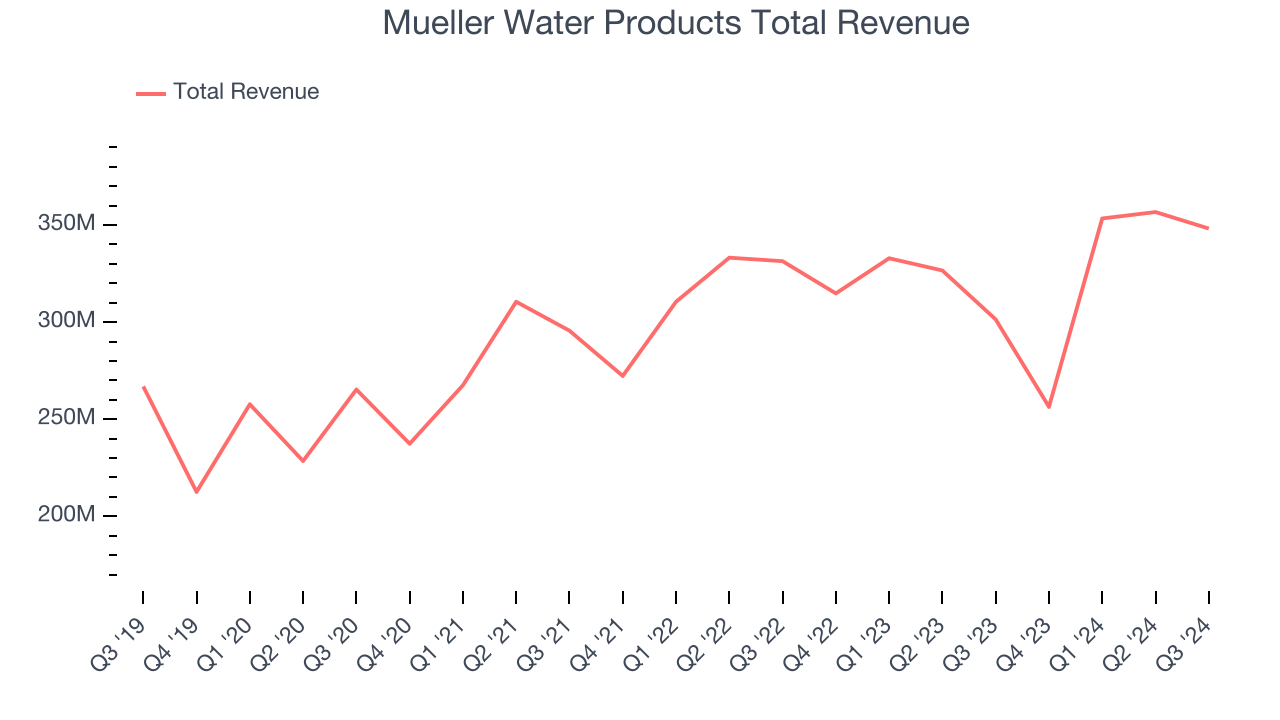

Best Q3: Mueller Water Products (NYSE:MWA)

As one of the oldest companies in the water infrastructure industry, Mueller (NYSE:MWA) is a provider of water infrastructure products and flow control systems for various sectors.

Mueller Water Products reported revenues of $348.2 million, up 15.5% year on year, outperforming analysts’ expectations by 6.5%. The business had a very strong quarter with an impressive beat of analysts’ organic revenue and EBITDA estimates.

Mueller Water Products achieved the biggest analyst estimates beat and fastest revenue growth among its peers. However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $24.15.

Is now the time to buy Mueller Water Products? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Tennant (NYSE:TNC)

As the world’s largest manufacturer of autonomous mobile robots, Tennant (NYSE:TNC) designs, manufactures, and sells cleaning products to various sectors.

Tennant reported revenues of $315.8 million, up 3.6% year on year, falling short of analysts’ expectations by 1.1%. It was a slower quarter as it posted a miss of analysts’ earnings and EBITDA estimates.

Interestingly, the stock is up 8.5% since the results and currently trades at $94.72.

Read our full analysis of Tennant’s results here.

Watts Water Technologies (NYSE:WTS)

Founded in 1874, Watts Water (NYSE:WTS) specializes in manufacturing water products and systems for residential, commercial, and industrial applications globally.

Watts Water Technologies reported revenues of $543.6 million, up 7.8% year on year. This print met analysts’ expectations. It was a satisfactory quarter as it also put up a decent beat of analysts’ operating margin estimates.

The stock is up 4.9% since reporting and currently trades at $207.24.

Read our full, actionable report on Watts Water Technologies here, it’s free.

Energy Recovery (NASDAQ:ERII)

Having saved far more than a trillion gallons of water, Energy Recovery (NASDAQ:ERII) provides energy recovery devices to the water treatment, oil and gas, and chemical processing sectors.

Energy Recovery reported revenues of $38.58 million, up 4.2% year on year. This number lagged analysts' expectations by 1.4%. Aside from that, it was a very strong quarter as it recorded an impressive beat of analysts’ earnings and EBITDA estimates.

The stock is up 11.1% since reporting and currently trades at $19.86.

Read our full, actionable report on Energy Recovery here, it’s free.

Market Update

As expected, the Federal Reserve cut its policy rate by 25bps (a quarter of a percent) in November 2024 after Donald Trump triumphed in the US Presidential election. This marks the central bank's second easing of monetary policy after a large 50bps rate cut two months earlier. Going forward, the markets will debate whether these rate cuts (and more potential ones in 2025) are perfect timing to support the economy or a bit too late for a macro that has already cooled too much. Adding to the degree of difficulty is a new Republican administration that could make large changes to corporate taxes and prior efforts such as the Inflation Reduction Act.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.