In a sliding market, Seagate Technology has defied the odds, trading up to $123.86 per share. Its 26.9% gain since December 2024 has outpaced the S&P 500’s 1.9% drop. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Seagate Technology, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Seagate Technology Not Exciting?

Despite the momentum, we don't have much confidence in Seagate Technology. Here are three reasons why we avoid STX and a stock we'd rather own.

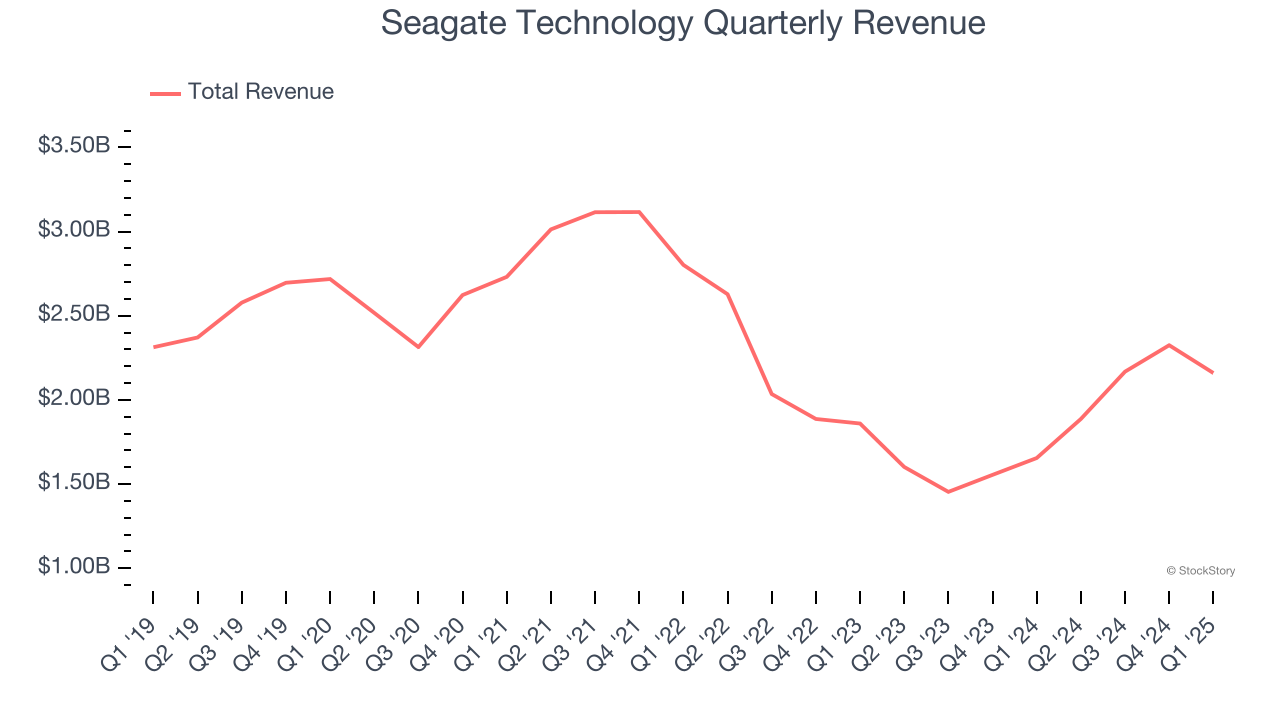

1. Revenue Spiraling Downwards

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Seagate Technology struggled to consistently generate demand over the last five years as its sales dropped at a 3.8% annual rate. This was below our standards and signals it’s a lower quality business. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

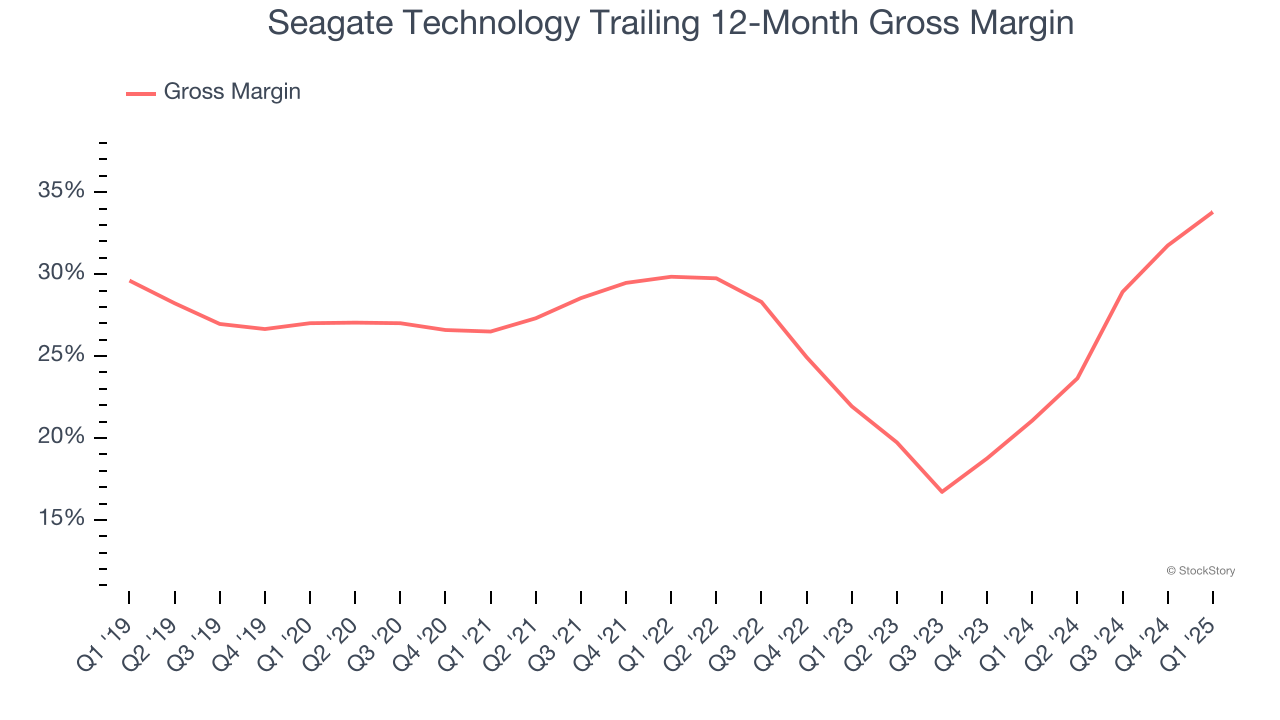

2. Low Gross Margin Reveals Weak Structural Profitability

Gross profit margin is a key metric to track because it shows how much money a semiconductor company gets to keep after paying for its raw materials, manufacturing, and other input costs.

Seagate Technology’s gross margin is one of the worst in the semiconductor industry, signaling it operates in a competitive market and lacks pricing power. As you can see below, it averaged a 28.4% gross margin over the last two years. That means Seagate Technology paid its suppliers a lot of money ($71.59 for every $100 in revenue) to run its business.

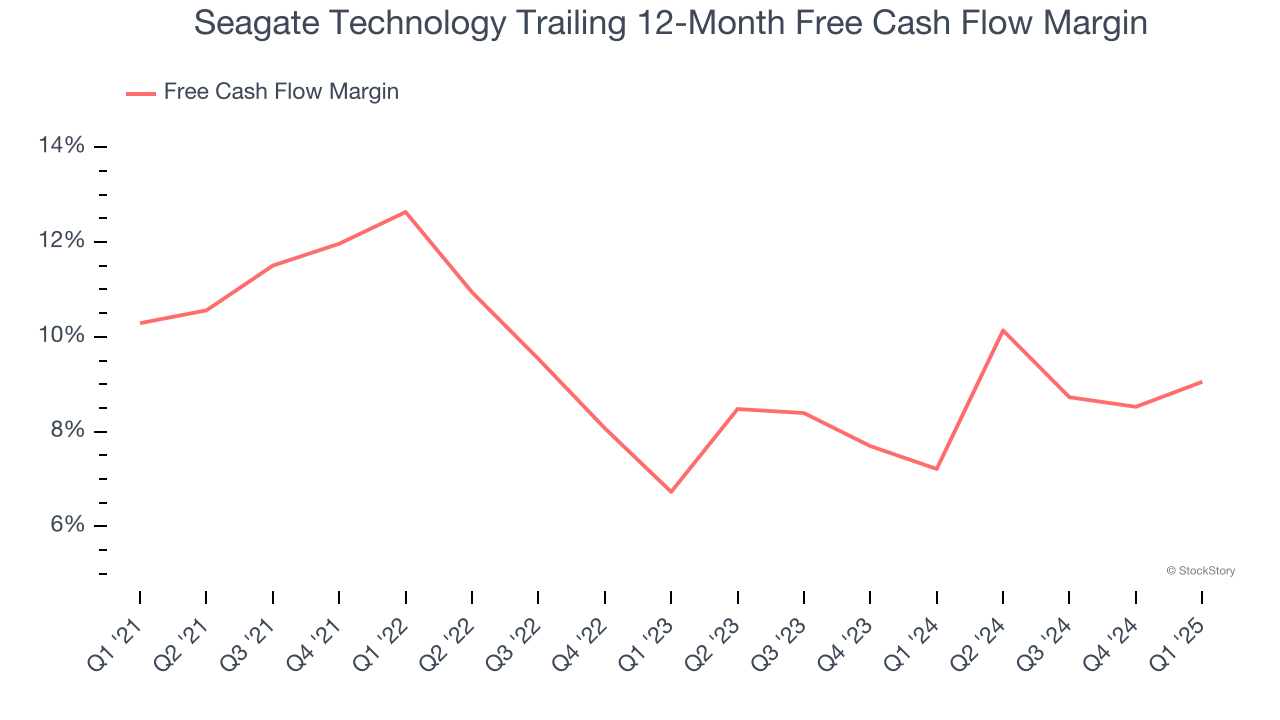

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Seagate Technology has shown weak cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 8.3%, subpar for a semiconductor business.

Final Judgment

Seagate Technology isn’t a terrible business, but it doesn’t pass our bar. With its shares beating the market recently, the stock trades at 13.8× forward P/E (or $123.86 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward a dominant Aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.