Micron (MU) has been one of the strongest performers over the past year, reflecting the surge in artificial intelligence (AI) infrastructure spending and the company’s strategic position in the memory industry. Shares are up around 35% year-to-date (YTD) and have surged by more than 307% in 12 months.

Notably, AI workloads require enormous amounts of high-bandwidth, high-capacity memory. This has created a surge in demand for DRAM and advanced memory solutions, areas where Micron has a strong technological footprint, positioning it well to benefit from this investment cycle.

Further, Micron is also benefiting from a widening set of applications for its memory products. Industrial demand is strengthening as autonomous systems are increasingly adopted across sectors. Memory and storage components are increasingly embedded in factory automation systems, video surveillance platforms, aerospace and defense technologies, robotics, and edge networking equipment. These structural shifts are steadily expanding the total addressable market for memory chips, strengthening long-term demand for Micron’s product portfolio.

Supply dynamics within the global memory market are also playing in Micron’s favor. The global memory market has historically been cyclical, often swinging between periods of oversupply and sharp price downturns. In the current cycle, however, supply growth has remained constrained while demand has accelerated sharply. The resulting tighter supply conditions have supported stronger pricing across the memory industry, which, in turn, has helped improve Micron's profitability.

What’s Next for Micron Stock?

Demand for AI infrastructure will remain the major growth driver for Micron in the coming quarters. Hyperscalers are significantly increasing capital expenditure on data centers, which should boost demand for memory and storage products. At the same time, broader adoption of Micron’s products across multiple industries and a constrained supply environment are likely to support stronger pricing and improved profitability.

Micron’s data center business is likely to be a major growth catalyst. Revenue from its data center NAND portfolio exceeded $1 billion in the fiscal first quarter, reflecting strong demand for the company’s solid-state drive (SSD) offerings. This growth has been supported by Micron’s advanced NAND technology. Across the memory industry, demand currently exceeds supply for both DRAM and NAND products. Management expects higher pricing, lower production costs, and a favorable product mix to expand gross margins and drive continued earnings growth in 2026.

The company expects to deliver record financial results during fiscal 2026. Management projects new highs in revenue, gross margin, earnings per share (EPS), and free cash flow in both the second quarter and the full fiscal year. In addition, Micron has finalized agreements covering price and volume for its entire calendar-year 2026 supply of high-bandwidth memory (HBM), including its next-generation HBM4 products. The company anticipates that the addressable market for HBM will expand rapidly in the coming years, providing a long-term growth opportunity.

For the second fiscal quarter, Micron expects revenue of approximately $18.7 billion, representing an increase of more than 132% from $8.05 billion in the prior year. This would mark acceleration in growth compared with the 57% year-over-year (YoY) revenue increase reported in the first quarter. Gross margin is projected to reach roughly 68%, a significant improvement from the adjusted gross margin of 37.9% reported a year earlier. EPS is expected to rise to about $8.42, compared with adjusted EPS of $1.56 in the previous year.

For fiscal 2026, analysts forecast substantial earnings growth for Micron. Consensus estimates suggest EPS could increase by about 349% in fiscal 2026, followed by an additional 42% growth in fiscal 2027. The solid revenue and profit growth could translate into meaningful capital appreciation for investors.

While Micron’s growth outlook remains solid, its valuation is still compelling. MU stock currently trades at 12.5 times forward earnings, which looks attractive relative to Micron’s EPS growth trajectory through 2026 and beyond.

Analysts Still Bullish on MU Stock

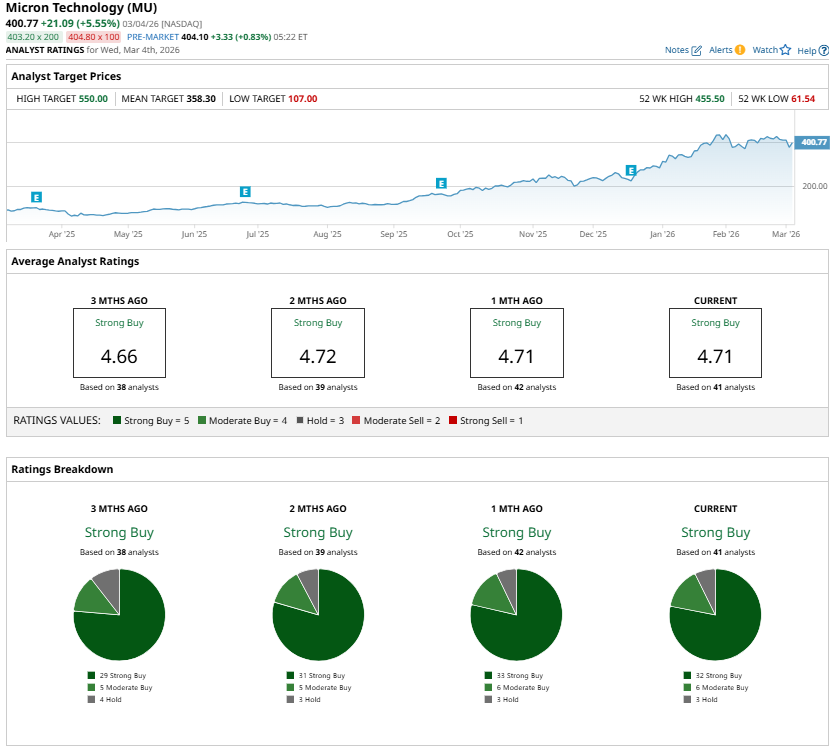

Supporting Micron’s investment case is the analysts’ bullish outlook. The majority of analysts maintain a “Strong Buy” rating on MU stock, and the Street’s highest price target of $550 implies over 37% upside from its recent close of $400.77.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart