The artificial intelligence (AI) boom is forcing investors to rethink where real value is being created. Is it the flashy chatbot makers, or the infrastructure quietly powering them behind the scenes? Increasingly, the answer is the latter.

That shift is why semiconductor stocks have surged — but it also raises a bigger question: what if one of the largest chip companies isn’t even being valued like one? That’s exactly the case with Amazon (AMZN), whose in-house silicon business is scaling faster than most investors realize.

A $50 Billion Chip Business, If You Look Closely

Amazon stock has delivered a 14% return year-to-date (YTD), well ahead of the S&P 500's ($SPX) roughly 5% gain and slightly ahead of its sector. That steadiness matters. While many AI stocks have swung sharply on earnings, Amazon has quietly benefited from improving Amazon Web Services (AWS) margins and cost discipline. Investors are rewarding consistency, but they may not yet be pricing in Amazon’s fastest-growing segment.

Here’s what the numbers tell us. Amazon’s custom silicon — including Graviton CPUs and Trainium AI chips — is already generating a $20 billion annual revenue run rate according to CEO Andy Jassy on the latest earnings call. But that figure only reflects chips monetized through AWS EC2. The real number is higher.

If Amazon sold chips directly, Jassy says the run rate would approach $50 billion. That means it would be ahead of Advanced Micro Devices (AMD), which had $34.6 billion in 2025 revenue. It also puts Amazon in line with Intel (INTC), which saw $52.9 billion in 2025 revenue, and within reach of Broadcom (AVGO), which saw $63.9 billion. With Amazon’s chip segment growing at triple-digit rates, it could surpass Broadcom, which saw 24% year-over-year (YOY) sales growth.

Jassy also recently disclosed that two large AWS customers asked to buy out all CPU capacity for 2026. Amazon declined in order to avoid crowding out other customers. That’s not a demand issue — it’s a capacity constraint.

Meta Platforms, OpenAI, and Anthropic Signal What’s Next

Customer adoption is where the story clicks. Meta Platforms (META) just agreed to use Amazon’s Graviton CPUs for AI workloads — a notable shift for a company that builds much of its own infrastructure. Meanwhile, Amazon’s Trainium chips are already committed to OpenAI and Anthropic for training and inference.

These aren’t experimental users. They’re among the largest AI builders in the world.

Amazon’s advantage is structural. It doesn’t sell chips — it sells computing powered by those chips. That creates a recurring revenue model instead of one-time hardware sales, giving it a compounding edge over traditional semiconductor companies.

Amazon's Valuation Still Misses the Chip Angle

Amazon trades at a forward price-to-earnings (P/E) ratio of 32.9 times. That reflects AWS growth and retail stabilization, but not a standalone chip business of this scale. If even a portion of that implied $50 billion silicon operation were valued like AMD or Broadcom, it could account for a meaningful slice of Amazon’s market value.

Granted, Amazon isn’t a pure-play chip stock. But that diversification also reduces risk while giving investors exposure to one of the fastest-growing areas in tech.

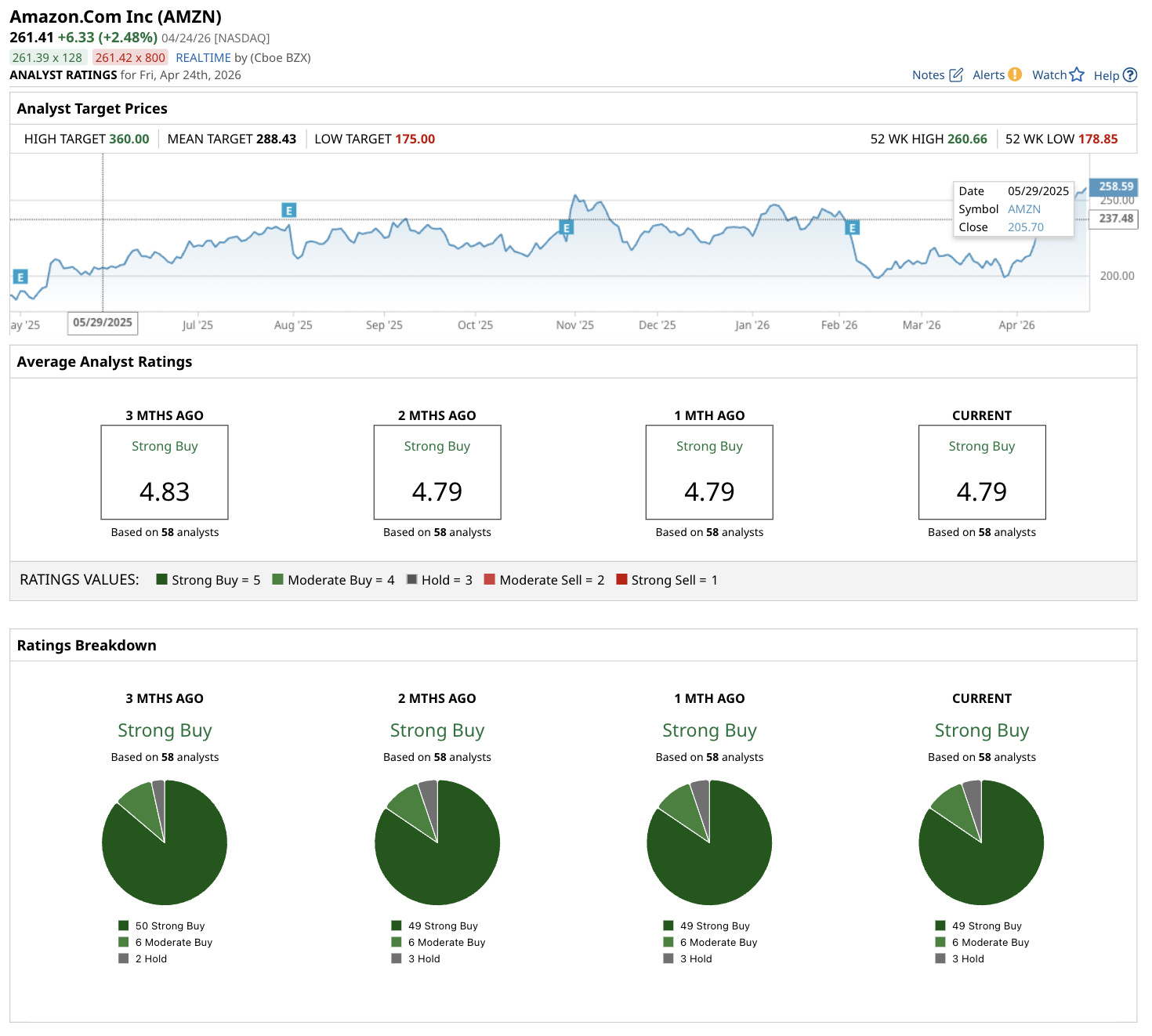

What Do Analysts Think About AMZN Stock?

Wall Street maintains a consensus “Strong Buy” rating on Amazon. Out of 58 analysts with coverage, 49 analysts have a "Strong Buy" rating, six have a "Moderate Buy," and three have a "Hold" rating.

The mean price target of $289.20 implies potential upside of 10% from current levels. Notably, Amazon's analyst estimates are driven largely by AWS and advertising, suggesting the chip story may still be underappreciated.

The Bottom Line

Amazon isn’t just participating in AI infrastructure — it’s becoming a core supplier. With a chip business that could rival Intel in scale and is growing at explosive rates, the market may be undervaluing what AMZN stock is becoming.

In short, this looks less like a e-commerce giant with a cloud arm and more like an AI infrastructure powerhouse hiding in plain sight.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart