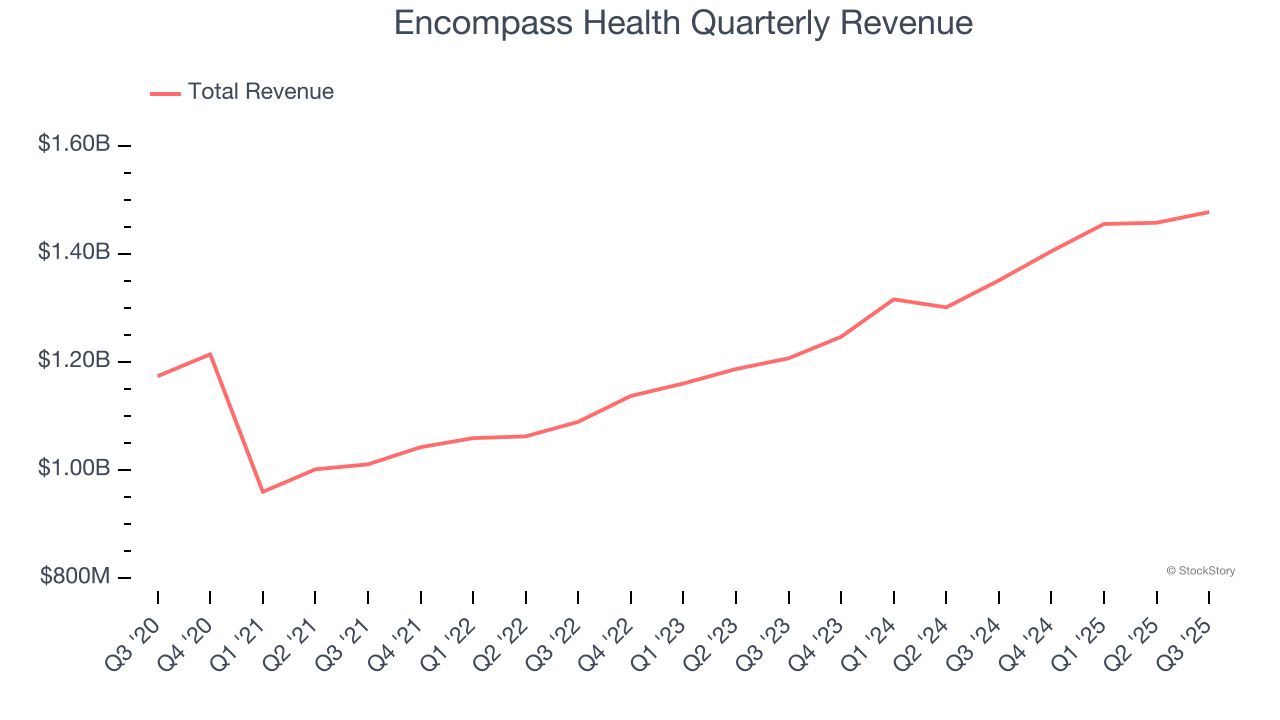

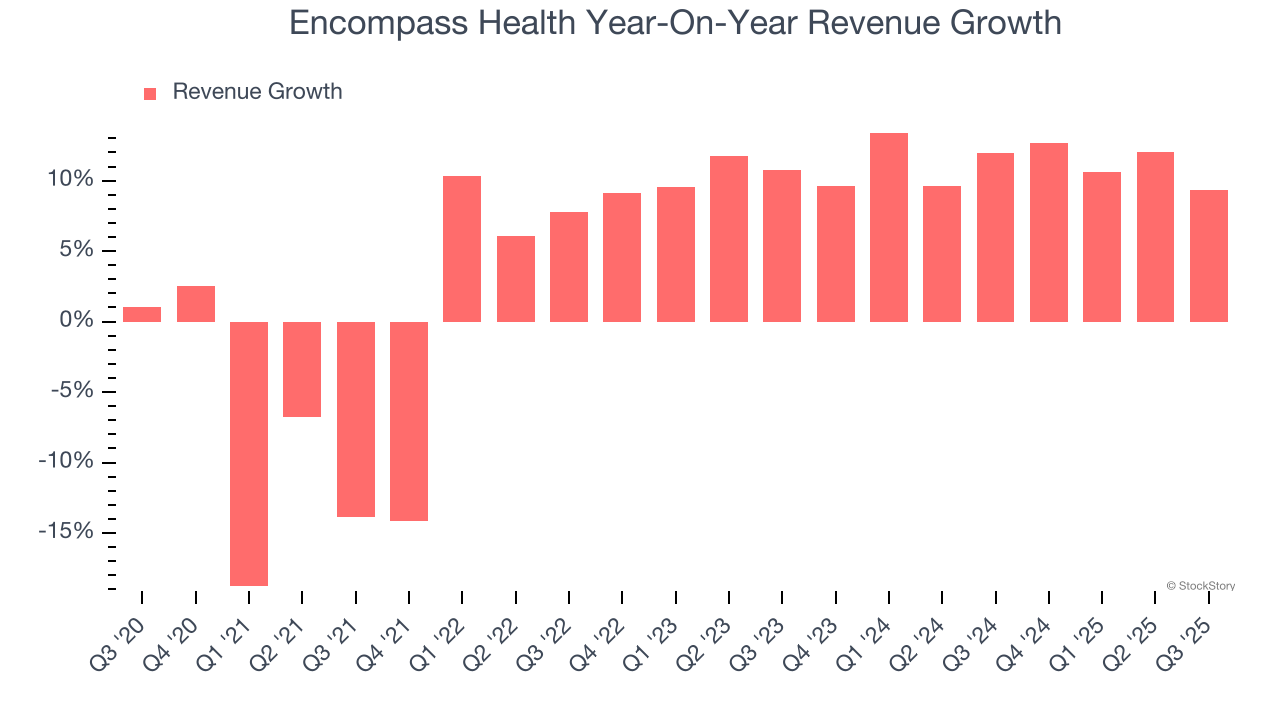

Health care services provider Encompass Health (NYSE: EHC) met Wall Street’s revenue expectations in Q3 CY2025, with sales up 9.4% year on year to $1.48 billion. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $5.93 billion at the midpoint. Its non-GAAP profit of $1.23 per share was 3.2% above analysts’ consensus estimates.

Is now the time to buy Encompass Health? Find out by accessing our full research report, it’s free for active Edge members.

Encompass Health (EHC) Q3 CY2025 Highlights:

- Revenue: $1.48 billion vs analyst estimates of $1.48 billion (9.4% year-on-year growth, in line)

- Adjusted EPS: $1.23 vs analyst estimates of $1.19 (3.2% beat)

- Adjusted EBITDA: $300.1 million vs analyst estimates of $296.2 million (20.3% margin, 1.3% beat)

- The company reconfirmed its revenue guidance for the full year of $5.93 billion at the midpoint

- Management raised its full-year Adjusted EPS guidance to $5.30 at the midpoint, a 1.2% increase

- EBITDA guidance for the full year is $1.25 billion at the midpoint, in line with analyst expectations

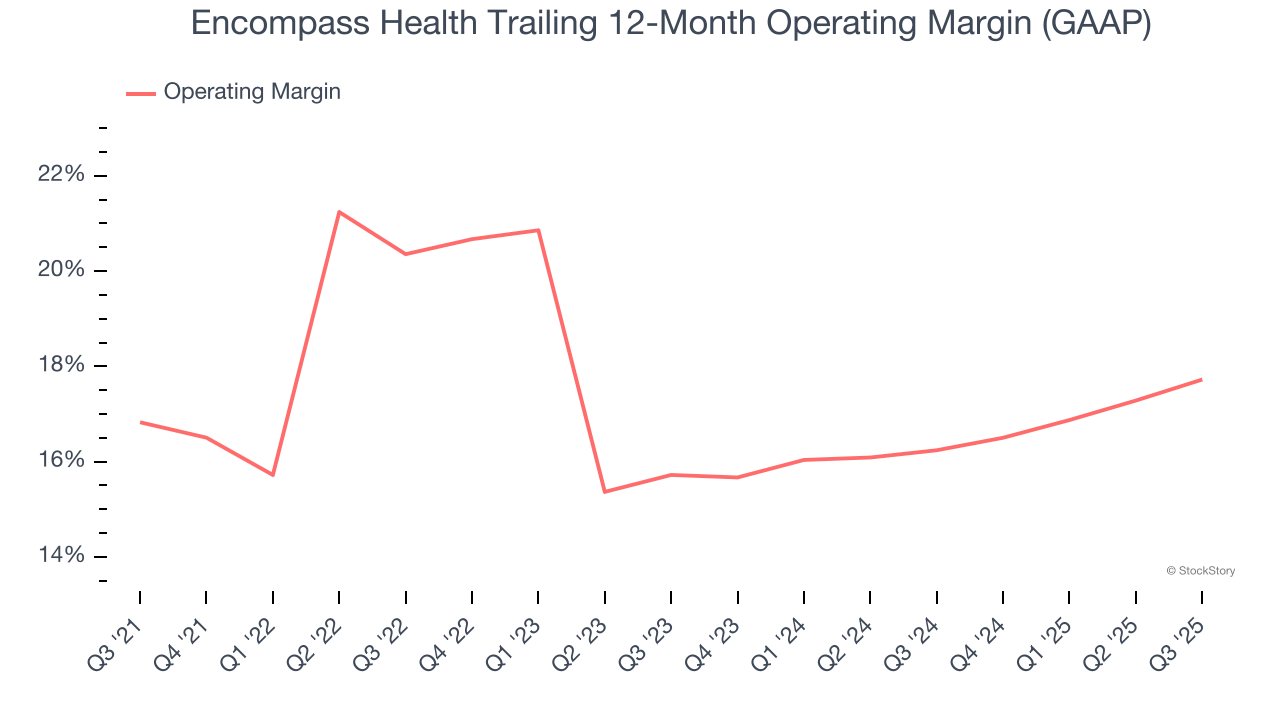

- Operating Margin: 17.5%, up from 15.7% in the same quarter last year

- Free Cash Flow Margin: 11.8%, down from 14% in the same quarter last year

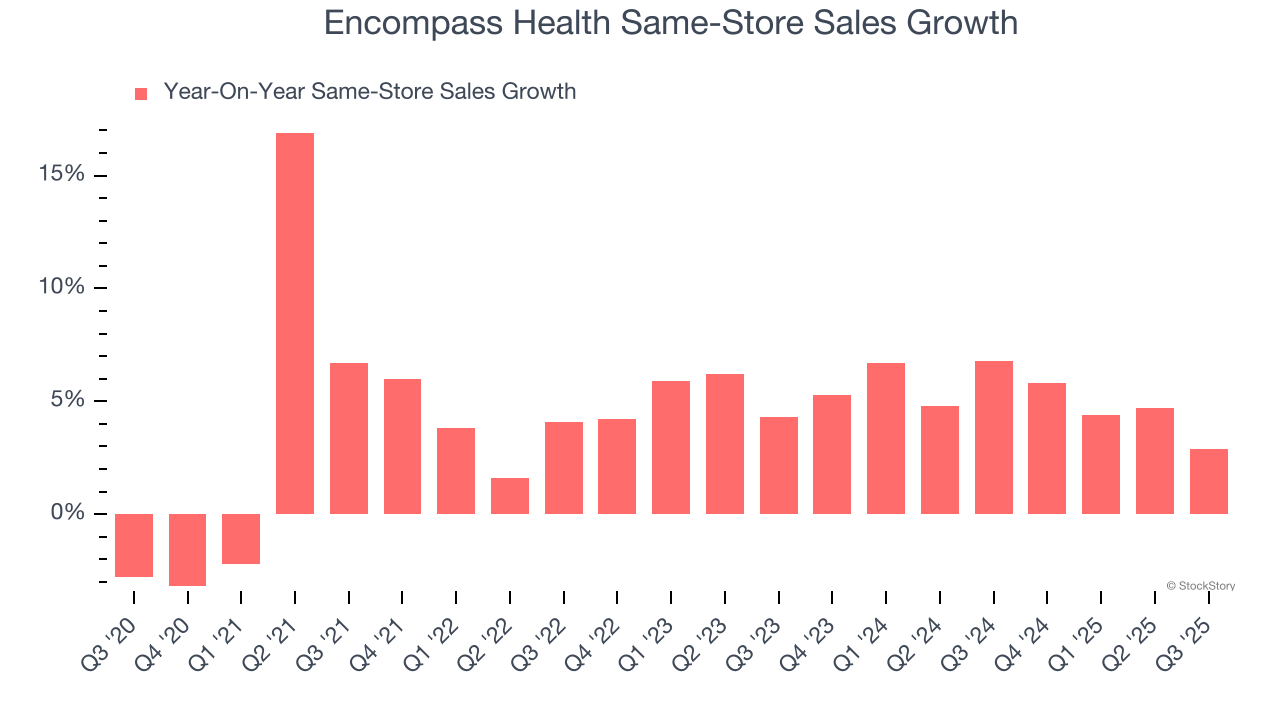

- Same-Store Sales rose 2.9% year on year (6.8% in the same quarter last year)

- Market Capitalization: $12.65 billion

"During the quarter, we further increased our capacity to serve patients in need of inpatient rehabilitation care by opening three new hospitals and adding 39 beds to existing hospitals," said President and Chief Executive Officer Mark Tarr.

Company Overview

With a network of 161 specialized facilities across 37 states and Puerto Rico, Encompass Health (NYSE: EHC) operates inpatient rehabilitation hospitals that help patients recover from strokes, hip fractures, and other debilitating conditions.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Encompass Health’s 4.7% annualized revenue growth over the last five years was mediocre. This was below our standard for the healthcare sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Encompass Health’s annualized revenue growth of 11.1% over the last two years is above its five-year trend, suggesting some bright spots.

We can better understand the company’s revenue dynamics by analyzing its same-store sales, which show how much revenue its established locations generate. Over the last two years, Encompass Health’s same-store sales averaged 5.2% year-on-year growth. Because this number is lower than its revenue growth, we can see the opening of new locations is boosting the company’s top-line performance.

This quarter, Encompass Health grew its revenue by 9.4% year on year, and its $1.48 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 9.1% over the next 12 months, a slight deceleration versus the last two years. Despite the slowdown, this projection is noteworthy and implies the market is baking in success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Encompass Health’s operating margin has been trending up over the last 12 months and averaged 17.3% over the last five years. Its solid profitability for a healthcare business shows it’s an efficient company that manages its expenses effectively.

Looking at the trend in its profitability, Encompass Health’s operating margin of 17.7% for the trailing 12 months may be around the same as five years ago, but it has increased by 2 percentage points over the last two years.

This quarter, Encompass Health generated an operating margin profit margin of 17.5%, up 1.9 percentage points year on year. This increase was a welcome development and shows it was more efficient.

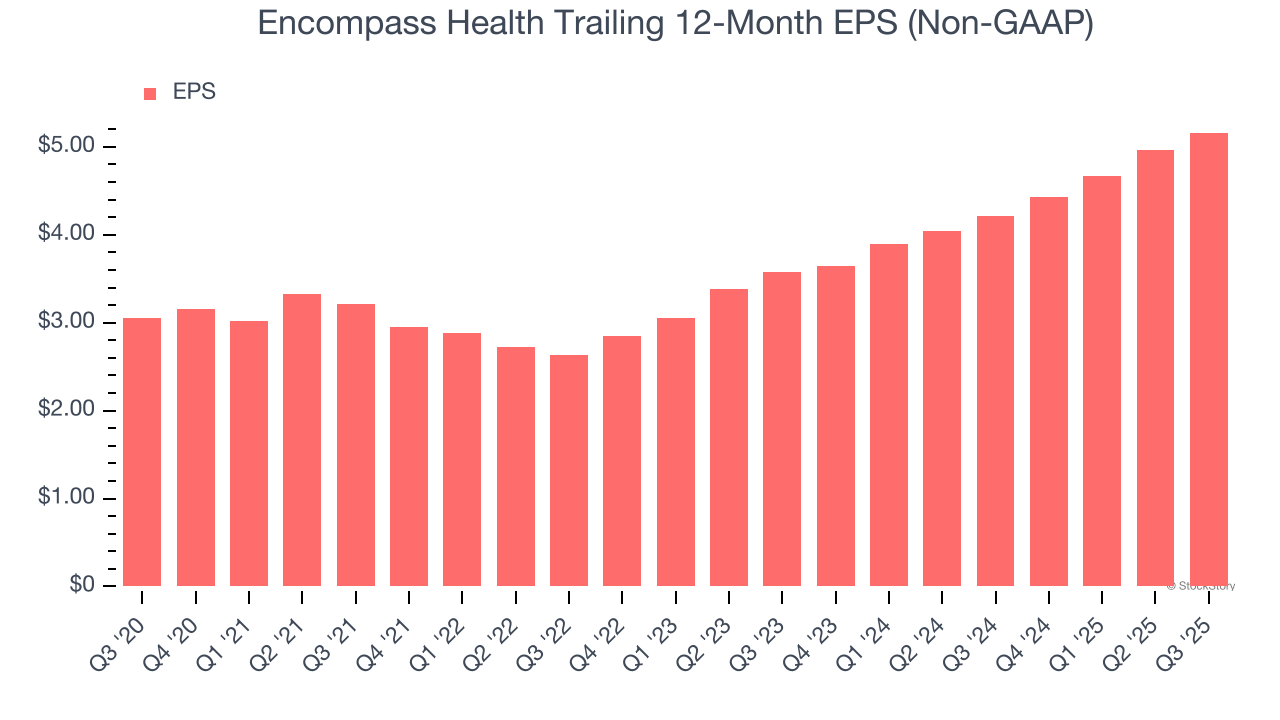

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Encompass Health’s EPS grew at a remarkable 11.1% compounded annual growth rate over the last five years, higher than its 4.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q3, Encompass Health reported adjusted EPS of $1.23, up from $1.03 in the same quarter last year. This print beat analysts’ estimates by 3.2%. Over the next 12 months, Wall Street expects Encompass Health’s full-year EPS of $5.16 to grow 8.8%.

Key Takeaways from Encompass Health’s Q3 Results

It was good to see Encompass Health narrowly top analysts’ full-year EPS guidance expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its same-store sales slightly missed and its revenue was in line with Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 6.6% to $117.40 immediately after reporting.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.