Wrapping up Q3 earnings, we look at the numbers and key takeaways for the semiconductor manufacturing stocks, including Teradyne (NASDAQ: TER) and its peers.

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers, and data storage. The need for technologies like artificial intelligence, 5G networks, and smart cars is also creating the next wave of growth for the industry. Keeping up with this dynamism requires new tools that can design, fabricate, and test chips at ever smaller sizes and more complex architectures, creating a dire need for semiconductor capital manufacturing equipment.

The 14 semiconductor manufacturing stocks we track reported a very strong Q3. As a group, revenues beat analysts’ consensus estimates by 3.3% while next quarter’s revenue guidance was 0.6% below.

Luckily, semiconductor manufacturing stocks have performed well with share prices up 13.6% on average since the latest earnings results.

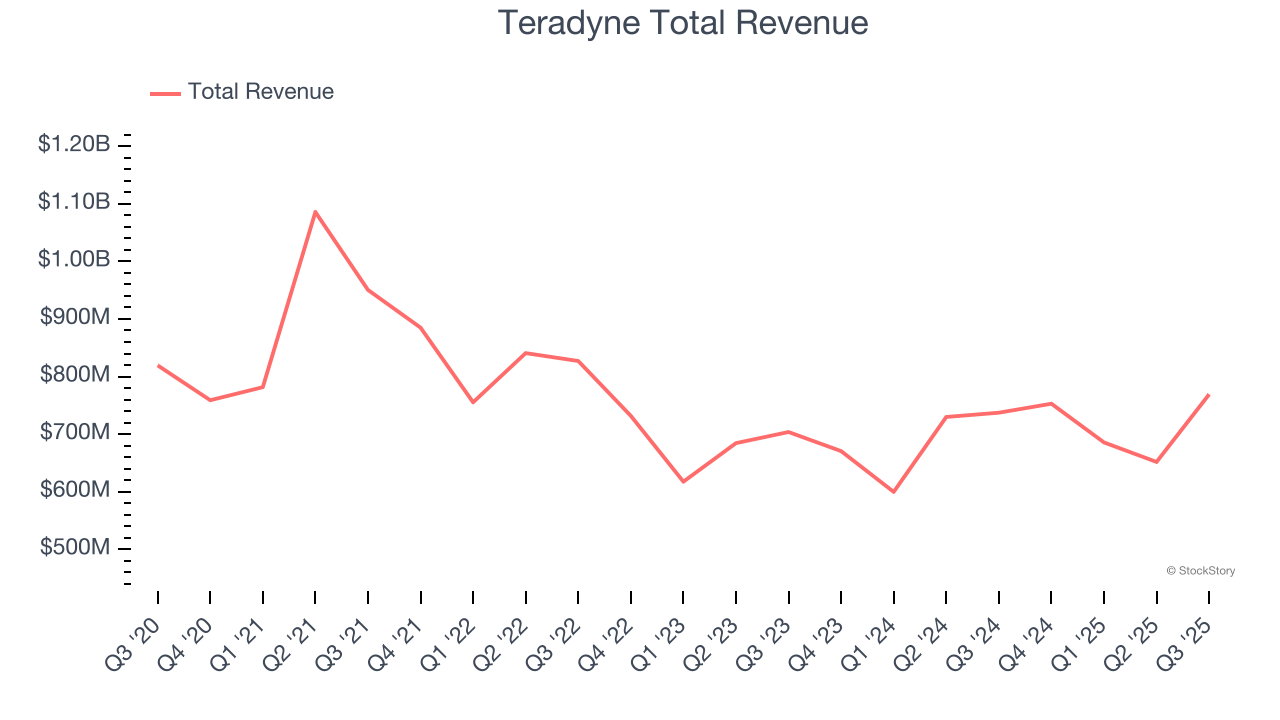

Best Q3: Teradyne (NASDAQ: TER)

Sporting most major chip manufacturers as its customers, Teradyne (NASDAQ: TER) is a US-based supplier of automated test equipment for semiconductors as well as other technologies and devices.

Teradyne reported revenues of $769.2 million, up 4.3% year on year. This print exceeded analysts’ expectations by 3.3%. Overall, it was a stunning quarter for the company with an impressive beat of analysts’ adjusted operating income estimates and revenue guidance for next quarter exceeding analysts’ expectations.

“Our Semiconductor Test Group delivered third quarter sales that exceeded expectations, driving company sales and profit to the high end of our Q3 guidance range,” said Teradyne CEO, Greg Smith.

Interestingly, the stock is up 34.6% since reporting and currently trades at $194.35.

Is now the time to buy Teradyne? Access our full analysis of the earnings results here, it’s free for active Edge members.

