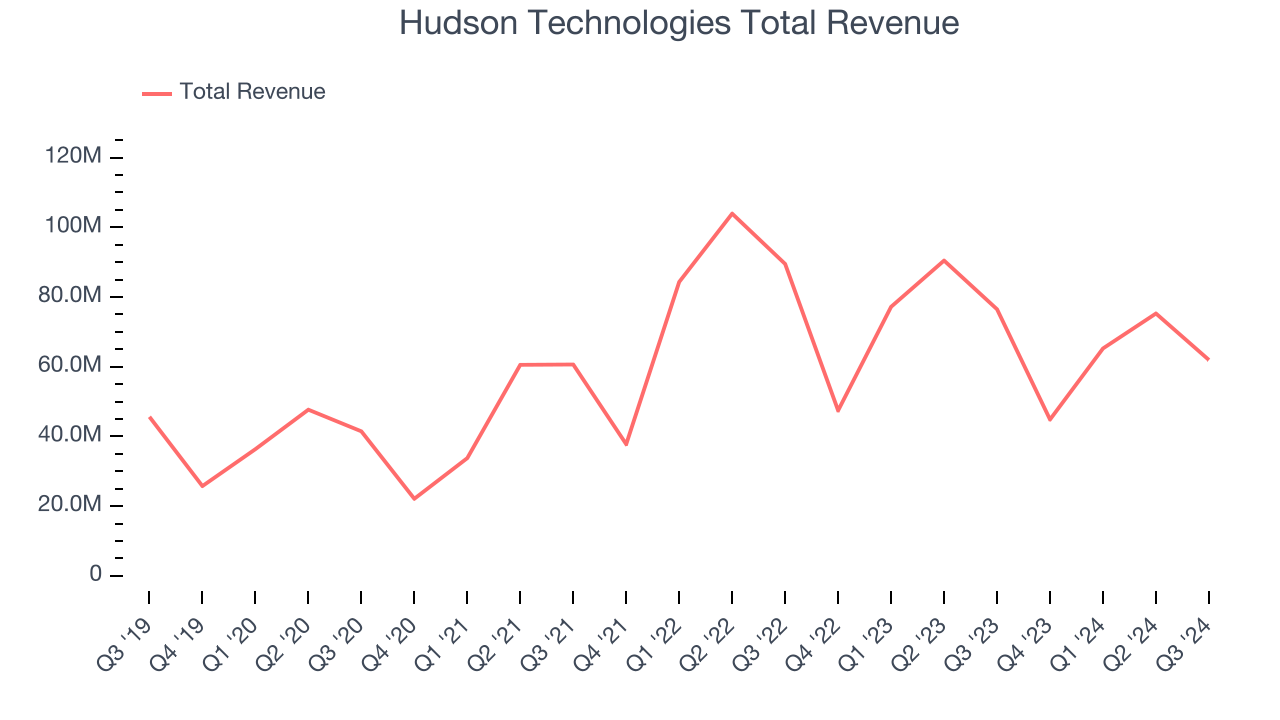

Refrigerant services company Hudson Technologies (NASDAQ:HDSN) fell short of the market’s revenue expectations in Q3 CY2024, with sales falling 19% year on year to $61.94 million. Its GAAP profit of $0.17 per share was 7.9% above analysts’ consensus estimates.

Is now the time to buy Hudson Technologies? Find out by accessing our full research report, it’s free.

Hudson Technologies (HDSN) Q3 CY2024 Highlights:

- Revenue: $61.94 million vs analyst estimates of $66.11 million (6.3% miss)

- EPS: $0.17 vs analyst estimates of $0.16 (7.9% beat)

- Gross Margin (GAAP): 25.7%, down from 40% in the same quarter last year

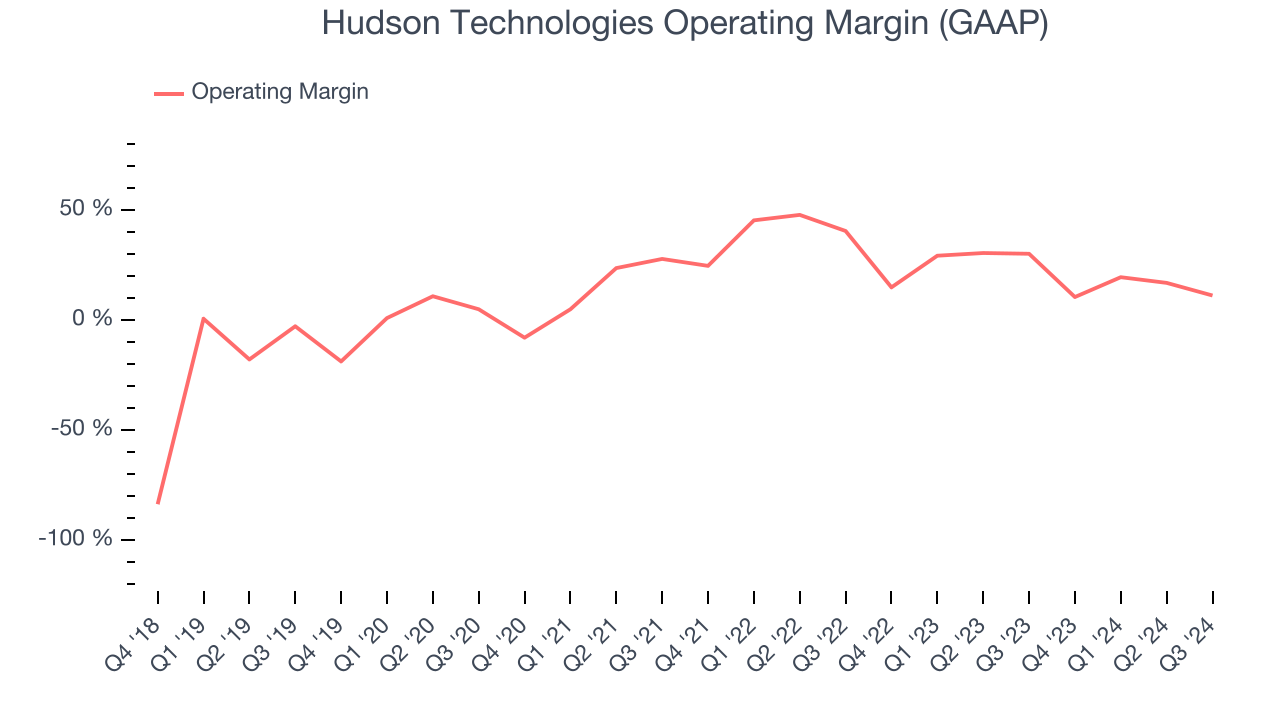

- Operating Margin: 11.3%, down from 30.2% in the same quarter last year

- Free Cash Flow Margin: 46.2%, up from 27.3% in the same quarter last year

- Market Capitalization: $337.8 million

Brian F. Coleman, President and Chief Executive Officer of Hudson Technologies commented, “Our third quarter results reflected continued pricing pressure that persisted for certain refrigerants throughout the 2024 cooling season. While disappointing in the near term, pricing trends are only one element of our business model and we remain confident in our long-term growth strategy to capitalize on the phasedown of HFC refrigerants and the expected corresponding growth in demand for reclaimed refrigerants. With our current visibility, we are adjusting our expectation for full year 2024 revenue, which we anticipate will be at the low end of the guidance range we previously provided, with full year gross margin of approximately 28%.

Company Overview

Founded in 1991, Hudson Technologies (NASDAQ:HDSN) specializes in refrigerant services and solutions, providing refrigerant sales, reclamation, and recycling.

Specialty Equipment Distributors

Historically, specialty equipment distributors have boasted deep selection and expertise in sometimes narrow areas like single-use packaging or unique lighting equipment. Additionally, the industry has evolved to include more automated industrial equipment and machinery over the last decade, driving efficiencies and enabling valuable data collection. Specialty equipment distributors whose offerings keep up with these trends can take share in a still-fragmented market, but like the broader industrials sector, this space is at the whim of economic cycles that impact the capital spending and manufacturing propelling industry volumes.

Sales Growth

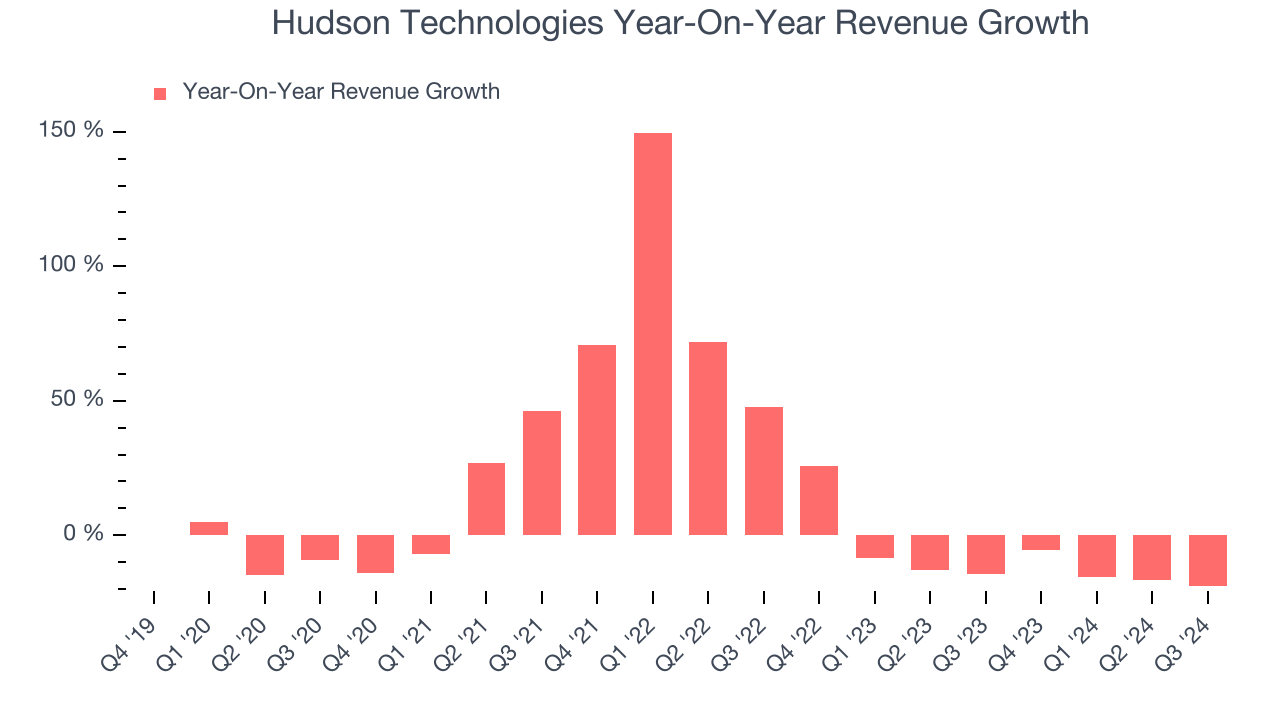

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Hudson Technologies grew its sales at a decent 8.8% compounded annual growth rate. This is a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Hudson Technologies’s recent history marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 11.5% over the last two years.

This quarter, Hudson Technologies missed Wall Street’s estimates and reported a rather uninspiring 19% year-on-year revenue decline, generating $61.94 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 11.1% over the next 12 months, an improvement versus the last two years. This projection is commendable and illustrates the market thinks its newer products and services will spur faster growth.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling them, and, most importantly, keeping them relevant through research and development.

Hudson Technologies has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 24.1%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Hudson Technologies’s annual operating margin rose by 13.2 percentage points over the last five years, showing its efficiency has meaningfully improved.

In Q3, Hudson Technologies generated an operating profit margin of 11.3%, down 19 percentage points year on year. Since Hudson Technologies’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

Analyzing revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

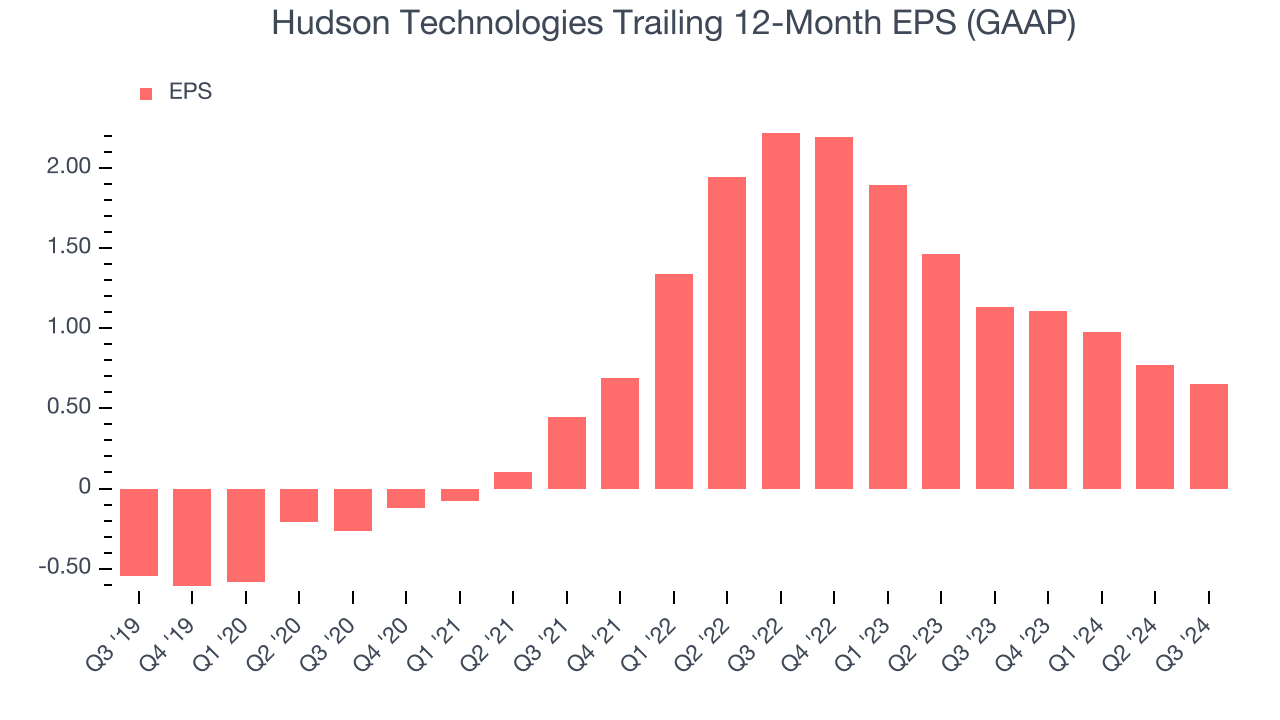

Hudson Technologies’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Hudson Technologies, its EPS declined by more than its revenue over the last two years, dropping 45.9%. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Diving into the nuances of Hudson Technologies’s earnings can give us a better understanding of its performance. Hudson Technologies’s operating margin has declined by 29.3 percentage points over the last two years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q3, Hudson Technologies reported EPS at $0.17, down from $0.29 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 7.9%. Over the next 12 months, Wall Street expects Hudson Technologies’s full-year EPS of $0.65 to grow by 17.4%.

Key Takeaways from Hudson Technologies’s Q3 Results

It was good to see Hudson Technologies beat analysts’ EPS expectations this quarter. On the other hand, its revenue missed. Overall, this was a weaker quarter. The stock traded down 4.4% to $7.26 immediately following the results.

The latest quarter from Hudson Technologies’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.