Since June 2020, the S&P 500 has delivered a total return of 88%. But one standout stock has more than doubled the market - over the past five years, Sanmina has surged 220% to $87.45 per share. Its momentum hasn’t stopped as it’s also gained 10.2% in the last six months, beating the S&P by 10.7%.

Is now the time to buy Sanmina, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Sanmina Will Underperform?

We’re glad investors have benefited from the price increase, but we're cautious about Sanmina. Here are three reasons why you should be careful with SANM and a stock we'd rather own.

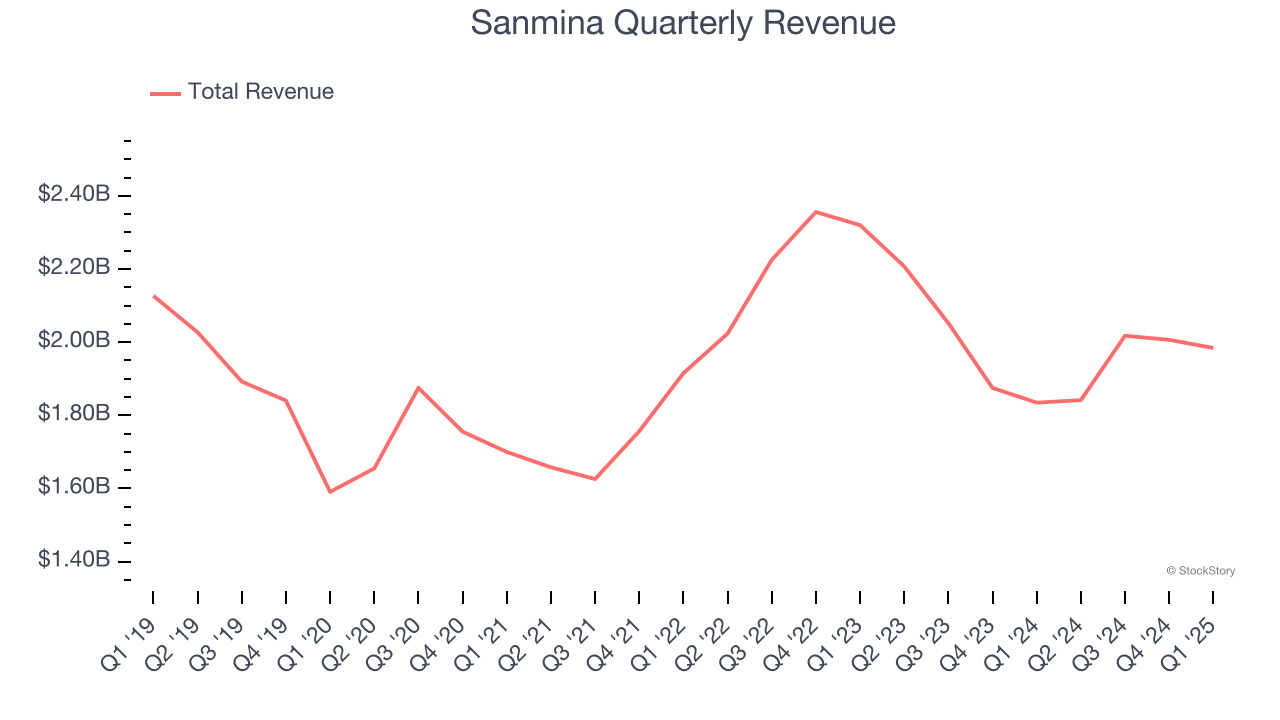

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Sanmina’s 1.3% annualized revenue growth over the last five years was weak. This was below our standards.

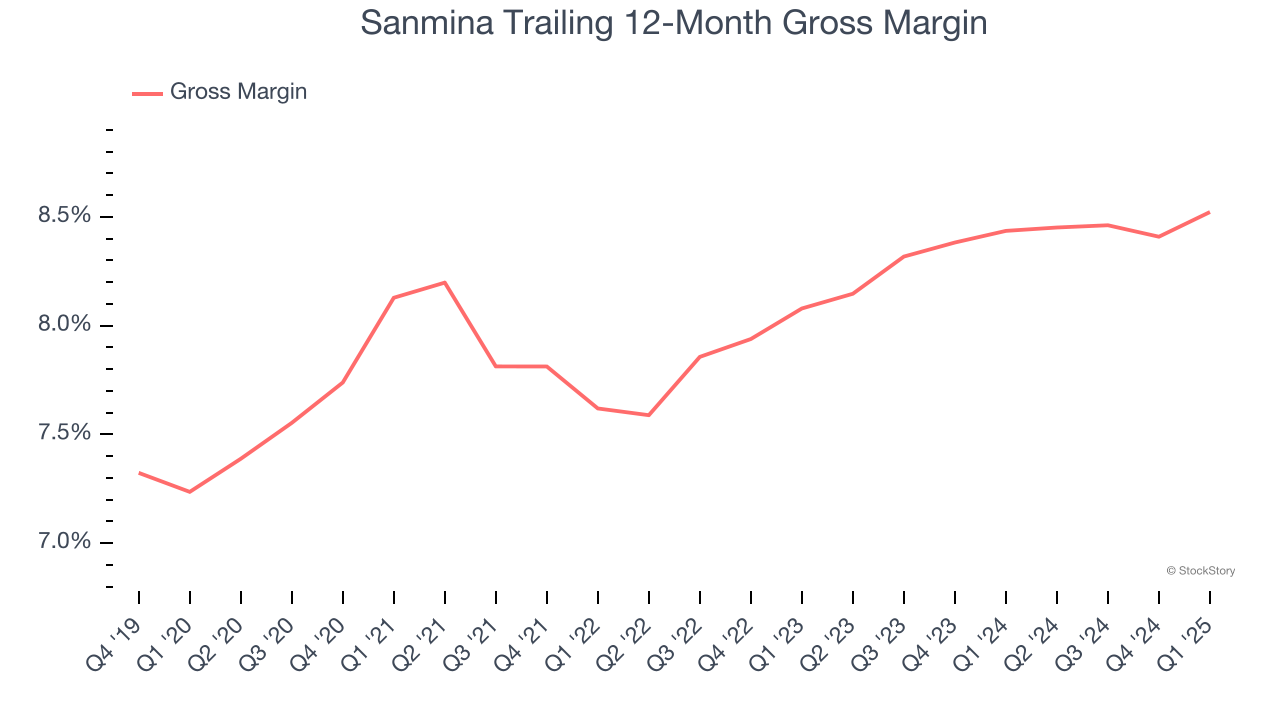

2. Low Gross Margin Reveals Weak Structural Profitability

At StockStory, we prefer high gross margin businesses because they indicate the company has pricing power or differentiated products, giving it a chance to generate higher operating profits.

Sanmina has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 8.2% gross margin over the last five years. Said differently, Sanmina had to pay a chunky $91.83 to its suppliers for every $100 in revenue.

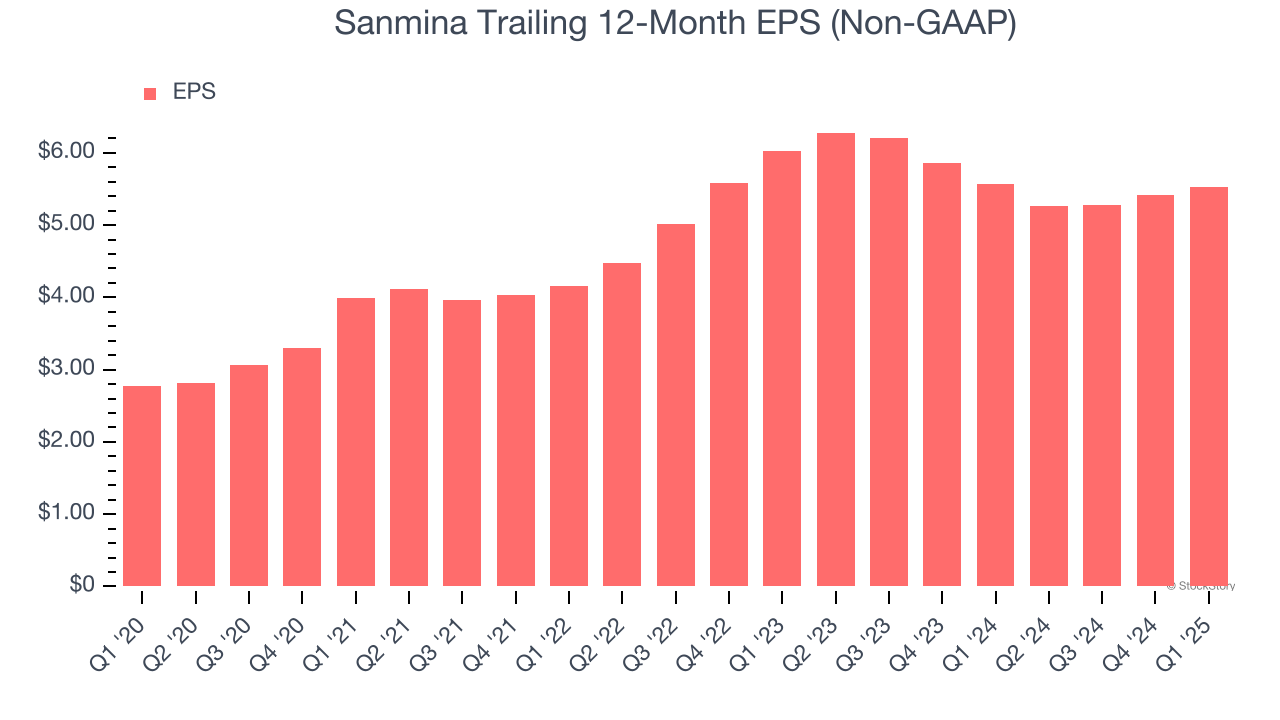

3. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Sanmina, its EPS and revenue declined by 4.2% and 6.2% annually over the last two years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Sanmina’s low margin of safety could leave its stock price susceptible to large downswings.

Final Judgment

Sanmina doesn’t pass our quality test. With its shares topping the market in recent months, the stock trades at 13.1× forward P/E (or $87.45 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are superior stocks to buy right now. We’d recommend looking at the most dominant software business in the world.

High-Quality Stocks for All Market Conditions

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.