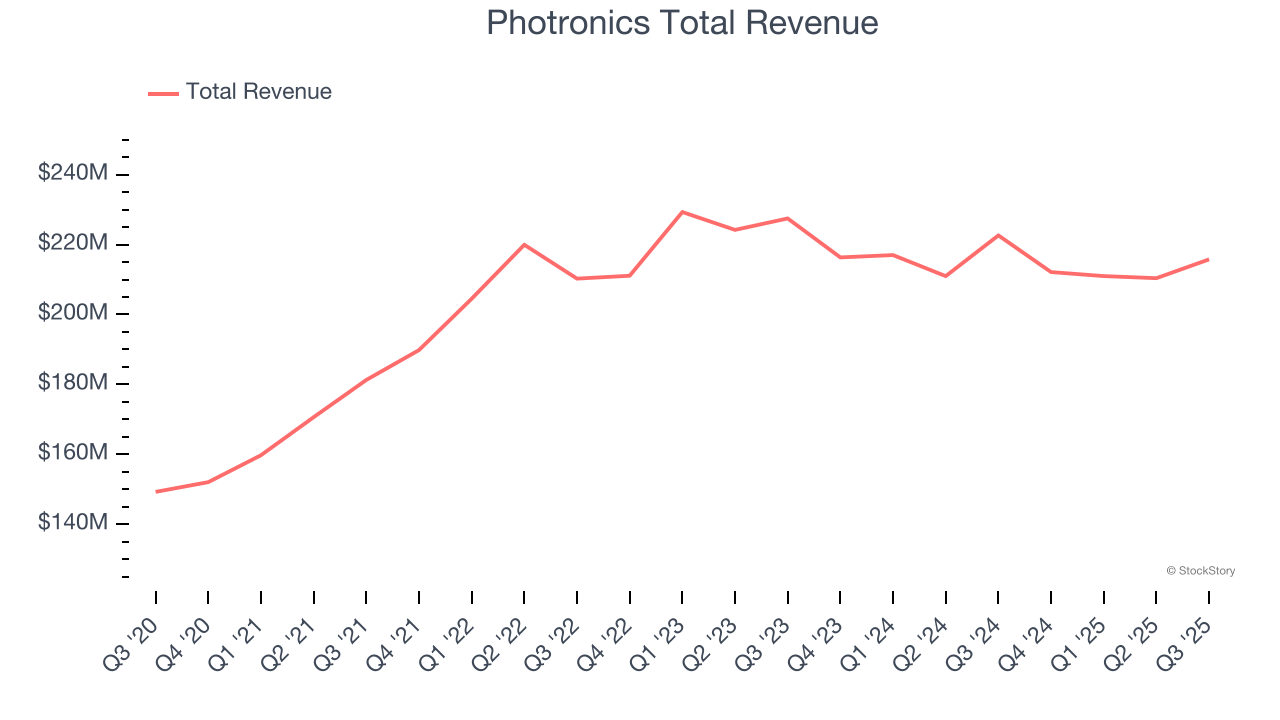

Photronics (NASDAQ: PLAB)

Sporting a global footprint of facilities, Photronics (NASDAQ: PLAB) is a manufacturer of photomasks, templates used to transfer patterns onto semiconductor wafers.

Photronics reported revenues of $215.8 million, down 3.1% year on year, outperforming analysts’ expectations by 5.5%. The business had an exceptional quarter with a beat of analysts’ EPS estimates and revenue guidance for next quarter exceeding analysts’ expectations.

The market seems happy with the results as the stock is up 41.1% since reporting. It currently trades at $36.25.

Is now the time to buy Photronics? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: Entegris (NASDAQ: ENTG)

With fabs representing the company’s largest customer type, Entegris (NASDAQ: ENTG) supplies products that purify, protect, and generally ensure the integrity of raw materials needed for advanced semiconductor manufacturing.

Entegris reported revenues of $807.1 million, flat year on year, exceeding analysts’ expectations by 0.6%. Still, it was a slower quarter as it posted revenue guidance for next quarter missing analysts’ expectations significantly and EPS in line with analysts’ estimates.

As expected, the stock is down 5% since the results and currently trades at $89.78.

Read our full analysis of Entegris’s results here.

Marvell Technology (NASDAQ: MRVL)

Moving away from a low margin storage device management chips in one of the biggest semiconductor business model pivots of the past decade, Marvell Technology (NASDAQ: MRVL) is a fabless designer of special purpose data processing and networking chips used by data centers, communications carriers, enterprises, and autos.

Marvell Technology reported revenues of $2.07 billion, up 36.8% year on year. This result was in line with analysts’ expectations. Overall, it was a satisfactory quarter as it also put up a beat of analysts’ EPS estimates.

Marvell Technology pulled off the fastest revenue growth among its peers. The stock is down 9.8% since reporting and currently trades at $83.95.

Read our full, actionable report on Marvell Technology here, it’s free for active Edge members.

FormFactor (NASDAQ: FORM)

With customers across the foundry and fabless markets, FormFactor (NASDAQ: FORM) is a US-based provider of test and measurement technologies for semiconductors.

FormFactor reported revenues of $202.7 million, down 2.5% year on year. This print beat analysts’ expectations by 1.3%. Overall, it was an exceptional quarter as it also logged a beat of analysts’ EPS estimates and a solid beat of analysts’ adjusted operating income estimates.

The stock is up 17.9% since reporting and currently trades at $56.26.

Read our full, actionable report on FormFactor here, it’s free for active Edge members.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.