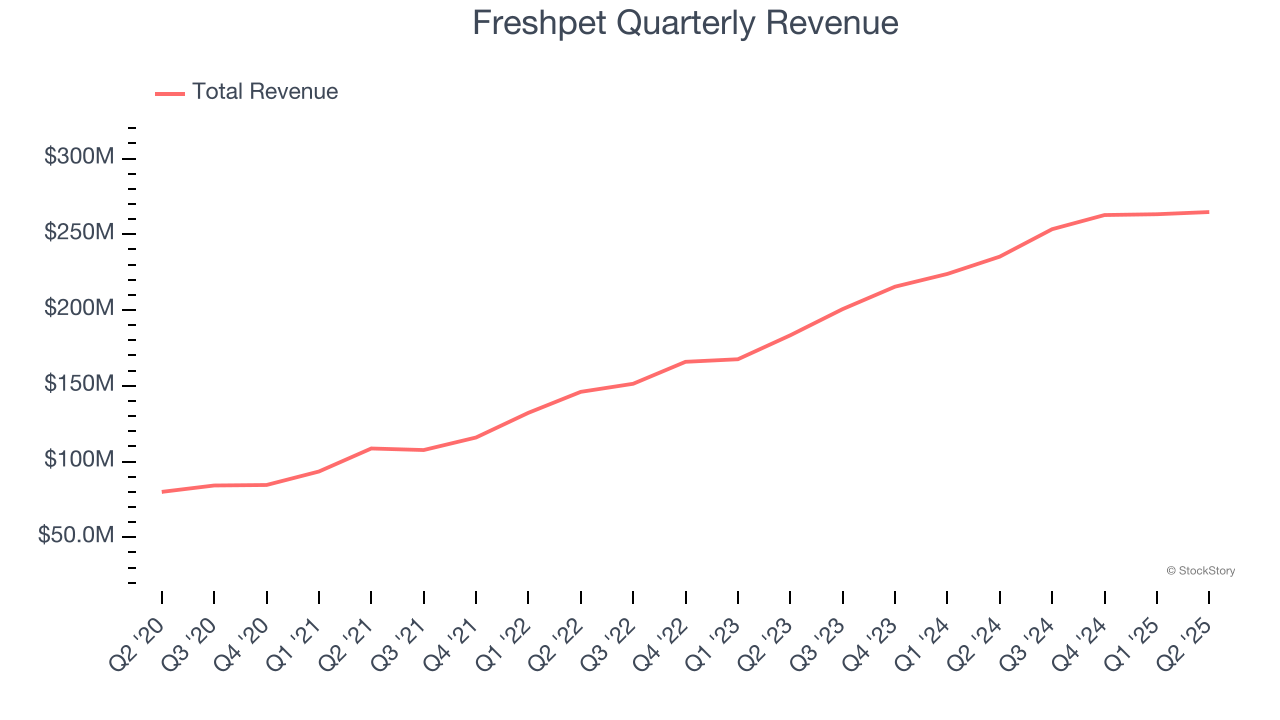

Pet food company Freshpet (NASDAQ: FRPT) fell short of the market’s revenue expectations in Q2 CY2025, but sales rose 12.5% year on year to $264.7 million. Its GAAP profit of $0.33 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Freshpet? Find out by accessing our full research report, it’s free.

Freshpet (FRPT) Q2 CY2025 Highlights:

- Revenue: $264.7 million vs analyst estimates of $268.8 million (12.5% year-on-year growth, 1.5% miss)

- EPS (GAAP): $0.33 vs analyst estimates of $0.09 (significant beat)

- Adjusted EBITDA: $44.4 million vs analyst estimates of $38.93 million (16.8% margin, 14.1% beat)

- EBITDA guidance for the full year is $200 million at the midpoint, above analyst estimates of $193.9 million

- Operating Margin: 6.7%, up from -0.7% in the same quarter last year

- Free Cash Flow was $445,000, up from -$5.91 million in the same quarter last year

- Organic Revenue was up 12.5% year on year

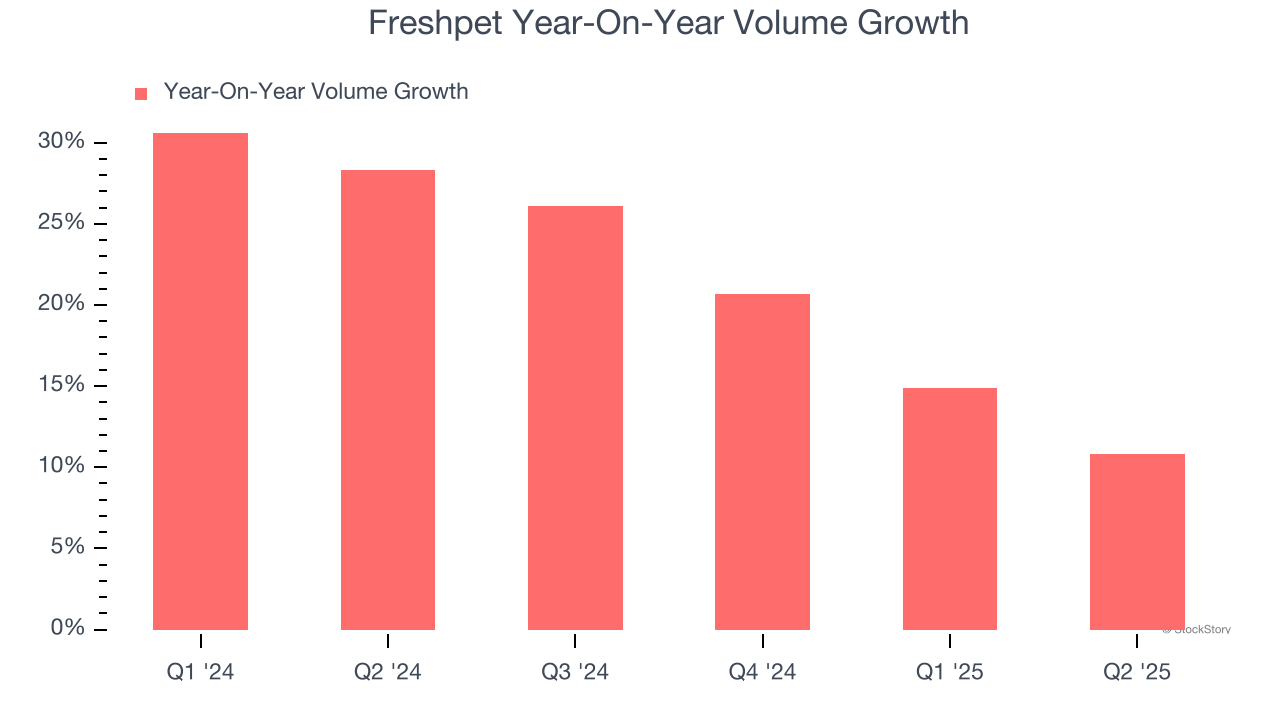

- Sales Volumes rose 10.8% year on year (28.3% in the same quarter last year)

- Market Capitalization: $3.21 billion

"Against a more challenging consumer sentiment backdrop, we continue to significantly outperform the dog food category - delivering both category leading sales growth and strong improvements in operations," commented Billy Cyr, Freshpet’s Chief Executive Officer.

Company Overview

Standing out from typical processed pet foods, Freshpet (NASDAQ: FRPT) is a pet food company whose product portfolio includes natural meals and treats for dogs and cats.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $1.04 billion in revenue over the past 12 months, Freshpet is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, Freshpet’s 27.7% annualized revenue growth over the last three years was exceptional as consumers bought more of its products.

This quarter, Freshpet’s revenue grew by 12.5% year on year to $264.7 million but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 15.6% over the next 12 months, a deceleration versus the last three years. Still, this projection is admirable and indicates the market is forecasting success for its products.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Freshpet’s average quarterly volume growth of 21.9% over the last two years has beaten the competition by a long shot. This is great because companies with significant volume growth are needles in a haystack in the stable consumer staples sector.

In Freshpet’s Q2 2025, sales volumes jumped 10.8% year on year. This result was a meaningful deceleration from its historical levels. We’ll be watching Freshpet closely to see if it can reaccelerate demand for its products.

Key Takeaways from Freshpet’s Q2 Results

We were impressed by how significantly Freshpet blew past analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its gross margin missed and its organic revenue fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 1.9% to $67.11 immediately following the results.

Freshpet had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.