The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how home furniture retailer stocks fared in Q3, starting with Williams-Sonoma (NYSE: WSM).

Furniture retailers understand that ‘home is where the heart is’ but that no home is complete without that comfy sofa to kick back on or a dreamy bed to rest in. These stores focus on providing not only what is practically needed in a house but also aesthetics, style, and charm in the form of tables, lamps, and mirrors. Decades ago, it was thought that furniture would resist e-commerce because of the logistical challenges of shipping large furniture, but now you can buy a mattress online and get it in a box a few days later; so just like other retailers, furniture stores need to adapt to new realities and consumer behaviors.

The 4 home furniture retailer stocks we track reported a slower Q3. As a group, revenues missed analysts’ consensus estimates by 1.6% while next quarter’s revenue guidance was 8.9% below.

Luckily, home furniture retailer stocks have performed well with share prices up 16.8% on average since the latest earnings results.

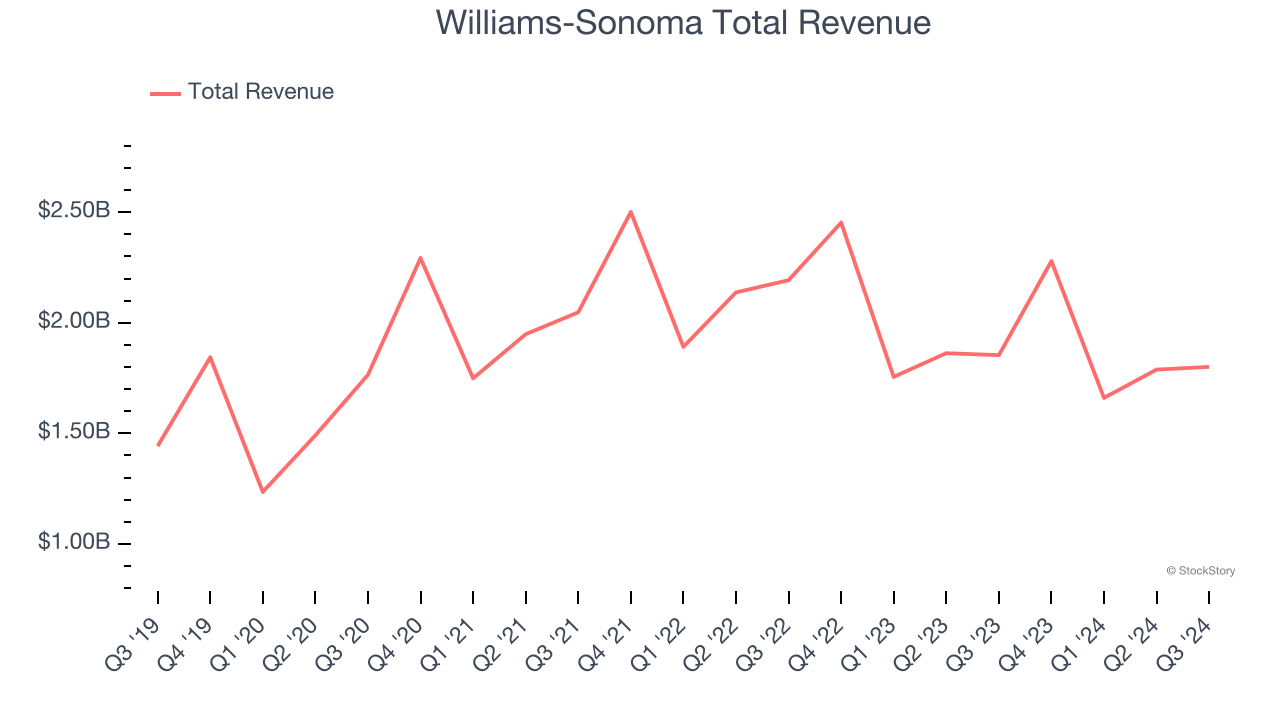

Best Q3: Williams-Sonoma (NYSE: WSM)

Started in 1956 as a store specializing in French cookware, Williams-Sonoma (NYSE: WSM) is a specialty retailer of higher-end kitchenware, home goods, and furniture.

Williams-Sonoma reported revenues of $1.80 billion, down 2.9% year on year. This print exceeded analysts’ expectations by 1.1%. Overall, it was a strong quarter for the company with a decent beat of analysts’ gross margin and EPS estimates.

“We are pleased with the results of our third quarter, beating both top and bottom-line expectations. The quarter was driven by continued improvement in our sales trend, market-share gains, and strong profit. In Q3, our comp came in at -2.9%, with an operating margin of 17.8%, delivering a 7.1% increase in earnings per share to $1.96. Our operating results reflect the operational improvements that we have been focused on all year, and demonstrate the strength of our margin profile in a difficult environment,” said Laura Alber, President and Chief Executive Officer.

Williams-Sonoma pulled off the biggest analyst estimates beat of the whole group. The stock is up 42.6% since reporting and currently trades at $195.72.

Is now the time to buy Williams-Sonoma? Access our full analysis of the earnings results here, it’s free.

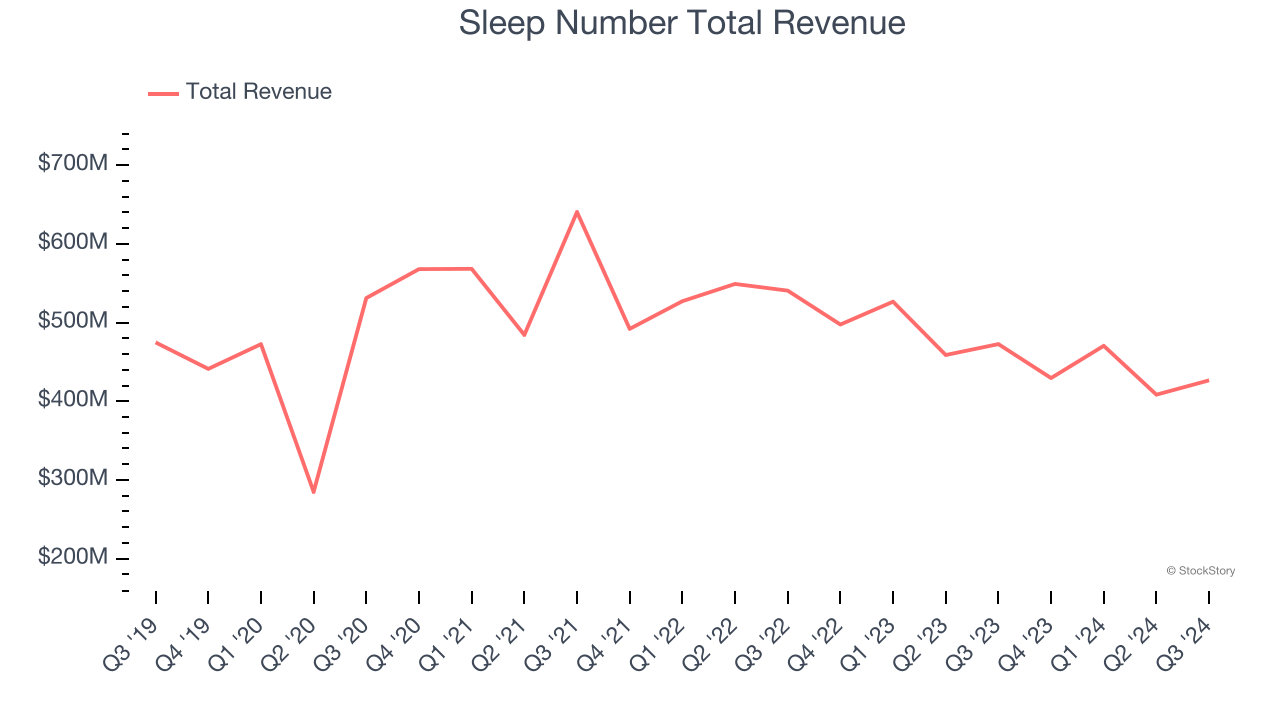

Sleep Number (NASDAQ: SNBR)

Known for mattresses that can be adjusted with regards to firmness, Sleep Number (NASDAQ: SNBR) manufactures and sells its own brand of bedding products such as mattresses, bed frames, and pillows.

Sleep Number reported revenues of $426.6 million, down 9.7% year on year, falling short of analysts’ expectations by 4.3%. The business performed better than its peers, but it was unfortunately a slower quarter with full-year EBITDA guidance missing analysts’ expectations.

The market seems happy with the results as the stock is up 13% since reporting. It currently trades at $14.96.

Is now the time to buy Sleep Number? Access our full analysis of the earnings results here, it’s free.

Arhaus (NASDAQ: ARHS)

With an aesthetic that features natural materials such as reclaimed wood, Arhaus (NASDAQ: ARHS) is a high-end furniture retailer that sells everything from sofas to rugs to bookcases.

Arhaus reported revenues of $319.1 million, down 2.2% year on year, falling short of analysts’ expectations by 3.1%. It was a disappointing quarter as it posted full-year EBITDA guidance missing analysts’ expectations.

Interestingly, the stock is up 22.3% since the results and currently trades at $11.15.

Read our full analysis of Arhaus’s results here.

RH (NYSE: RH)

Formerly known as Restoration Hardware, RH (NYSE: RH) is a specialty retailer that exclusively sells its own brand of high-end furniture and home decor.

RH reported revenues of $811.7 million, up 8.1% year on year. This number was in line with analysts’ expectations. Aside from that, it was a softer quarter as it recorded a significant miss of analysts’ EBITDA estimates.

RH pulled off the fastest revenue growth among its peers. The stock is down 10.8% since reporting and currently trades at $340.

Read our full, actionable report on RH here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.