Amazon (AMZN) stock has lagged its Big Tech peers over the past year, rising approximately 6% over the last 12 months but down about 7% year-to-date (YTD), making it one of the weakest performers within the “Magnificent Seven” group. This underperformance reflects mounting competitive pressures in its most profitable segment and rising concerns about future margins.

The primary source of investor caution is Amazon Web Services (AWS), the company’s high-margin cloud computing division. AWS faces intensifying competition from Google Cloud, owned by Alphabet (GOOGL), and Microsoft (MSFT) Azure. Both rivals continue to expand aggressively, investing heavily in infrastructure and artificial intelligence (AI) capabilities to gain market share. As enterprise customers diversify cloud providers and demand advanced AI functionality, AWS is operating in an increasingly competitive environment.

Adding to these concerns, Amazon plans to substantially increase its capital expenditures in 2026. During the fourth-quarter conference call, Amazon announced $200 billion in capital spending, with the majority allocated to AWS.

What’s Behind Amazon’s Rising Capex?

Amazon has outlined a significant increase in capital expenditures, attributing the move primarily to exceptionally strong demand within AWS. The scale of the planned investment reflects the company’s strategic focus on expanding data-center capacity and enhancing its AI infrastructure. Management views this buildout as essential to meeting accelerating customer demand and sustaining long-term growth in cloud computing and AI-driven services.

AWS is experiencing robust demand, particularly in AI-related workloads. Management indicated that the newly installed capacity is being monetized rapidly. Amazon expects that incremental capacity will be fully utilized. The company believes this expansion will strengthen its competitive positioning in an attractive sector, while supporting strong returns on invested capital over time.

However, the stepped-up capital spending is likely to exert pressure on margins. In addition, Amazon’s trailing 12-month free cash flow has consistently declined on a quarter-over-quarter basis, falling from $47.74 billion in the third quarter of 2024 to $11.19 billion in Q4 2025. With capital expenditures set to rise further, free cash flow could turn negative in 2026.

In sum, Amazon’s rising capital expenditures reflect the company’s strategy to capitalize on strong demand for cloud and AI. While the investments may strengthen its long-term competitive position and revenue potential, they introduce short- to medium-term pressure on cash flow and profitability metrics.

What’s Next for Amazon Stock?

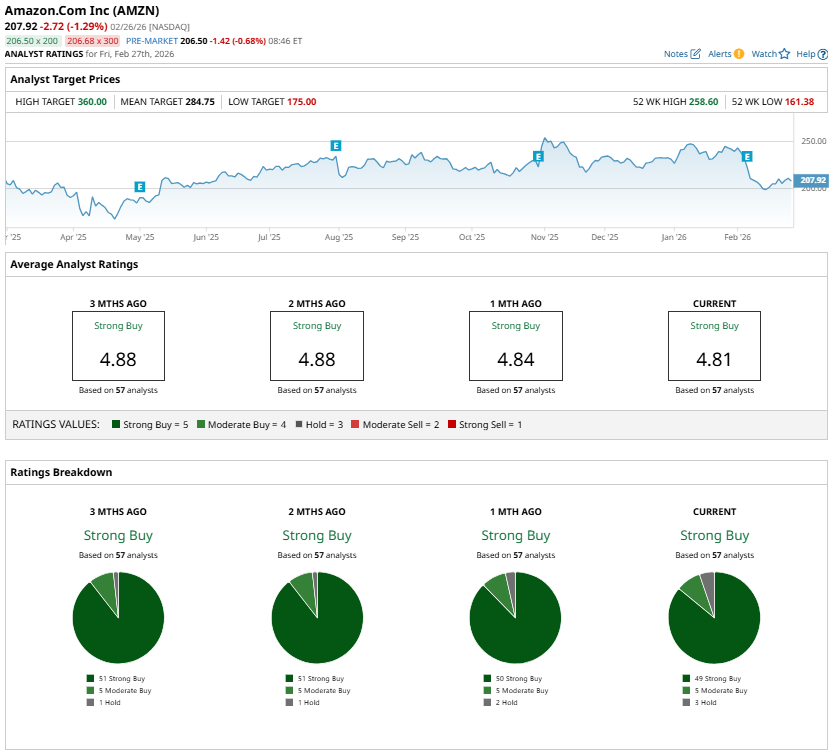

The increased competition and higher capex pose challenges for AMZN stock and add uncertainty. The Street’s lowest price target for AMZN stock is $175, implying about 19% potential downside from current levels.

However, despite these pressures, Amazon’s fundamental outlook remains constructive, supported by accelerating performance in its cloud and advertising segments, a fast-growing chips business, and improving operating metrics within its online retail business. The company’s cloud platform, AWS, delivered 24% year-over-year (YOY) revenue growth in the fourth quarter, marking its fastest expansion in thirteen quarters. Quarterly AWS revenue increased by $2.6 billion sequentially and almost $7 billion compared with the prior-year period, bringing AWS to a $142 billion annualized revenue run rate.

In addition to core cloud services, Amazon’s custom silicon portfolio, including its Graviton and Trainium processors, has scaled meaningfully. This chips business has surpassed a $10 billion annual revenue run rate and is expanding at triple-digit YOY rates. Continued investment in infrastructure capacity and incremental service offerings is expected to further support growth across the AWS ecosystem.

Notably, Amazon is also experiencing strong demand for non-AI workloads, driven by ongoing cloud migration initiatives.

Advertising represents another significant growth driver. Q4 advertising revenue increased 22% YOY to $21.3 billion, benefiting from Amazon’s full-funnel strategy that connects brands with consumers across its commerce and media properties.

With strong momentum in AWS and the advertising business, and emerging opportunities in AI, custom chips, low Earth orbit satellite initiatives, and robotics, Amazon’s long-term growth potential remains solid.

Wall Street sentiment remains favorable. AMZN stock carries a consensus “Strong Buy” rating, with an average price target of $284.75, suggesting approximately 32% potential upside from current levels. Meanwhile, the highest price target of $360 implies potential appreciation of roughly 67% over the next 12 months.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Down 23% in the YTD, Should You Buy the Dip in Snowflake Stock?

- Oil Price Shocks Have Hit India, But This 1 Emerging Market ETF Is Still a Buy Now Near $40

- Want to Invest in AI? Consider These 3 Bank Stocks.

- Investors Are Bullish on Alphabet Stock - Piling Into GOOGL Call Options With Huge Unusual Options Volume