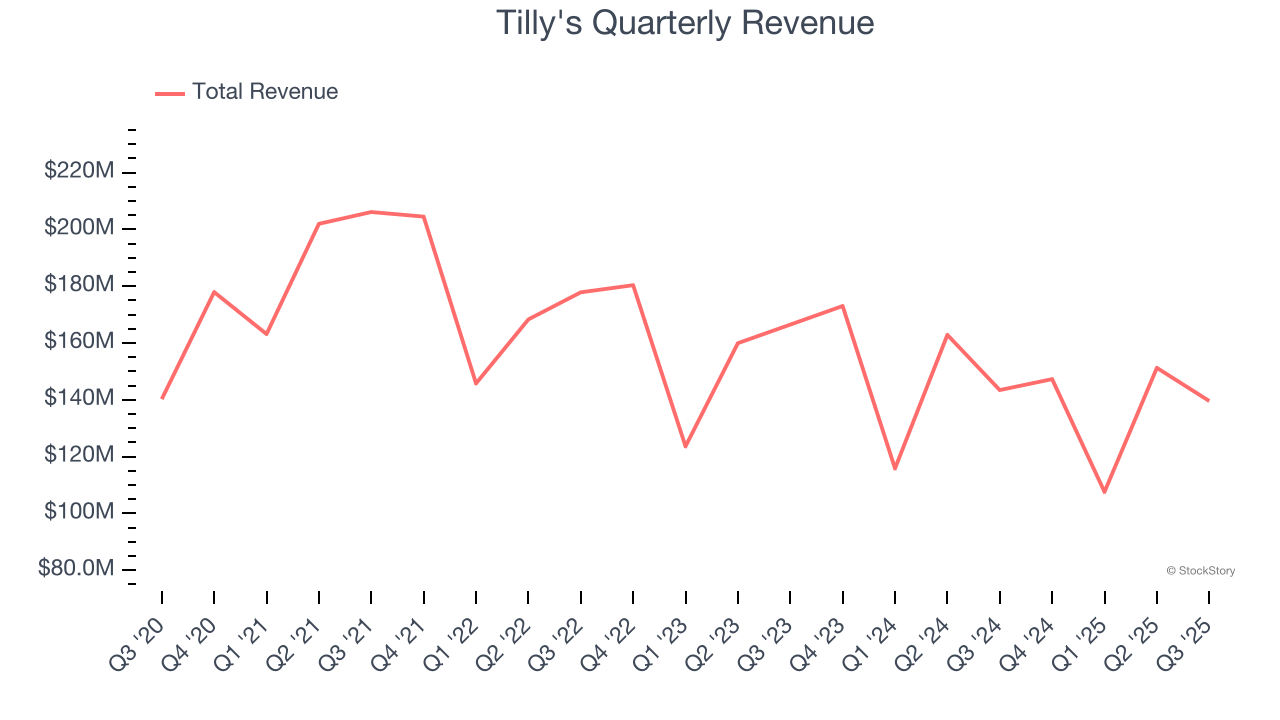

Young adult apparel retailer Tilly’s (NYSE: TLYS) beat Wall Street’s revenue expectations in Q3 CY2025, but sales fell by 2.7% year on year to $139.6 million. Guidance for next quarter’s revenue was better than expected at $148.5 million at the midpoint, 1.6% above analysts’ estimates. Its GAAP loss of $0.05 per share was 83.3% above analysts’ consensus estimates.

Is now the time to buy Tilly's? Find out by accessing our full research report, it’s free for active Edge members.

Tilly's (TLYS) Q3 CY2025 Highlights:

- Revenue: $139.6 million vs analyst estimates of $136.9 million (2.7% year-on-year decline, 2% beat)

- EPS (GAAP): -$0.05 vs analyst estimates of -$0.30 (83.3% beat)

- Adjusted EBITDA: $619,000 (0.4% margin, 111% year-on-year growth)

- Revenue Guidance for Q4 CY2025 is $148.5 million at the midpoint, above analyst estimates of $146.1 million

- EPS (GAAP) guidance for Q4 CY2025 is -$0.16 at the midpoint, beating analyst estimates by 51.6%

- Operating Margin: -1.4%, up from -4.4% in the same quarter last year

- Free Cash Flow was -$11.66 million compared to -$25.05 million in the same quarter last year

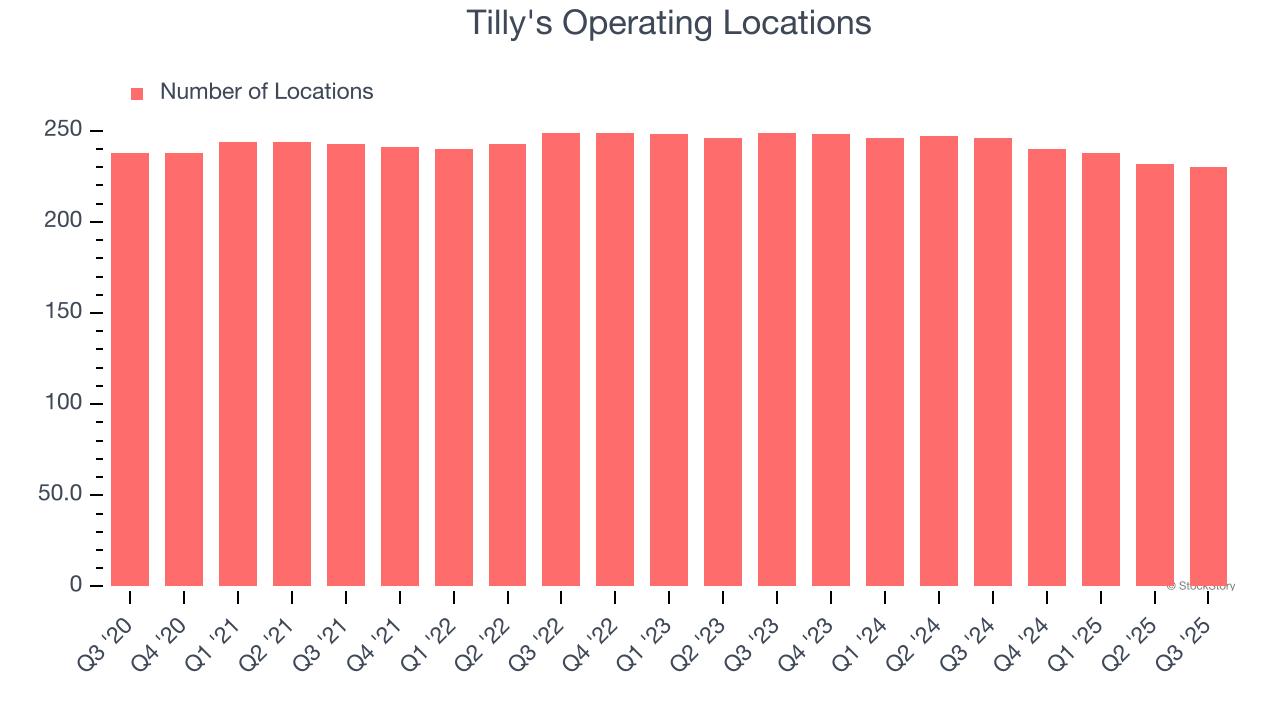

- Locations: 230 at quarter end, down from 246 in the same quarter last year

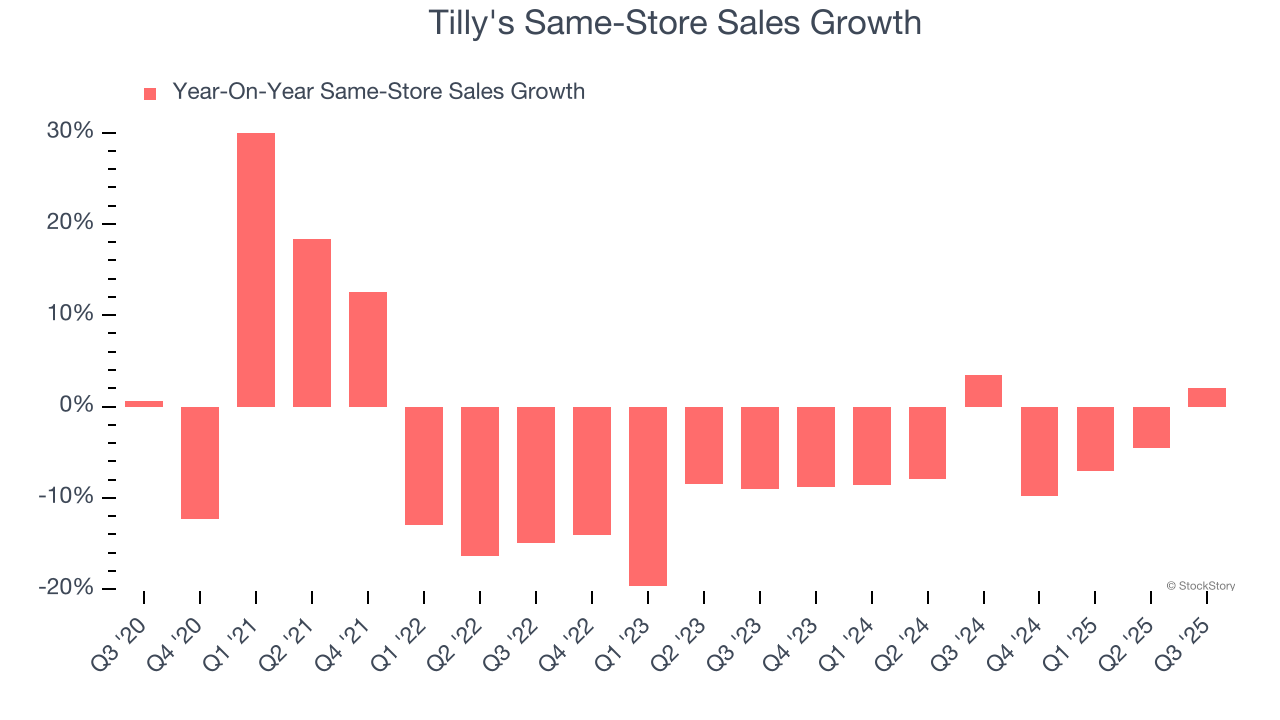

- Same-Store Sales rose 2% year on year (3.4% in the same quarter last year)

- Market Capitalization: $44.8 million

Company Overview

With an emphasis on skate and surf culture, Tilly’s (NYSE: TLYS) is a specialty retailer that sells clothing, footwear, and accessories geared towards fashion-forward teens and young adults.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $545.7 million in revenue over the past 12 months, Tilly's is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Tilly’s demand was weak over the last three years (we compare to 2019 to normalize for COVID-19 impacts). Its sales fell by 7.8% annually as it closed stores and observed lower sales at existing, established locations.

This quarter, Tilly’s revenue fell by 2.7% year on year to $139.6 million but beat Wall Street’s estimates by 2%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection suggests its newer products will catalyze better top-line performance, it is still below the sector average.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Store Performance

Number of Stores

Tilly's listed 230 locations in the latest quarter and has generally closed its stores over the last two years, averaging 2.6% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Tilly’s demand has been shrinking over the last two years as its same-store sales have averaged 5.2% annual declines. This performance isn’t ideal, and Tilly's is attempting to boost same-store sales by closing stores (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Tilly’s same-store sales rose 2% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

Key Takeaways from Tilly’s Q3 Results

We were impressed by Tilly’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 13.9% to $2.08 immediately following the results.

Indeed, Tilly's had a rock-solid quarterly earnings result, but is this stock a good investment here? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.