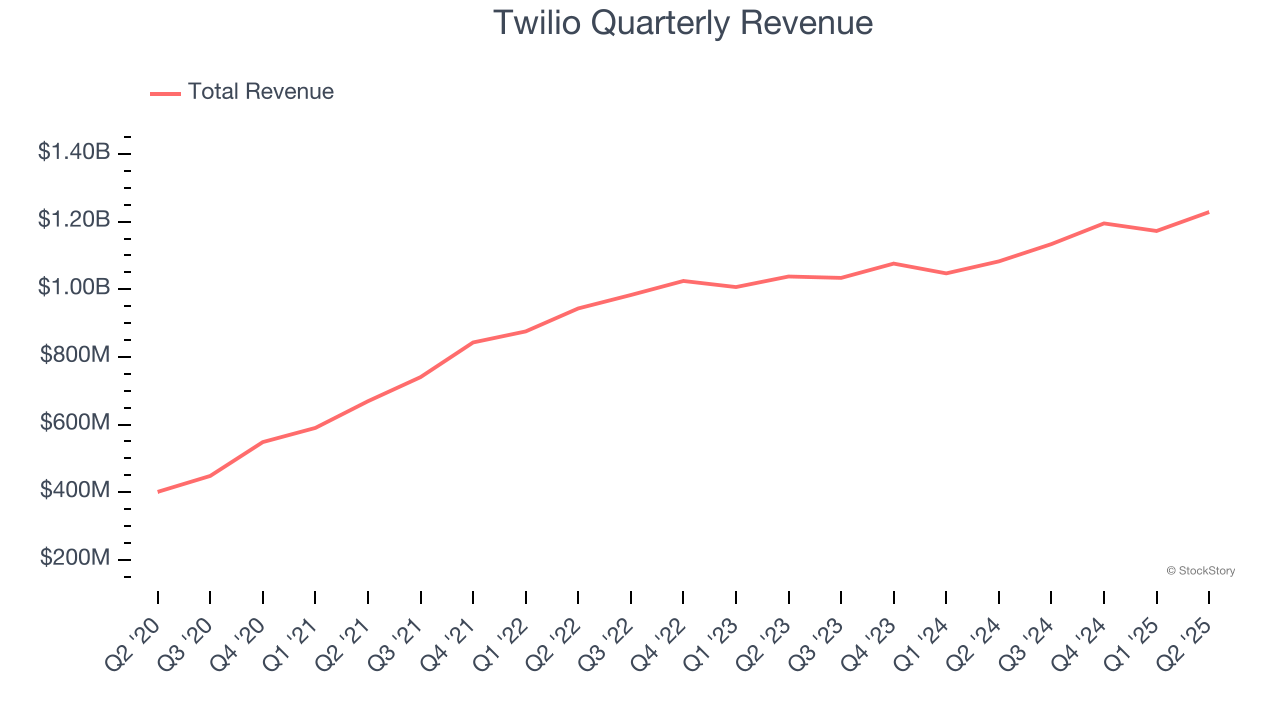

Cloud communications infrastructure company Twilio (NYSE: TWLO) announced better-than-expected revenue in Q2 CY2025, with sales up 13.5% year on year to $1.23 billion. On top of that, next quarter’s revenue guidance ($1.25 billion at the midpoint) was surprisingly good and 3% above what analysts were expecting. Its non-GAAP profit of $1.19 per share was 13.3% above analysts’ consensus estimates.

Is now the time to buy Twilio? Find out by accessing our full research report, it’s free.

Twilio (TWLO) Q2 CY2025 Highlights:

- Revenue: $1.23 billion vs analyst estimates of $1.19 billion (13.5% year-on-year growth, 3.4% beat)

- Adjusted EPS: $1.19 vs analyst estimates of $1.05 (13.3% beat)

- Adjusted Operating Income: $220.5 million vs analyst estimates of $202 million (18% margin, 9.2% beat)

- Revenue Guidance for Q3 CY2025 is $1.25 billion at the midpoint, above analyst estimates of $1.21 billion

- Adjusted EPS guidance for Q3 CY2025 is $1.04 at the midpoint, below analyst estimates of $1.15

- Operating Margin: 3%, up from -1.8% in the same quarter last year

- Free Cash Flow Margin: 21.4%, up from 15.2% in the previous quarter

- Customers: 349,000, up from 335,000 in the previous quarter

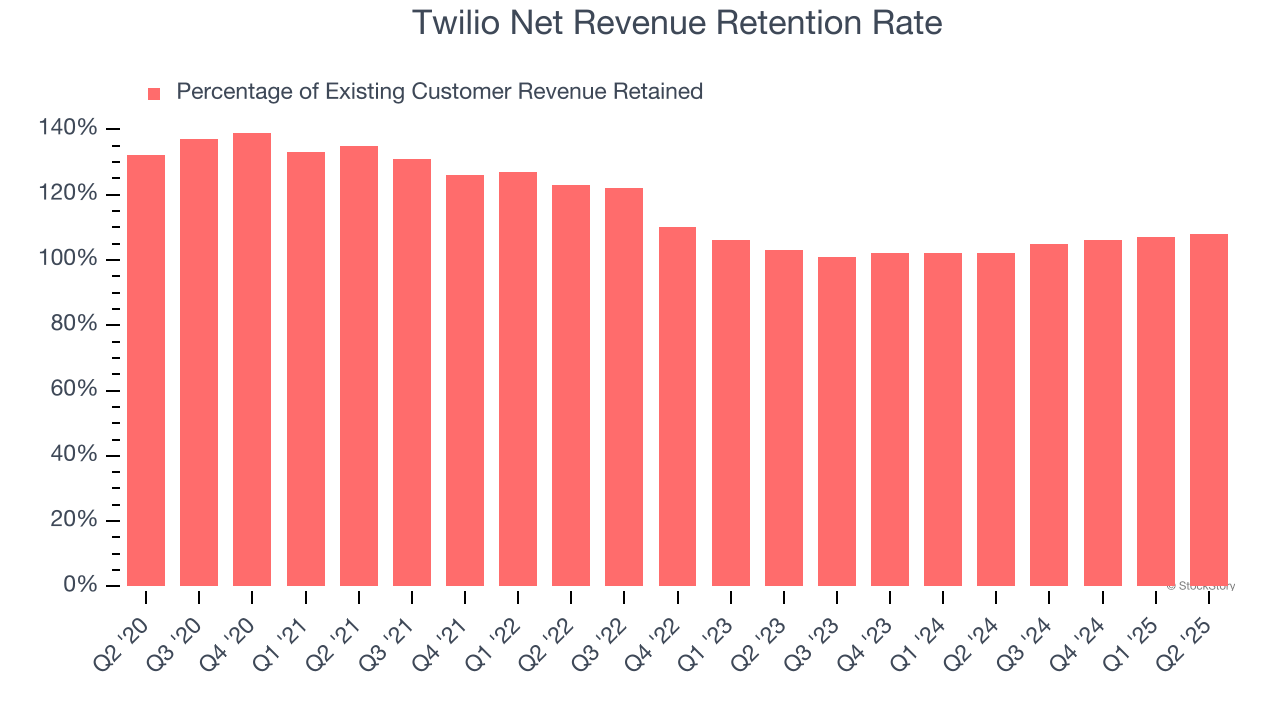

- Net Revenue Retention Rate: 108%, up from 107% in the previous quarter

- Market Capitalization: $19.88 billion

“The company’s focus and execution is paying off as Q2 marked another quarter of accelerated year-over-year revenue growth as well as record non-GAAP income from operations and free cash flow,” said Khozema Shipchandler, CEO of Twilio.

Company Overview

Founded in 2008 by Jeff Lawson, a former engineer at Amazon, Twilio (NYSE: TWLO) is a software as a service platform that makes it really easy for software developers to use text messaging, voice calls and other forms of communication in their apps.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Twilio grew its sales at a 11.6% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the software sector, which enjoys a number of secular tailwinds.

This quarter, Twilio reported year-on-year revenue growth of 13.5%, and its $1.23 billion of revenue exceeded Wall Street’s estimates by 3.4%. Company management is currently guiding for a 10.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.7% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and implies its products and services will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Twilio’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 107% in Q2. This means Twilio would’ve grown its revenue by 6.5% even if it didn’t win any new customers over the last 12 months.

Trending up over the last year, Twilio has a decent net retention rate, showing us that its customers not only tend to stick around but also get increasing value from its software over time.

Key Takeaways from Twilio’s Q2 Results

We enjoyed seeing Twilio’s customer growth accelerate this quarter. We were also glad its revenue guidance for next quarter exceeded Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed. Overall, this print had some key positives. The market seemed to be hoping for more, and the stock traded down 10.6% to $109.65 immediately after reporting.

Is Twilio an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.