Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Bill.com (NYSE: BILL) and the best and worst performers in the finance and hr software industry.

Organizations are constantly looking to improve organizational efficiencies, whether it is financial planning, tax management or payroll. Finance and HR software benefit from the SaaS-ification of businesses, large and small, who much prefer the flexibility of cloud-based, web-browser delivered software paid for on a subscription basis than the hassle and expense of purchasing and managing on-premise enterprise software.

The 14 finance and HR software stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was 1.4% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 16% since the latest earnings results.

Bill.com (NYSE: BILL)

Started by René Lacerte in 2006 after selling his previous payroll and accounting software company PayCycle to Intuit, Bill.com (NYSE: BILL) is a software as a service platform that aims to make payments and billing processes easier for small and medium-sized businesses.

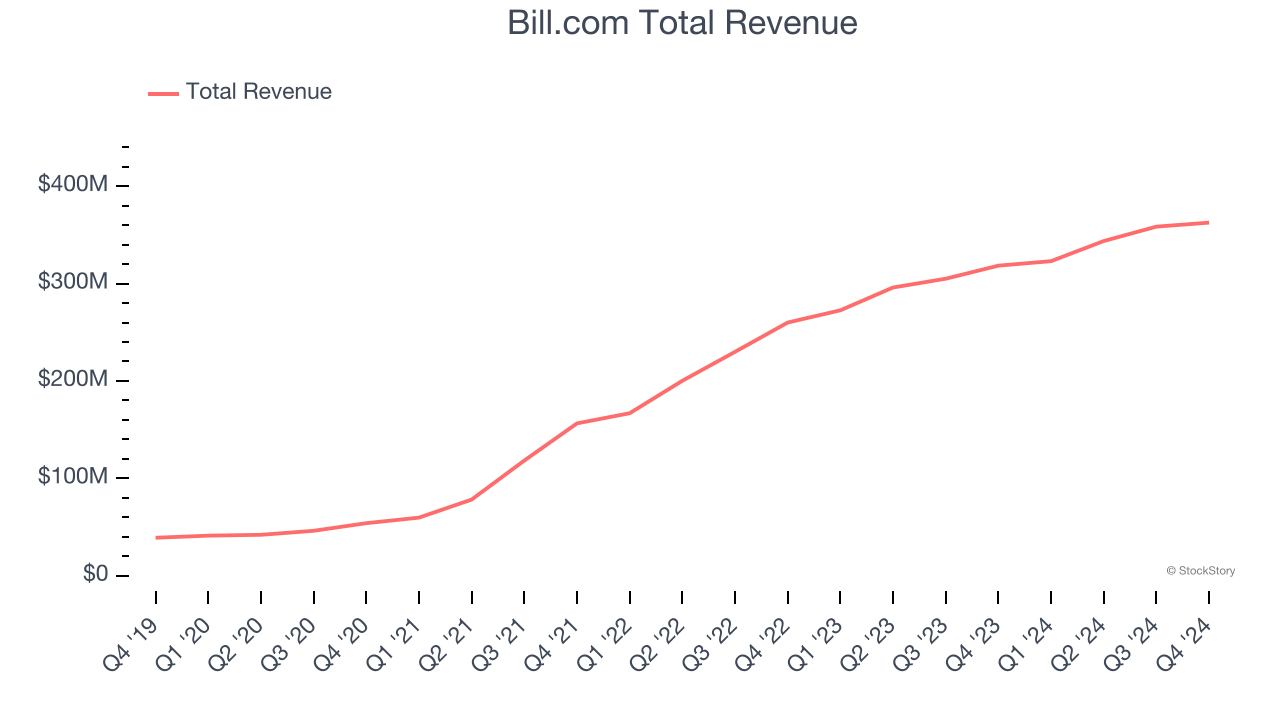

Bill.com reported revenues of $362.6 million, up 13.9% year on year. This print was in line with analysts’ expectations, and overall, it was a very strong quarter for the company with EPS guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ EBITDA estimates.

The stock is down 56.8% since reporting and currently trades at $41.61.

Is now the time to buy Bill.com? Access our full analysis of the earnings results here, it’s free.

Best Q4: Workday (NASDAQ: WDAY)

Founded by industry veterans Aneel Bushri and Dave Duffield after their former company PeopleSoft was acquired by Oracle in a hostile takeover, Workday (NASDAQ: WDAY) provides cloud-based software for organizations to manage and plan finance and human resources.

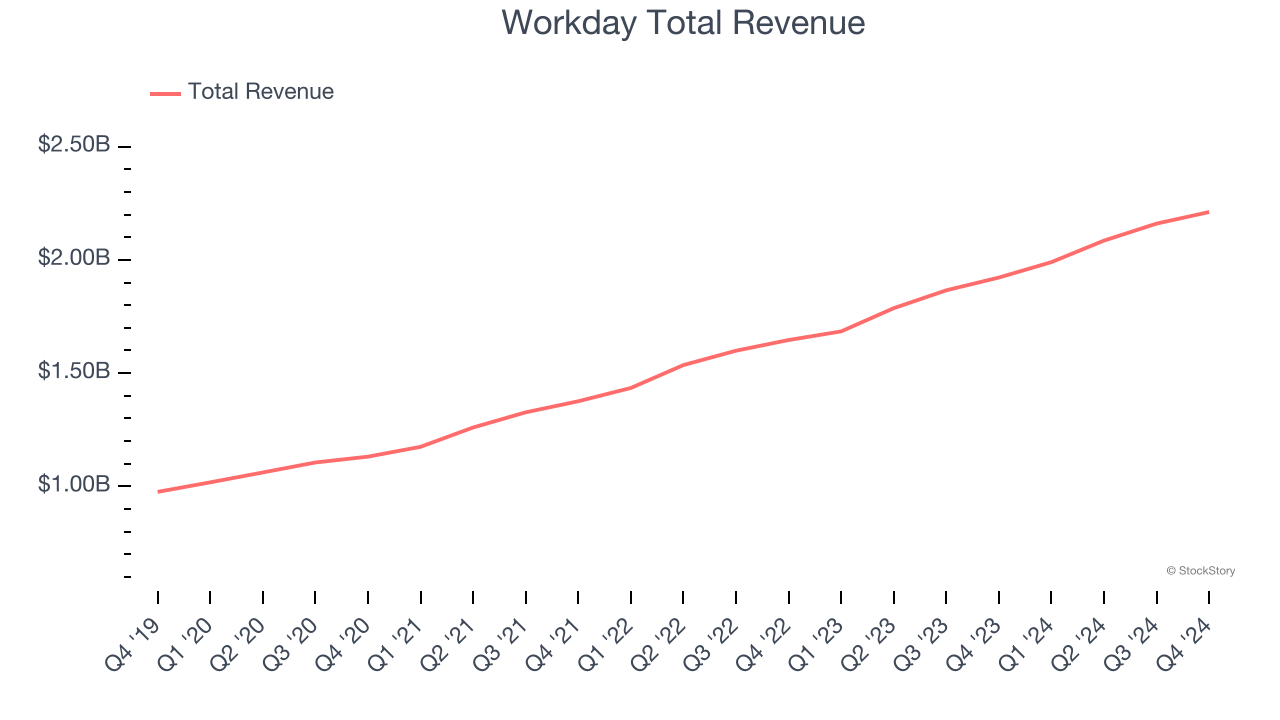

Workday reported revenues of $2.21 billion, up 15% year on year, outperforming analysts’ expectations by 1.3%. The business had a very strong quarter with an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ billings estimates.

The stock is down 10.3% since reporting. It currently trades at $228.80.

Is now the time to buy Workday? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Flywire (NASDAQ: FLYW)

Originally created to process international tuition payments for universities, Flywire (NASDAQ: FLYW) is a cross border payments processor and software platform focusing on complex, high-value transactions like education, healthcare and B2B payments.

Flywire reported revenues of $117.6 million, up 22.4% year on year, falling short of analysts’ expectations by 4.9%. It was a softer quarter as it posted revenue guidance for next quarter slightly missing analysts’ expectations.

Flywire delivered the fastest revenue growth but had the weakest performance against analyst estimates in the group. As expected, the stock is down 46.5% since the results and currently trades at $9.44.

Read our full analysis of Flywire’s results here.

Marqeta (NASDAQ: MQ)

Founded by CEO Jason Gardner in 2009, Marqeta (NASDAQ: MQ) is an innovative card issuer that provides companies with the ability to issue and process virtual, physical, and tokenized credit and debit cards.

Marqeta reported revenues of $135.8 million, up 14.3% year on year. This result surpassed analysts’ expectations by 3%. It was a very strong quarter as it also put up an impressive beat of analysts’ EBITDA estimates.

The stock is up 9.3% since reporting and currently trades at $3.81.

Read our full, actionable report on Marqeta here, it’s free.

Paycom (NYSE: PAYC)

Founded in 1998 as one of the first online payroll companies, Paycom (NYSE: PAYC) provides software for small and medium-sized businesses (SMBs) to manage their payroll and HR needs in one place.

Paycom reported revenues of $493.8 million, up 13.6% year on year. This number beat analysts’ expectations by 2.6%. Overall, it was a strong quarter as it also recorded an impressive beat of analysts’ EBITDA estimates.

The stock is up 5.5% since reporting and currently trades at $218.30.

Read our full, actionable report on Paycom here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.