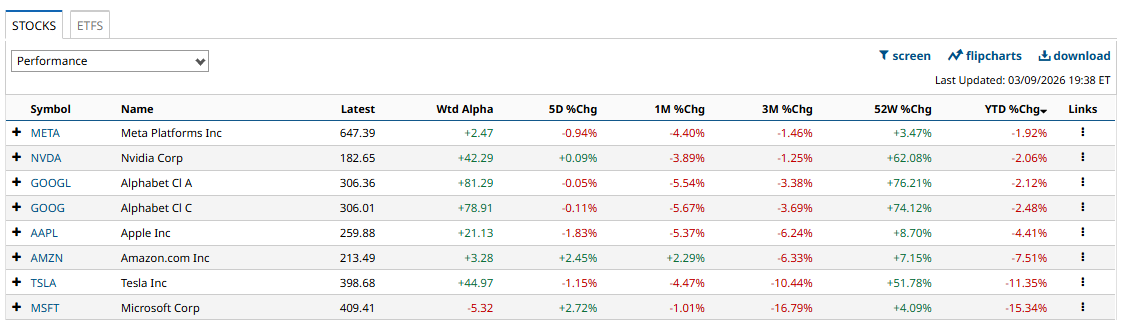

Shares of Microsoft (MSFT) have come under pressure in recent months, declining more than 15% year-to-date (YTD) and trailing its big tech peers in the “Magnificent Seven” group. The stock’s relative underperformance reflects growing investor concerns surrounding the company’s planned surge in capital expenditures and the long-term return on those investments.

As demand for artificial intelligence (AI) capabilities expands across its cloud ecosystem, Microsoft is investing significantly to build the computing capacity required to support growth. These investments are focused primarily on high-performance hardware and infrastructure, including GPUs and CPUs, as well as continued expansion of global data center capacity.

While MSFT is investing in AI capabilities, growth in Azure has moderated slightly from the previous quarter. This weighed on investor sentiment. Further, a significant portion of Microsoft’s backlog is related to OpenAI. This concentration has prompted questions about the durability and diversification of future cloud revenue.

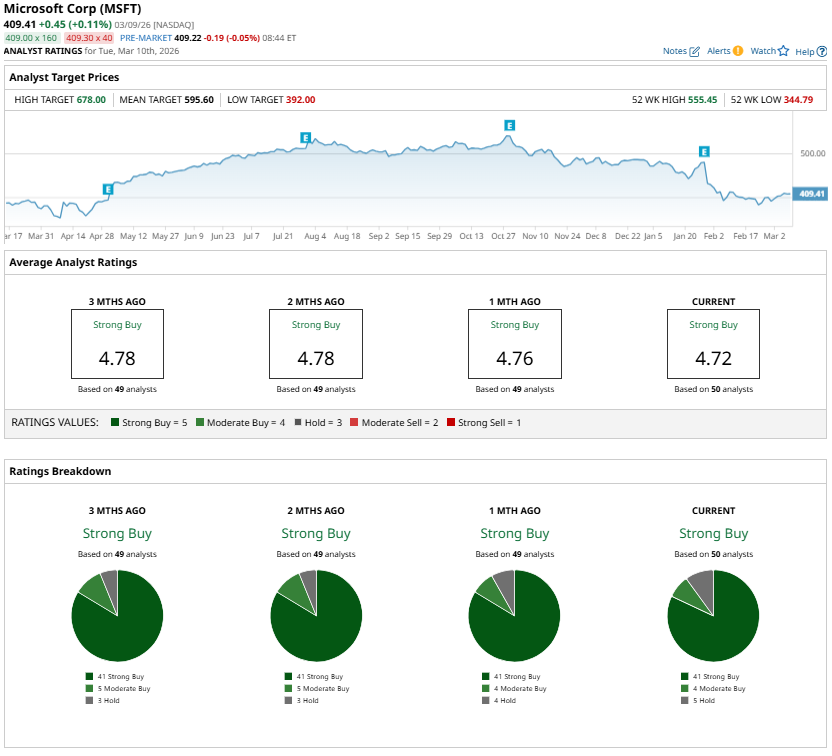

Despite these concerns and the stock’s recent underperformance, Wall Street sentiment remains positive. Analysts keep a “Strong Buy” consensus rating on MSFT stock, reflecting confidence in the company’s long-term growth prospects. The current average price target also implies meaningful upside potential over the next 12 months.

Key Drivers Supporting Microsoft Stock’s Investment Case

Microsoft continues to strengthen its long-term investment case despite facing near-term margin pressure. The company is currently investing heavily in AI infrastructure and capabilities, while its revenue mix is increasingly shifting toward Azure and other cloud services. These dynamics can weigh on margins in the short term, but strong revenue expansion has the potential to support continued earnings growth. At the same time, Microsoft’s aggressive investment strategy will help capture greater market share in rapidly expanding cloud and AI markets.

In the second quarter, Microsoft delivered revenue growth of 17% year-over-year (YoY), driven primarily by accelerating demand for its cloud and AI solutions. Earnings per share increased 24% during the same period. Revenue from Microsoft Cloud totaled $51.5 billion, up 26% from the previous year.

Performance in the Intelligent Cloud segment remained strong. Revenue in this division rose 29% YoY to $32.9 billion. Within intelligent cloud, Azure revenue increased 39%, slightly moderating from the 40% growth recorded in the previous quarter. Importantly, the moderation does not reflect weakening demand. Instead, Microsoft has indicated that demand for Azure services continues to exceed available supply, suggesting that current growth may be constrained more by capacity limitations than by any slowdown in customer interest.

Looking ahead, the company expects this business momentum to continue. Demand for Microsoft’s cloud and AI services remains strong across a wide range of workloads, industries, and geographic markets. Management has also noted that customer demand for these capabilities continues to outpace the company’s existing infrastructure capacity.

For the third quarter, Microsoft projects total revenue of $80.65 billion to $81.75 billion, implying YoY growth of approximately 15% to 17%. Revenue from the Intelligent Cloud segment is expected to reach between $34.1 billion and $34.4 billion, representing growth of roughly 27% to 29%. Azure revenue growth is projected to range from 37% to 38% in constant currency, which is high even as the company faces challenging YoY comparisons.

Coming to customer concentration risk related to Microsoft’s partnership with OpenAI. At the end of the second quarter, Microsoft’s commercial remaining performance obligation (RPO) stood at $625 billion, with roughly 45% tied to OpenAI-related agreements. However, the remainder of the backlog, which represents a substantial portion, expanded by 28% in the quarter. This growth highlights the broad, diversified demand for Microsoft’s portfolio of cloud, enterprise software, and AI-enabled services.

The Bottom Line on MSFT Stock

While MSFT stock has recently lagged its peers, the company’s underlying fundamentals remain strong, supporting a bullish outlook. Robust demand for cloud and AI services, sustained double-digit revenue growth, and expanding backlog across a diversified customer base strengthen the long-term growth narrative.

As Microsoft continues scaling its infrastructure to meet accelerating AI demand and strengthens its competitive positioning, it remains well-positioned to deliver solid long-term growth.

Analysts are bullish about MSFT, and the average price target of $595.60 suggests about 45% upside potential from current levels.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart