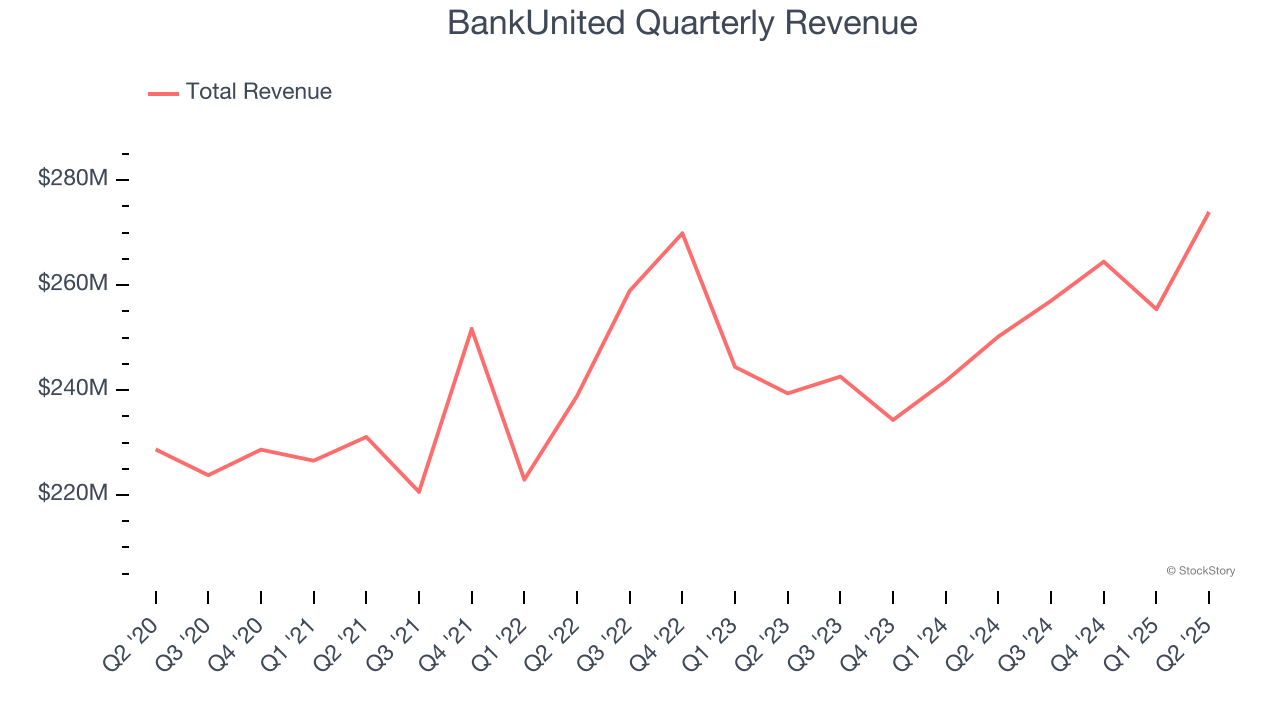

Regional banking company BankUnited (NYSE: BKU) beat Wall Street’s revenue expectations in Q2 CY2025, with sales up 9.5% year on year to $273.9 million. Its GAAP profit of $0.91 per share was 15.3% above analysts’ consensus estimates.

Is now the time to buy BankUnited? Find out by accessing our full research report, it’s free.

BankUnited (BKU) Q2 CY2025 Highlights:

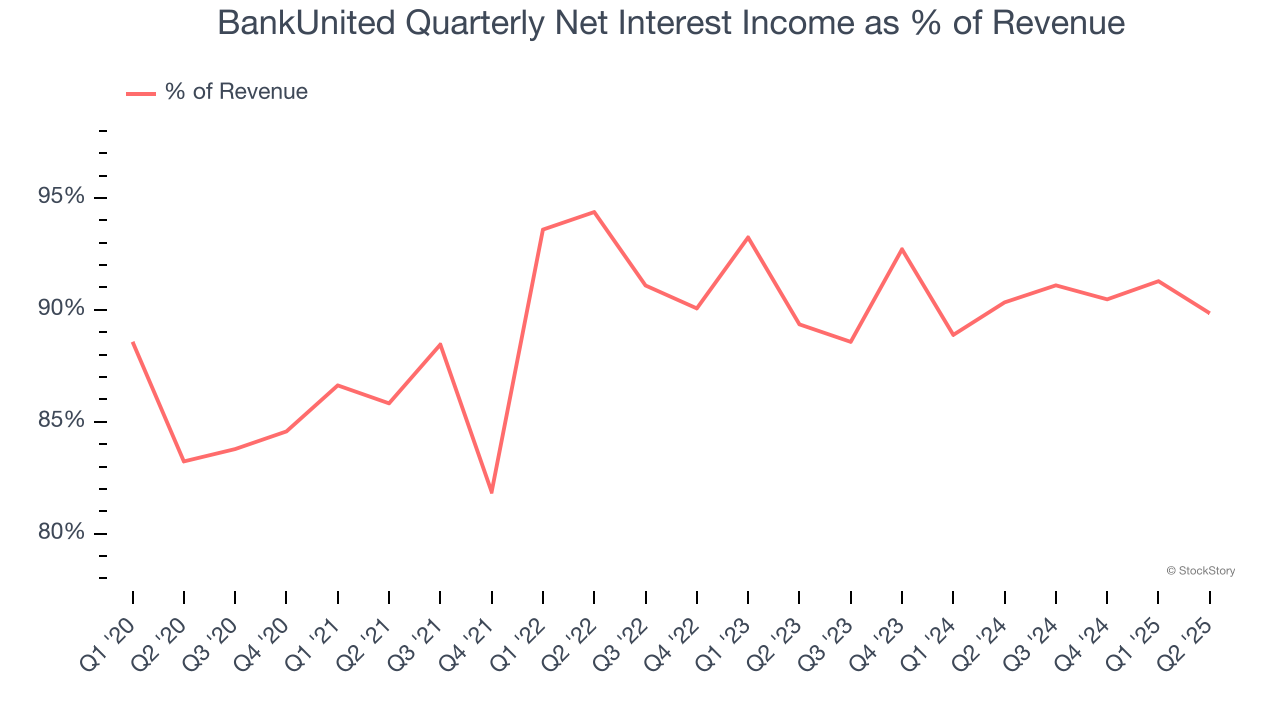

- Net Interest Income: $246.1 million vs analyst estimates of $244.1 million (8.9% year-on-year growth, 0.8% beat)

- Net Interest Margin: 2.9% vs analyst estimates of 2.9% (21 basis point year-on-year increase, 3 bps beat)

- Revenue: $273.9 million vs analyst estimates of $265.9 million (9.5% year-on-year growth, 3% beat)

- EPS (GAAP): $0.91 vs analyst estimates of $0.79 (15.3% beat)

- Market Capitalization: $2.91 billion

"This was an outstanding quarter - we continued to deliver on key priorities with strong NIDDA growth and continued margin expansion," said Rajinder Singh, Chairman, President and Chief Executive Officer.

Company Overview

Born from the ashes of a failed Florida thrift during the 2009 financial crisis, BankUnited (NYSE: BKU) is a regional bank that provides commercial lending, deposit services, and treasury solutions to businesses and consumers primarily in Florida and the New York metropolitan area.

Sales Growth

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income.

Over the last five years, BankUnited grew its revenue at a mediocre 3.6% compounded annual growth rate. This fell short of our benchmark for the bank sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. BankUnited’s recent performance shows its demand has slowed as its annualized revenue growth of 1.9% over the last two years was below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

