Over the past six months, Macy’s shares (currently trading at $13.75) have posted a disappointing 10.7% loss, well below the S&P 500’s 5.8% gain. This might have investors contemplating their next move.

Is there a buying opportunity in Macy's, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Macy's Will Underperform?

Even with the cheaper entry price, we're cautious about Macy's. Here are three reasons why you should be careful with M and a stock we'd rather own.

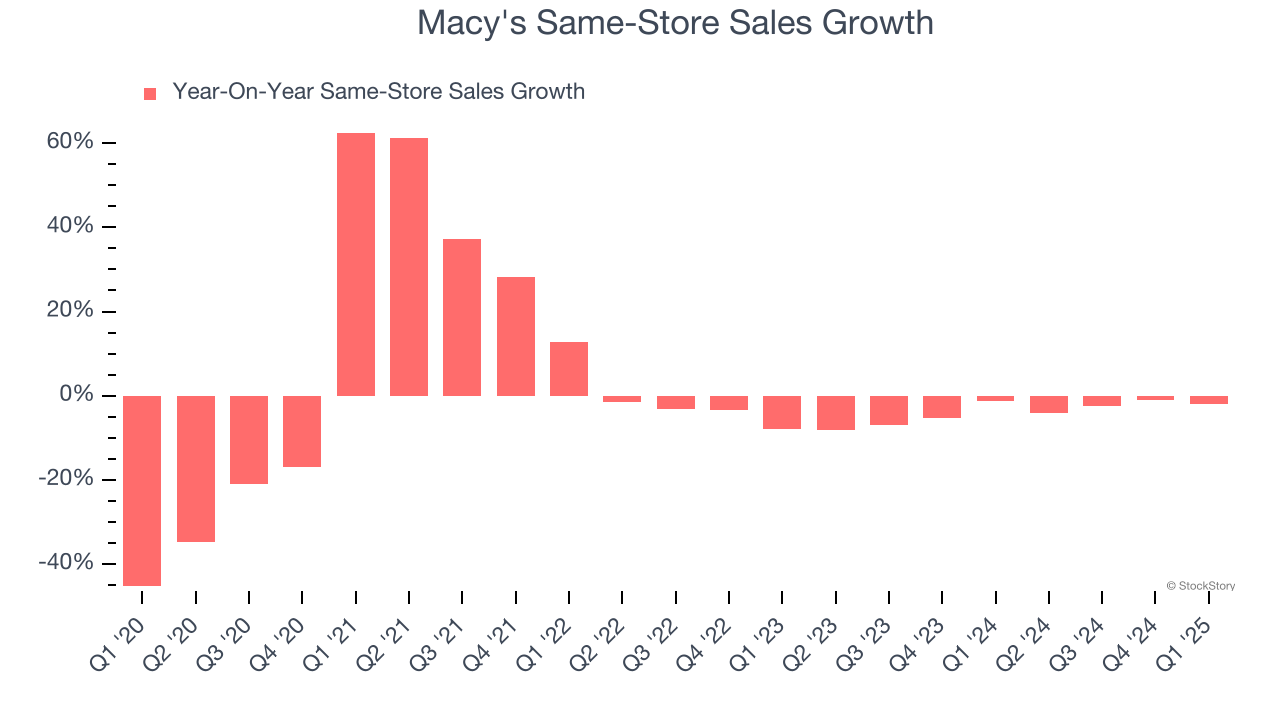

1. Shrinking Same-Store Sales Indicate Waning Demand

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Macy’s demand has been shrinking over the last two years as its same-store sales have averaged 3.9% annual declines.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Macy’s revenue to drop by 4.3%, a decrease from This projection is underwhelming and indicates its products will see some demand headwinds.

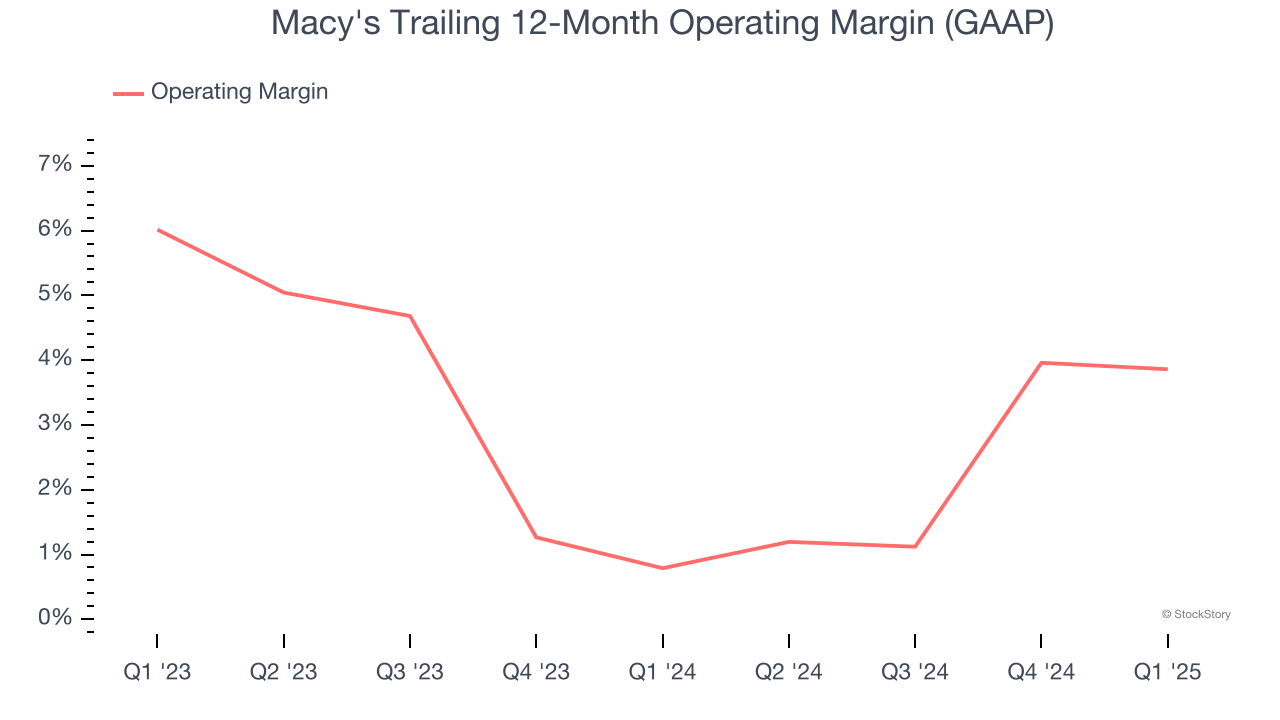

3. Weak Operating Margin Could Cause Trouble

Operating margin is a key profitability metric because it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

Macy's was profitable over the last two years but held back by its large cost base. Its average operating margin of 2.3% was weak for a consumer retail business. This result is surprising given its high gross margin as a starting point.

Final Judgment

Macy's falls short of our quality standards. Following the recent decline, the stock trades at 7.1× forward P/E (or $13.75 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. We’d suggest looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of Macy's

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.