Over the past six months, Hormel Foods’s shares (currently trading at $23.91) have posted a disappointing 19.5% loss, well below the S&P 500’s 22.7% gain. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Hormel Foods, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Why Do We Think Hormel Foods Will Underperform?

Even with the cheaper entry price, we're sitting this one out for now. Here are three reasons you should be careful with HRL and a stock we'd rather own.

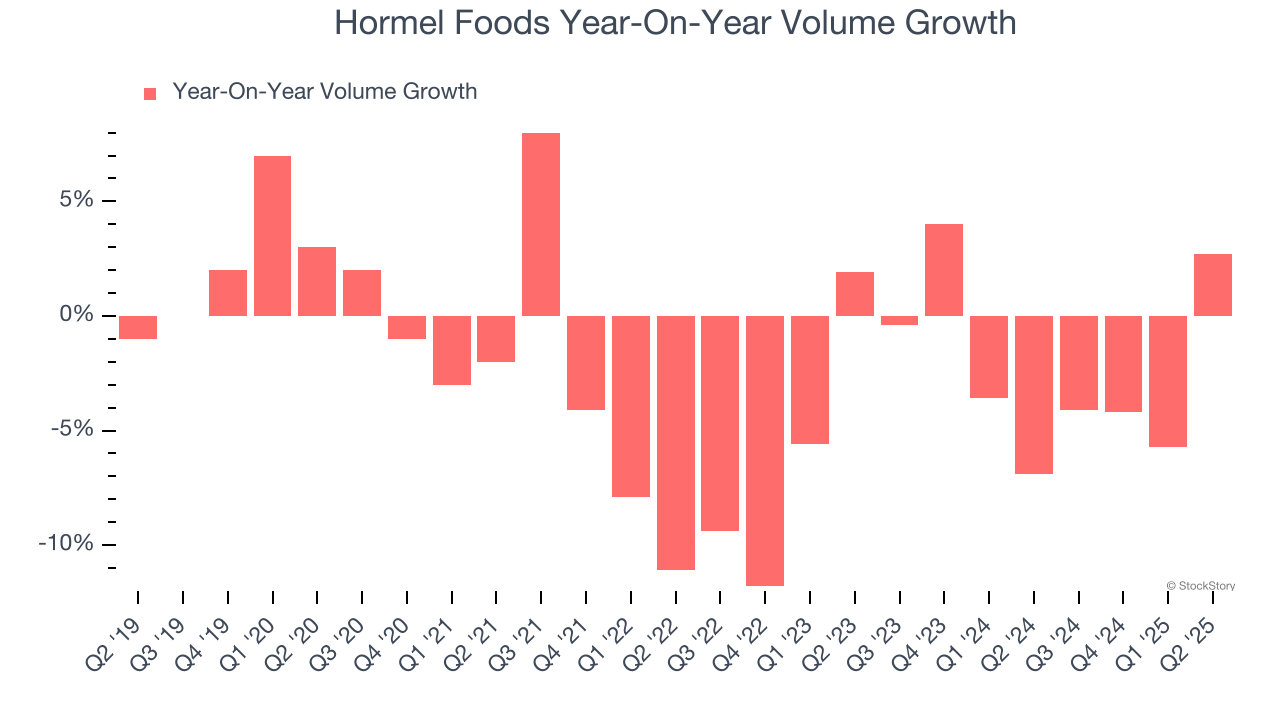

1. Demand Slipping as Sales Volumes Decline

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Hormel Foods’s average quarterly sales volumes have shrunk by 2.3% over the last two years. This decrease isn’t ideal because the quantity demanded for consumer staples products is typically stable.

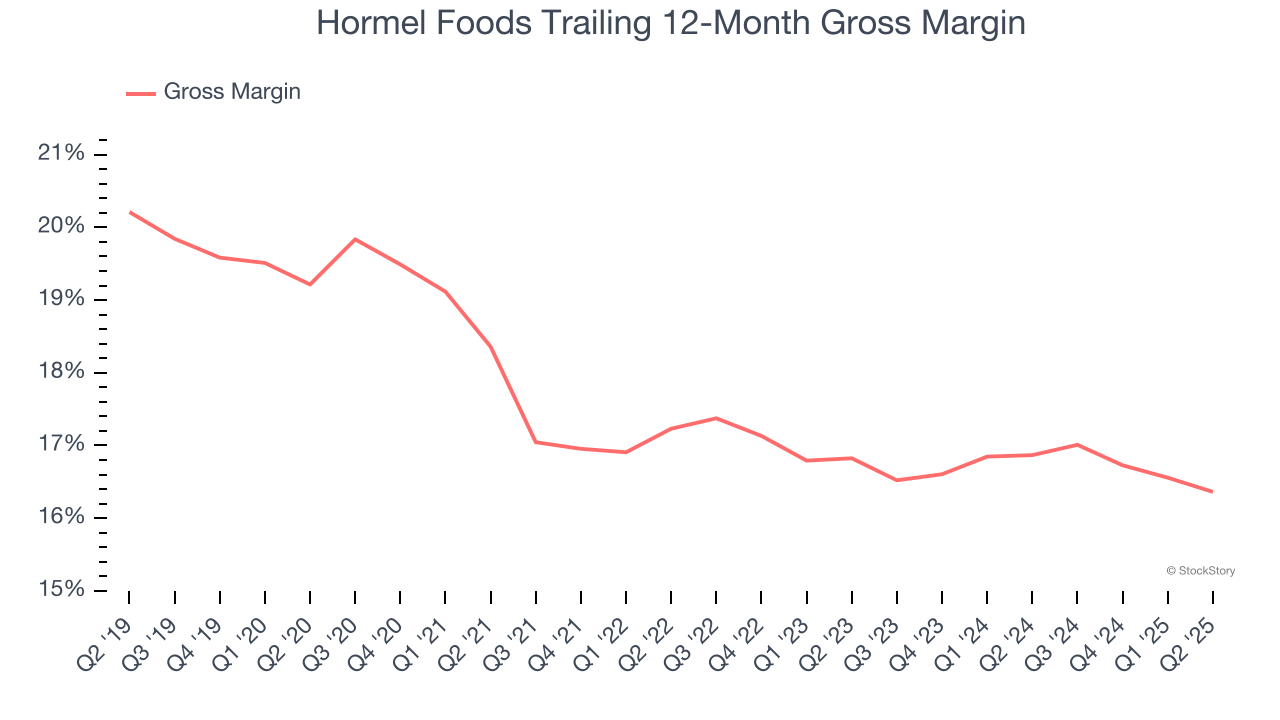

2. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

Hormel Foods has bad unit economics for a consumer staples company, signaling it operates in a competitive market and lacks pricing power because its products can be substituted. As you can see below, it averaged a 16.6% gross margin over the last two years. That means Hormel Foods paid its suppliers a lot of money ($83.39 for every $100 in revenue) to run its business.

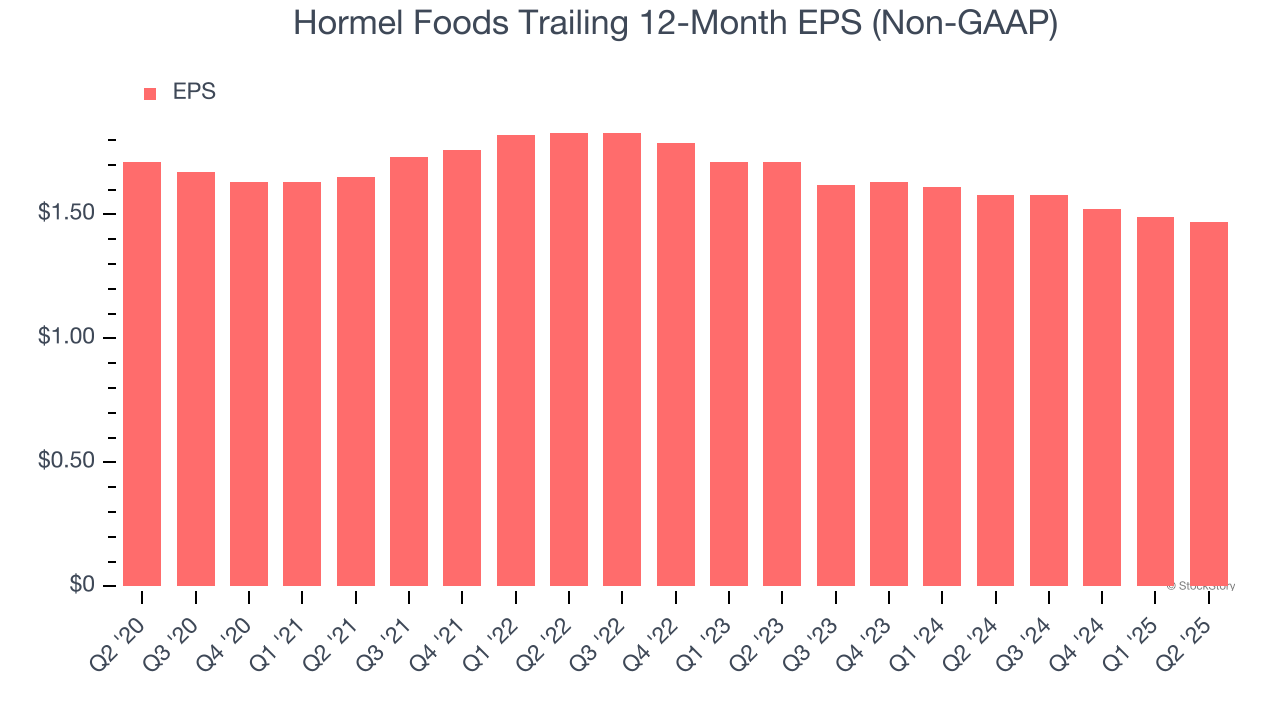

3. EPS Trending Down

We track the change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Hormel Foods, its EPS declined by 7% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Final Judgment

Hormel Foods falls short of our quality standards. After the recent drawdown, the stock trades at 16.1× forward P/E (or $23.91 per share). This valuation tells us a lot of optimism is priced in - we think other companies feature superior fundamentals at the moment. We’d recommend looking at the most entrenched endpoint security platform on the market.

Stocks We Like More Than Hormel Foods

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.