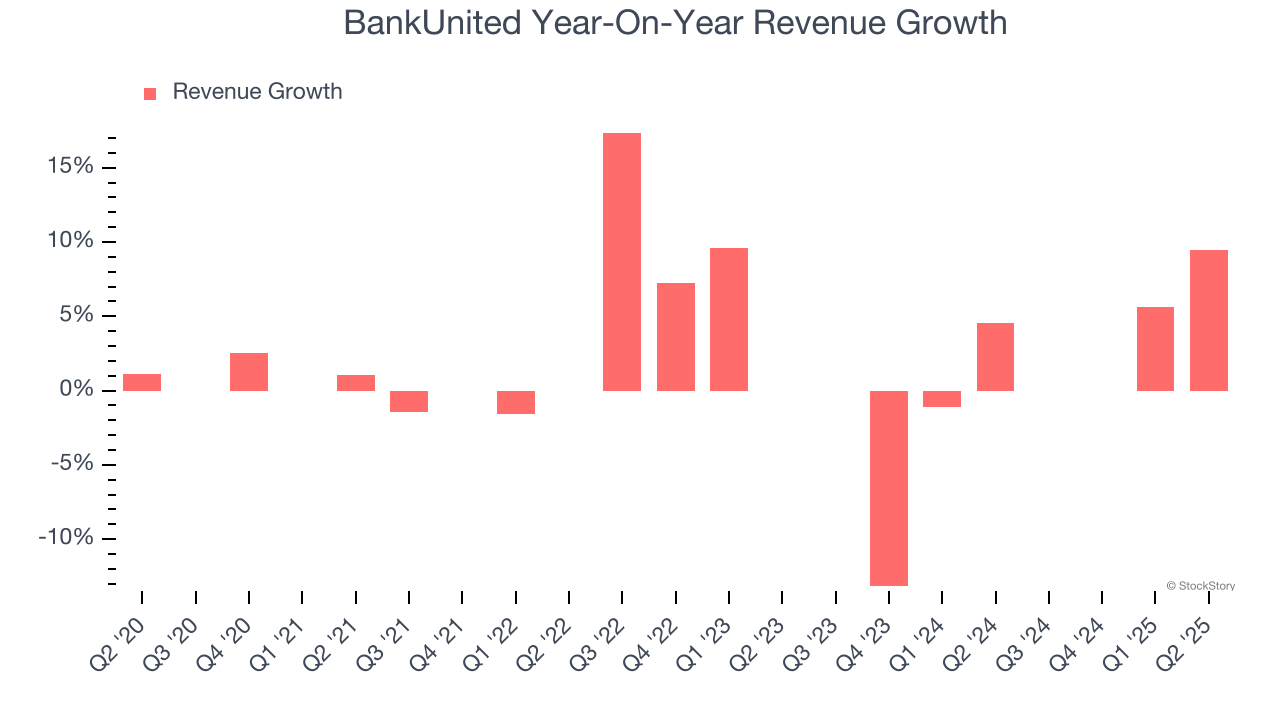

This quarter, BankUnited reported year-on-year revenue growth of 9.5%, and its $273.9 million of revenue exceeded Wall Street’s estimates by 3%.

Net interest income made up 89.3% of the company’s total revenue during the last five years, meaning BankUnited barely relies on non-interest income to drive its overall growth.

Our experience and research show the market cares primarily about a bank’s net interest income growth as non-interest income is considered a lower-quality and non-recurring revenue source.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

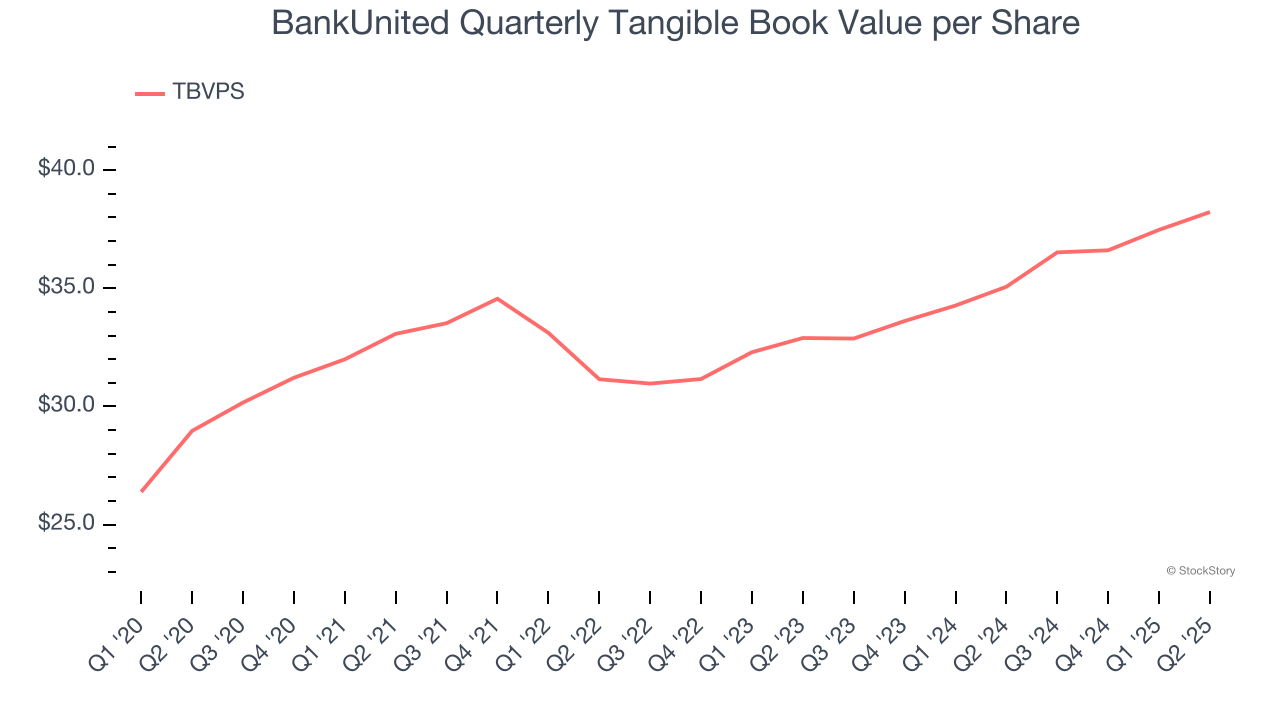

Tangible Book Value Per Share (TBVPS)

The balance sheet drives banking profitability since earnings flow from the spread between borrowing and lending rates. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark. By excluding intangible assets with uncertain liquidation values, this metric captures real, liquid net worth per share. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

BankUnited’s TBVPS grew at a decent 5.7% annual clip over the last five years. TBVPS growth has accelerated recently, growing by 7.8% annually over the last two years from $32.90 to $38.23 per share.

Over the next 12 months, Consensus estimates call for BankUnited’s TBVPS to grow by 5.4% to $40.31, mediocre growth rate.

Key Takeaways from BankUnited’s Q2 Results

We enjoyed seeing BankUnited beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $38.72 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.