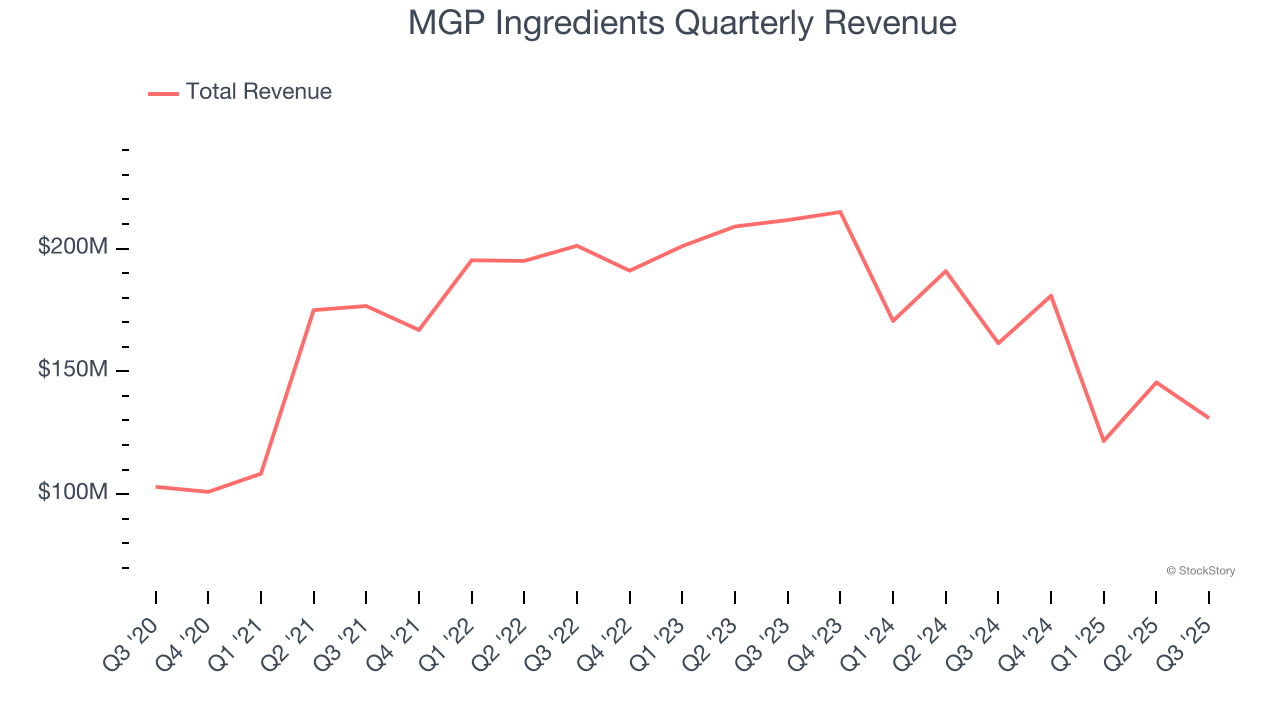

Food and beverage supplier MGP Ingredients (NASDAQ: MGPI) beat Wall Street’s revenue expectations in Q3 CY2025, but sales fell by 18.9% year on year to $130.9 million. On the other hand, the company’s full-year revenue guidance of $530 million at the midpoint came in 0.5% below analysts’ estimates. Its non-GAAP profit of $0.85 per share was 40.9% above analysts’ consensus estimates.

Is now the time to buy MGP Ingredients? Find out by accessing our full research report, it’s free for active Edge members.

MGP Ingredients (MGPI) Q3 CY2025 Highlights:

- Revenue: $130.9 million vs analyst estimates of $128.2 million (18.9% year-on-year decline, 2.1% beat)

- Adjusted EPS: $0.85 vs analyst estimates of $0.60 (40.9% beat)

- Adjusted EBITDA: $32.26 million vs analyst estimates of $25.56 million (24.6% margin, 26.2% beat)

- The company reconfirmed its revenue guidance for the full year of $530 million at the midpoint

- Management raised its full-year Adjusted EPS guidance to $2.68 at the midpoint, a 2.9% increase

- EBITDA guidance for the full year is $112.5 million at the midpoint, above analyst estimates of $109.4 million

- Operating Margin: 16.1%, down from 20.2% in the same quarter last year

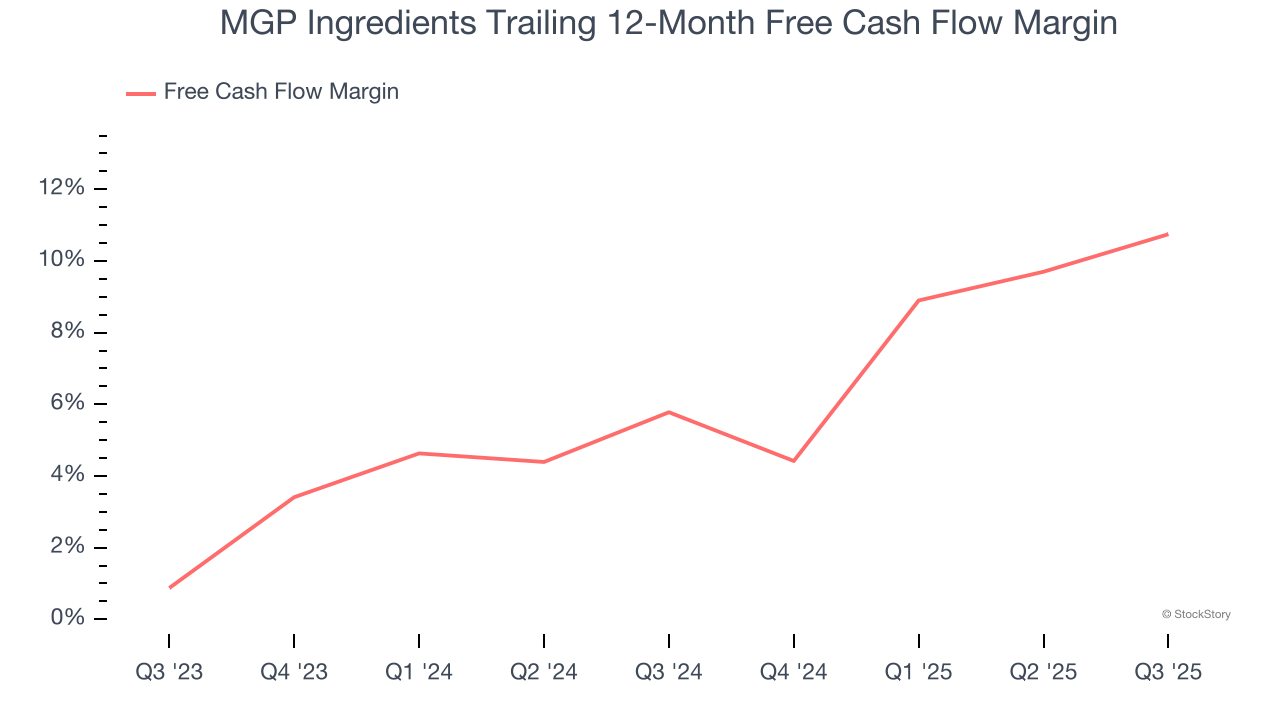

- Free Cash Flow Margin: 21.1%, up from 15.2% in the same quarter last year

- Market Capitalization: $504 million

Company Overview

Headquartered in Atchison, Kansas, MGP Ingredients (NASDAQ: MGPI) is a leading supplier of high-quality ingredients to the food and beverage industry

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $578.9 million in revenue over the past 12 months, MGP Ingredients is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, MGP Ingredients struggled to generate demand over the last three years. Its sales dropped by 8.6% annually, a rough starting point for our analysis.

This quarter, MGP Ingredients’s revenue fell by 18.9% year on year to $130.9 million but beat Wall Street’s estimates by 2.1%.

Looking ahead, sell-side analysts expect revenue to decline by 11.7% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and implies its products will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

MGP Ingredients has shown impressive cash profitability, driven by its attractive business model that gives it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 8% over the last two years, better than the broader consumer staples sector.

Taking a step back, we can see that MGP Ingredients’s margin expanded by 5 percentage points over the last year. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

MGP Ingredients’s free cash flow clocked in at $27.57 million in Q3, equivalent to a 21.1% margin. This result was good as its margin was 5.9 percentage points higher than in the same quarter last year, building on its favorable historical trend.

Key Takeaways from MGP Ingredients’s Q3 Results

It was good to see MGP Ingredients beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year revenue guidance slightly missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $23.67 immediately after reporting.

So should you invest in MGP Ingredients right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.