Building materials company Builders FirstSource (NYSE: BLDR) reported Q1 CY2026 results beating Wall Street’s revenue expectations, but sales fell by 10.1% year on year to $3.29 billion. The company’s full-year revenue guidance of $15.1 billion at the midpoint came in 1.3% above analysts’ estimates. Its non-GAAP profit of $0.27 per share was 27.6% below analysts’ consensus estimates.

Is now the time to buy Builders FirstSource? Find out by accessing our full research report, it’s free.

Builders FirstSource (BLDR) Q1 CY2026 Highlights:

- Revenue: $3.29 billion vs analyst estimates of $3.17 billion (10.1% year-on-year decline, 3.6% beat)

- Adjusted EPS: $0.27 vs analyst expectations of $0.37 (27.6% miss)

- Adjusted EBITDA: $213.8 million vs analyst estimates of $204.1 million (6.5% margin, 4.7% beat)

- The company dropped its revenue guidance for the full year to $15.1 billion at the midpoint from $15.3 billion, a 1.3% decrease

- EBITDA guidance for the full year is $1.3 billion at the midpoint, below analyst estimates of $1.39 billion

- Operating Margin: 0.5%, down from 5% in the same quarter last year

- Free Cash Flow Margin: 1.2%, similar to the same quarter last year

- Market Capitalization: $8.96 billion

“Our first quarter results reflect the adaptability of our operating model as we delivered strong strategic share growth in a weak housing market. Across the organization, we remain focused on the factors within our control, including serving our customers, expanding our differentiated portfolio of value-added solutions, and leveraging technology to accelerate growth and drive operational excellence. This disciplined approach continues to strengthen our leading position as a trusted, full-service partner to homebuilders,” commented Peter Jackson, CEO of Builders FirstSource.

Company Overview

Headquartered in Irving, TX, Builders FirstSource (NYSE: BLDR) is a construction materials manufacturer that offers a variety of lumber and lumber-related building products.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Builders FirstSource’s sales grew at a mediocre 6.2% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Builders FirstSource’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 6.9% annually.

We can better understand the company’s revenue dynamics by analyzing its most important segments, Manufactured products

and Windows, doors & millwork

, which are 22.3% and 26% of revenue. Over the last two years, Builders FirstSource’s Manufactured products

revenue (floors, wall panels, and engineered wood) averaged 14.1% year-on-year declines while its Windows, doors & millwork

revenue (self explanatory) averaged 8.7% declines.

This quarter, Builders FirstSource’s revenue fell by 10.1% year on year to $3.29 billion but beat Wall Street’s estimates by 3.6%.

Looking ahead, sell-side analysts expect revenue to grow 1.9% over the next 12 months. While this projection implies its newer products and services will fuel better top-line performance, it is still below the sector average.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Builders FirstSource has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 11.6%.

Looking at the trend in its profitability, Builders FirstSource’s operating margin decreased by 9.9 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Builders FirstSource’s breakeven margin was 0.5%, down 4.5 percentage points year on year. Since Builders FirstSource’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

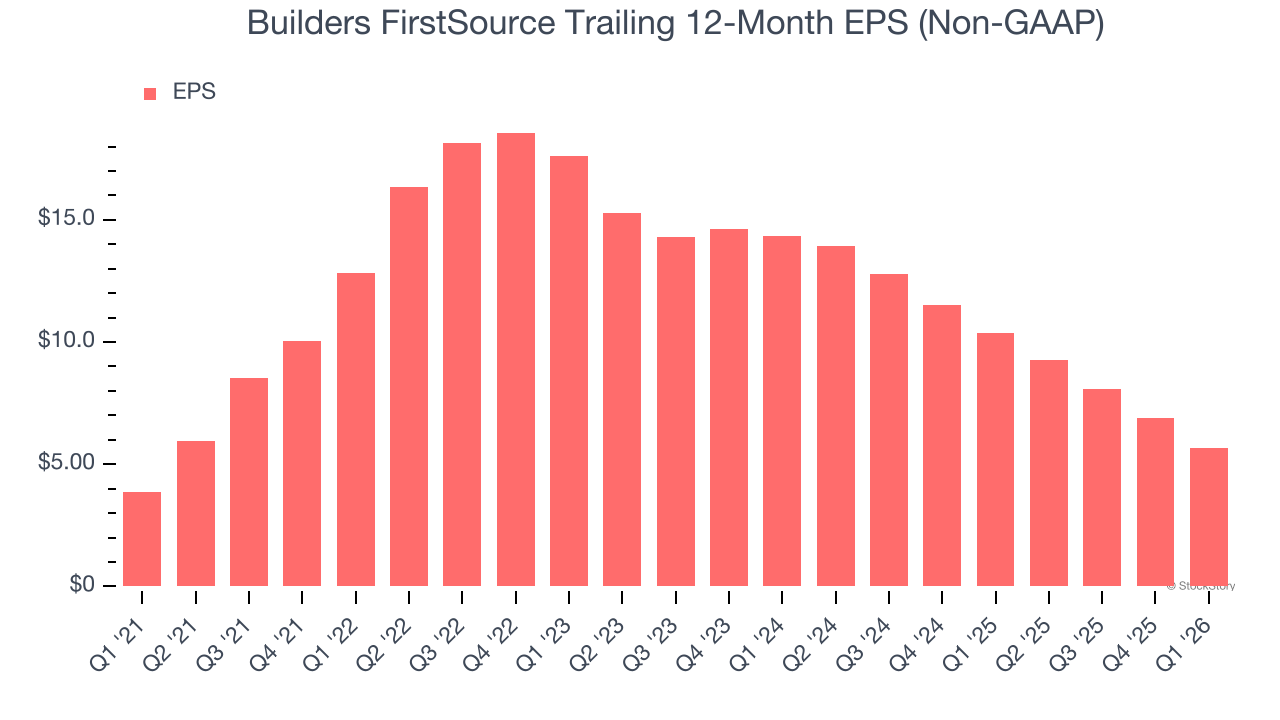

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Builders FirstSource’s unimpressive 8% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Builders FirstSource’s two-year annual EPS declines of 37.2% were bad and lower than its two-year revenue losses.

Diving into the nuances of Builders FirstSource’s earnings can give us a better understanding of its performance. Builders FirstSource’s operating margin has declined over the last two years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Builders FirstSource reported adjusted EPS of $0.27, down from $1.51 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Builders FirstSource’s full-year EPS of $5.65 to grow 8.1%.

Key Takeaways from Builders FirstSource’s Q1 Results

We were impressed by how significantly Builders FirstSource blew past analysts’ revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed and its adjusted operating income fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $83.17 immediately following the results.

Builders FirstSource’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).