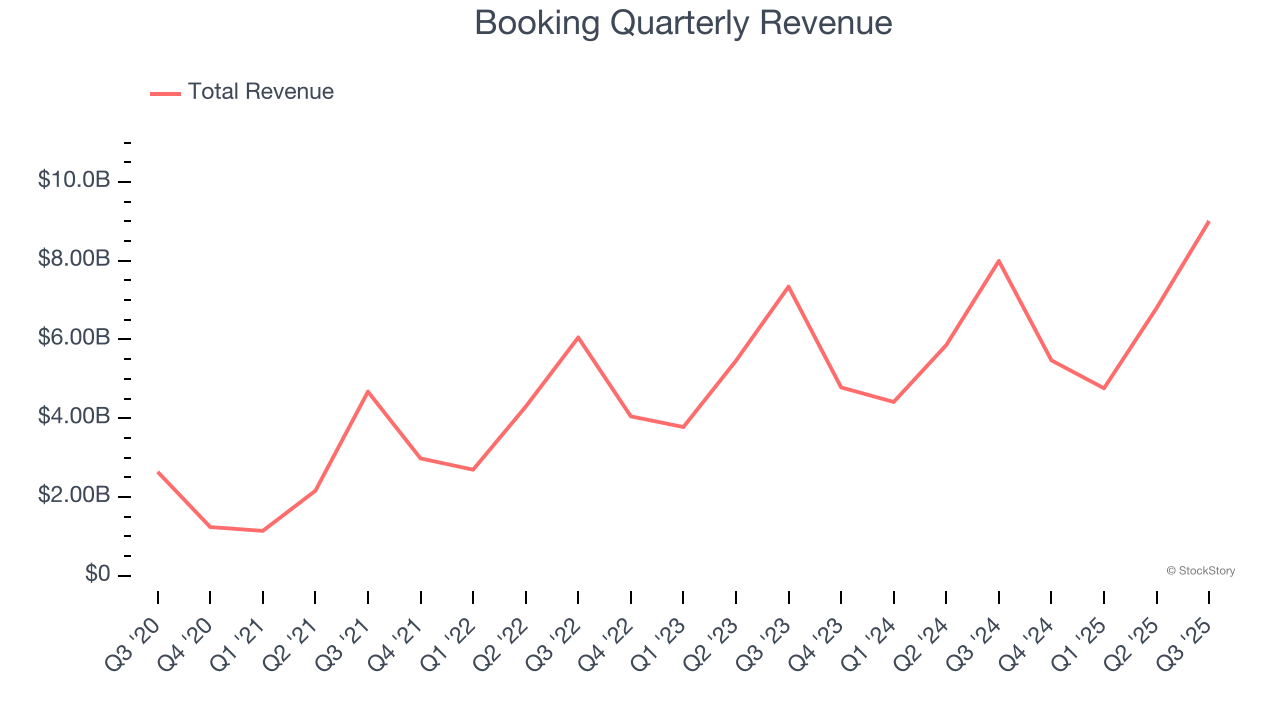

Online travel agency Booking Holdings (NASDAQ: BKNG) reported Q3 CY2025 results topping the market’s revenue expectations, with sales up 12.7% year on year to $9.01 billion. Its GAAP profit of $84.41 per share was 10% below analysts’ consensus estimates.

Is now the time to buy Booking? Find out by accessing our full research report, it’s free for active Edge members.

Booking (BKNG) Q3 CY2025 Highlights:

- Revenue: $9.01 billion vs analyst estimates of $8.74 billion (12.7% year-on-year growth, 3.1% beat)

- EPS (GAAP): $84.41 vs analyst expectations of $93.77 (10% miss)

- Adjusted EBITDA: $4.22 billion vs analyst estimates of $4.01 billion (46.8% margin, 5% beat)

- Operating Margin: 38.7%, down from 39.8% in the same quarter last year

- Free Cash Flow Margin: 15.2%, down from 46.1% in the previous quarter

- Room Nights Booked: 323 million, up 24 million year on year

- Market Capitalization: $170.3 billion

Company Overview

Formerly known as The Priceline Group, Booking Holdings (NASDAQ: BKNG) is the world’s largest online travel agency.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Booking’s 17.6% annualized revenue growth over the last three years was solid. Its growth beat the average consumer internet company and shows its offerings resonate with customers, a helpful starting point for our analysis.

This quarter, Booking reported year-on-year revenue growth of 12.7%, and its $9.01 billion of revenue exceeded Wall Street’s estimates by 3.1%.

Looking ahead, sell-side analysts expect revenue to grow 8.3% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Room Nights Booked

Booking Growth

As an online travel company, Booking generates revenue growth by increasing both the number of stays (or experiences) booked and the commission charged on those bookings.

Over the last two years, Booking’s room nights booked, a key performance metric for the company, increased by 8.7% annually to 323 million in the latest quarter. This growth rate is decent for a consumer internet business and indicates people enjoy using its offerings.

In Q3, Booking added 24 million room nights booked, leading to 8% year-on-year growth. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating booking growth just yet.

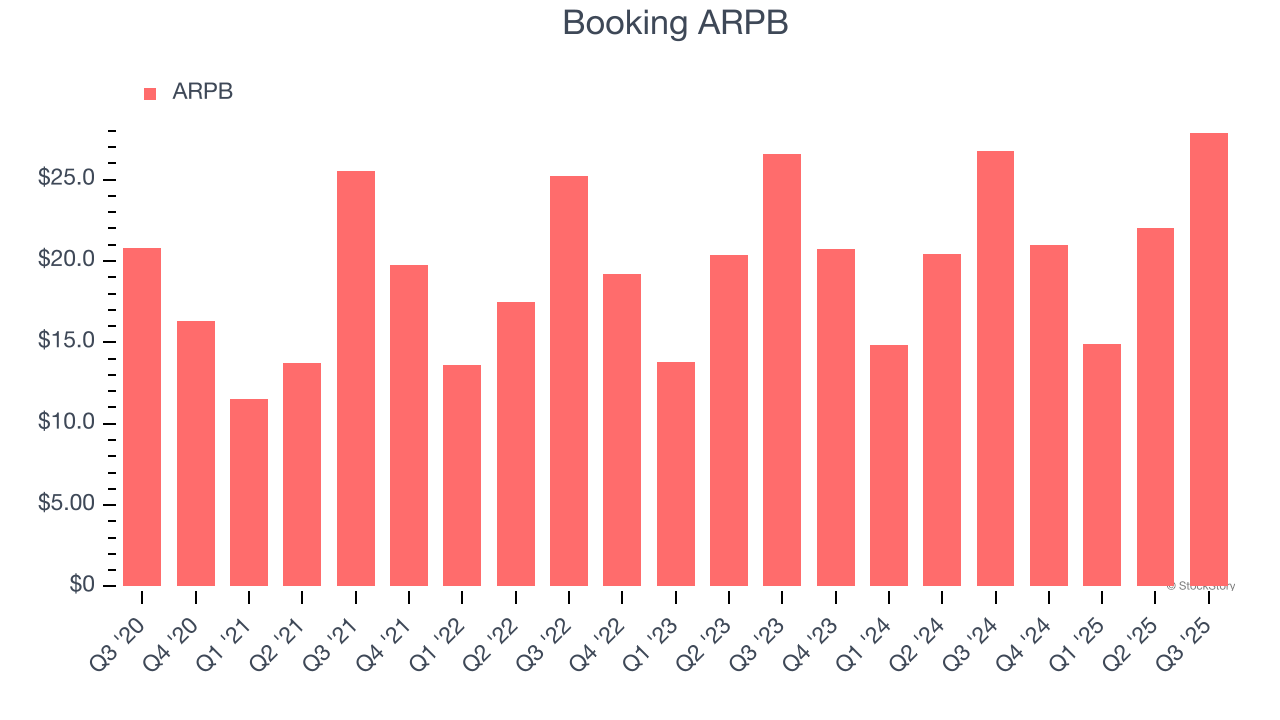

Revenue Per Booking

Average revenue per booking (ARPB) is a critical metric to track because it not only measures how much users book on its platform but also the commission that Booking can charge.

Booking’s ARPB growth has been mediocre over the last two years, averaging 3.8%. This isn’t great, but the increase in room nights booked is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Booking tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether bookings can continue growing at the current pace.

This quarter, Booking’s ARPB clocked in at $27.89. It grew by 4.3% year on year, slower than its booking growth.

Key Takeaways from Booking’s Q3 Results

We enjoyed seeing Booking beat analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 3.1% to $5,302 immediately after reporting.

Indeed, Booking had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.