The AI buildout around Alphabet's Google (GOOG) (GOOGL) ecosystem is still picking up speed. Broadcom (AVGO) is deepening its long-term partnership with Google to make advanced chips, including hardware tied to Google TPUs, while Anthropic has lined up about 3.5 gigawatts of computing capacity tied to Google’s processors.

On top of that, Alphabet’s 2026 capital spending could reach $175–185 billion, with a big chunk going into AI-focused data centers, which will ripple through both chip suppliers and the cloud side of the business.

In that setting, Alphabet is pushing even harder on its own hardware. Google has just unveiled two 8th‑generation TPUs at a Las Vegas event, as it tries to handle growing demand from Google DeepMind and paying cloud customers. Management has already said most of its higher capex is aimed at AI compute and cloud capacity, and recent updates showed Google Cloud revenue growing at a strong double‑digit pace with a rising backlog, giving Google a much larger base where new hardware like these TPUs can actually show up in the numbers.

Given that level of spending, the new chip deals, and fresh in-house TPUs, will these 8th‑generation chips really move Google’s stock, or just raise the cost of staying in the game?

The Numbers Behind the AI Spending Surge

Alphabet runs a broad business built on search, ads, cloud services, and now a growing push into its own chips and data center hardware.

The stock has been on a strong run. Up 118.64% over the past 12 months, and 8.51% so far this year.

That shows up in the valuation too, with a forward P/E of 28.81 times, more than double the sector average of 13.79 times, so the market is clearly betting on more growth from its AI and cloud spending.

Income investors get a smaller slice for now. Alphabet’s dividend yield is 0.25%, with the latest payout at $0.210 on March 9, 2026, a forward payout ratio of 7.60%, and only one year of dividend increases, as most cash is being plowed back into the business. You can see that in the latest quarter.

Q4 CY2025 revenue hit $113.8 billion and beat forecasts, and EPS of $2.82 also came in ahead of expectations. Google Cloud was the main bright spot, even though the line items look odd on paper, and operating metrics showed how much demand is building. The operating margin held at 31.6%, but free cash flow margin slipped to 21.6% as spending picked up, with capex expected to jump to $175–$185 billion in 2026 as Alphabet leans hard into new infrastructure like its latest TPUs.

The Engines Powering Alphabet’s AI Push

Alphabet is widening its reach into government work, holding talks to bring its Gemini models into classified U.S. Department of Defense systems for lawful classified uses, with clear limits on things like domestic mass surveillance and fully autonomous weapons. It fits with the Pentagon’s push to use more software to cut costs and run operations more efficiently, and it puts Google closer to the center of defense tech decisions.

On the consumer side, the multi-year deal with Apple (AAPL) is aimed at doing something similar on a massive scale. Apple picked Gemini and Google Cloud to power new AI features across its ecosystem, including Siri, after reviewing other options, and that partnership helped Alphabet cross the $4 trillion market cap mark, showing how valuable this demand can be.

Under the hood, Alphabet is also looking at going deeper on its own chips through a possible tie-up with Marvell (MRVL), where they’d work on a memory processing unit that supports TPU workloads and a separate inference-focused TPU. That would give Google tighter control over performance and costs and reduce how much it relies on outside chip suppliers.

What the Street Thinks and What Comes Next

For Q1 2026, analysts are looking for EPS of $2.64, down from $2.81 a year ago, so they’re bracing for about a 6.05% decline. After that, they expect things to pick up: Q2 2026 EPS is pegged at $2.80, up 21.21% from $2.31 in the same quarter last year. For the full year, the Street sees 2026 EPS at $11.57 versus $10.81 in 2025 (about 7.03% growth).

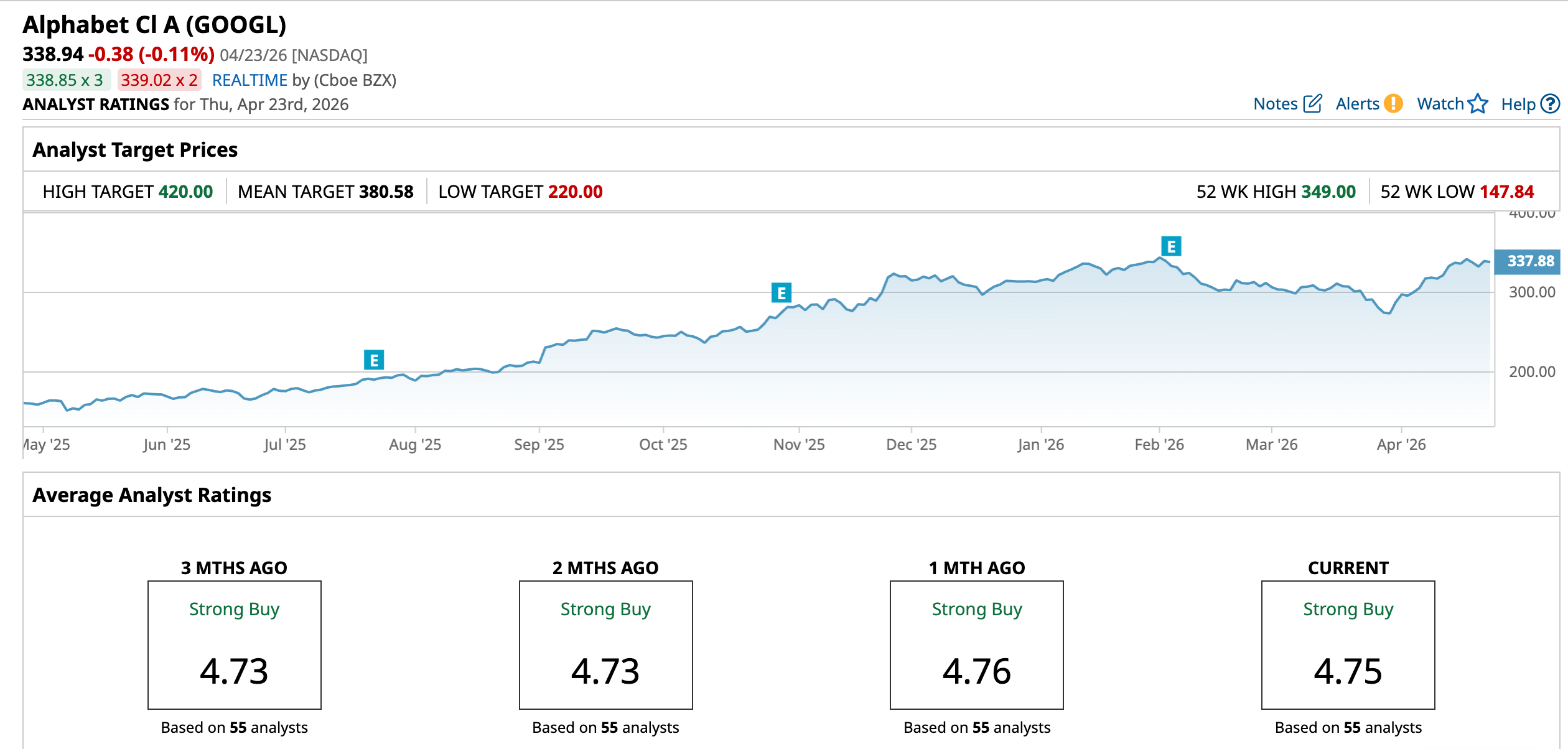

Wells Fargo’s Ken Gawrelski is leaning into that story. He raised his price target to $397 and kept an “Overweight” rating, pointing mainly to Google Cloud, where he expects a strong lift helped by a TPU licensing deal with Broadcom (AVGO) and the acquisition of Wiz.

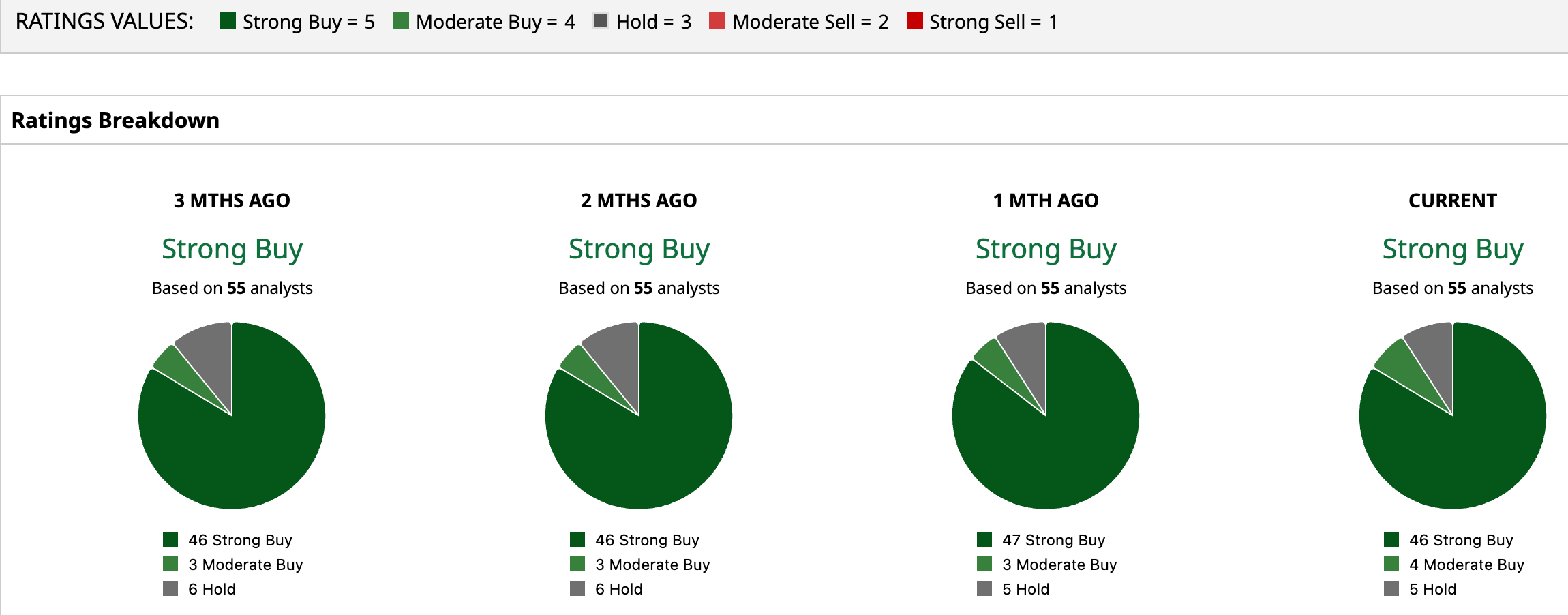

Overall, all 55 analysts tracked rate the stock a consensus “Strong Buy”, and the average target of $380.58 suggests roughly 12.3% upside from recent levels.

Conclusion

Given the scale of Alphabet’s AI buildout, the new 8th‑generation TPUs look less like a speculative side bet and more like the hardware spine of its next earnings leg. Between surging Google Cloud demand, potential government and enterprise AI contracts, and a Street that’s modeling steady EPS acceleration and assigning a “Strong Buy” consensus, these chips should help support both revenue growth and margin leverage over the next few years rather than simply bloating capex. In that context, I think the stock is more likely to grind higher than break down from here, with AI execution and cloud traction nudging shares toward the upper end of current price targets over time.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart