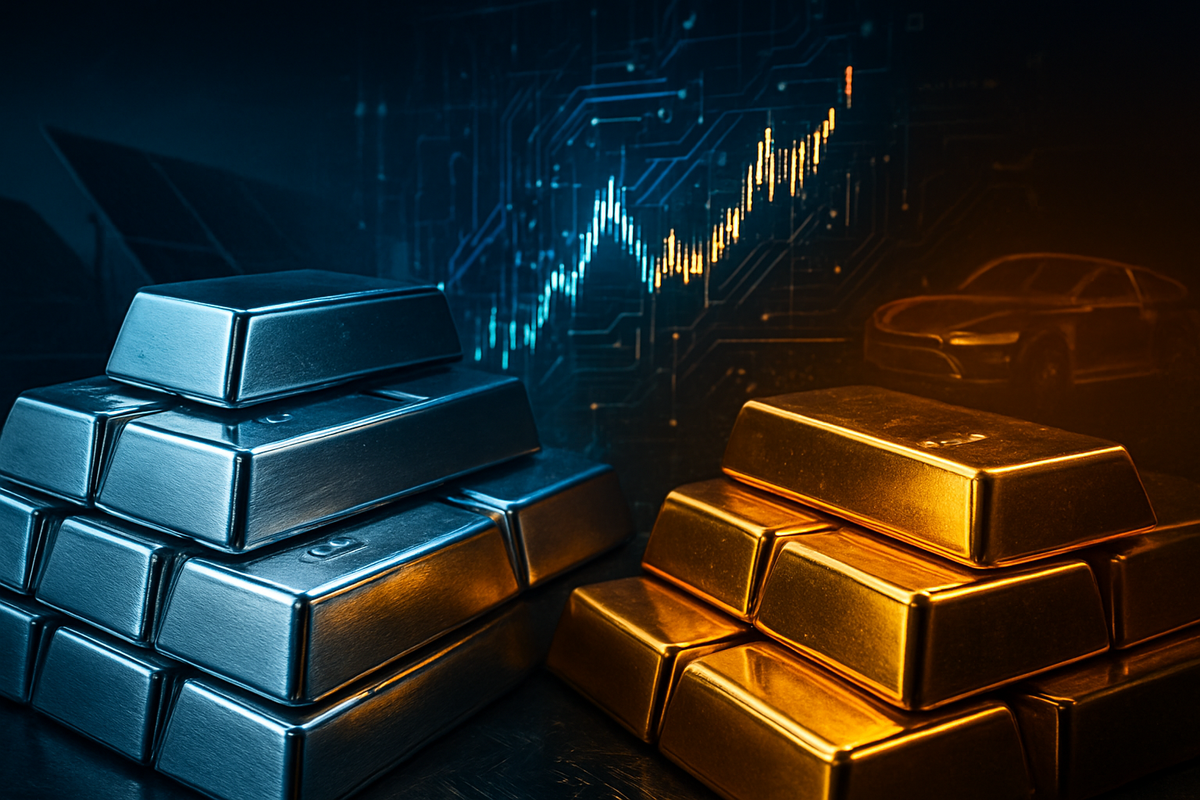

As 2025 draws to a close, the global financial landscape has been fundamentally reshaped by what analysts are calling the "Gold and Silver Revolution." In a year marked by geopolitical volatility and a tectonic shift in industrial demand, precious metals have staged a historic rally that has left traditional equity markets in the dust. While gold has reached breathtaking new heights, it is silver that has stolen the spotlight, delivering a staggering 128% year-to-date return that has redefined its status from a mere monetary metal to a mission-critical industrial commodity.

The immediate implications of this surge are being felt across every sector of the economy. For investors, the rally has provided a massive hedge against a backdrop of escalating trade wars and currency debasement. However, for industrial giants in the green technology and automotive sectors, the "precious metal squeeze" has become a dual-edged sword, threatening profit margins while simultaneously accelerating a new wave of technological innovation. With silver prices crossing the $65 per ounce threshold and gold breaching $4,300, the market is witnessing a valuation reset that could persist for years to come.

The Perfect Storm: A Timeline of the 2025 Surge

The meteoric rise of precious metals in 2025 was not the result of a single event, but rather a "perfect storm" of structural and geopolitical factors that converged throughout the year. The rally began in earnest during the first quarter, fueled by a resurgence in global trade tensions. As major economies implemented aggressive tariff regimes—including a brief but chaotic 39% tariff on Swiss-refined gold—investors fled to the safety of physical assets. This flight to quality was further intensified by a "complete blockade" of Venezuelan oil tankers and escalating U.S.-China trade frictions, which cast a long shadow over global economic stability.

A pivotal moment arrived on July 1, 2025, with the implementation of the updated Basel III Agreement. This regulatory shift allowed central banks to reclassify physical gold as a Tier 1 High-Quality Liquid Asset (HQLA) with a 0% risk weight. The move triggered a massive wave of institutional buying, as central banks worldwide scrambled to diversify their reserves away from the U.S. dollar, purchasing over 1,100 tons of gold in the second half of the year alone. This institutional floor provided the launchpad for gold to climb toward its December peak of $4,381 per ounce.

While gold provided the foundation, silver provided the fireworks. Throughout 2025, the "white metal" shattered records as it faced its fifth consecutive year of supply deficits. The industrial demand for silver, driven by the rapid expansion of solar power and the AI revolution, finally outstripped the market's ability to supply it. By mid-December, silver had surged from its January opening to a high of $66.50 per ounce. Initial market reactions were a mix of euphoria among bullion holders and panic among industrial buyers, leading to a frenzy in the futures markets that saw trading volumes reach all-time highs.

The Winners and Losers of the Metal Squeeze

The financial windfall of 2025 has been most evident in the balance sheets of major mining corporations. Newmont Corporation (NYSE: NEM), the world’s largest gold producer, saw its stock price soar by over 135% this year, reaching all-time highs above $100 per share. The company reported a record free cash flow of $1.6 billion in the third quarter alone, underscoring the immense profitability of gold mining at $4,000+ prices. Similarly, Pan American Silver Corp. (NYSE: PAAS) emerged as a primary beneficiary of the silver boom, with its shares climbing nearly 100% year-to-date. Its strategic positioning in high-growth silver markets allowed it to post revenues of $884.4 million in Q3, a testament to the metal's new valuation floor.

Streaming and royalty companies have also thrived in this environment. Wheaton Precious Metals Corp. (NYSE: WPM) reported record-breaking earnings and cash flow, as its low-cost model allowed it to capture the full upside of rising prices without the inflationary pressures of direct mining operations. For pure-play silver investors, First Majestic Silver Corp. (NYSE: AG) became a high-beta favorite, as its direct exposure to silver prices provided amplified returns during the metal's 128% climb.

Conversely, the surge has created significant headwinds for the "green" industrial sector. Tesla, Inc. (NASDAQ: TSLA) saw its automotive gross margins under heavy siege, falling to a low of 13.6% as the cost of silver per vehicle jumped from $25 to over $100. The solar industry faced even harsher realities; JinkoSolar Holding Co., Ltd. (NYSE: JKS) reported a net loss of $181.7 million in the first quarter, as the cost of silver paste—a critical component in photovoltaic cells—began to erode razor-thin margins. Even First Solar, Inc. (NASDAQ: FSLR), which uses less silver than its peers, was forced to cut its full-year guidance due to broader inflationary pressures and production inefficiencies exacerbated by the metal crisis.

A Fundamental Shift in Industrial and Regulatory Policy

The 2025 precious metals surge is more than just a price spike; it represents a fundamental shift in how the industry views these assets. Historically, silver has been viewed as "gold's understudy," but the 2025 rally has decoupled the two. Silver is now recognized as a critical industrial staple, essential for the global energy transition. This shift fits into a broader trend of "resource nationalism," where countries are increasingly viewing their mineral reserves as strategic assets rather than mere commodities. The supply deficit, estimated at nearly 240 million ounces this year, highlights the inelasticity of silver production, as 70% of the metal is mined as a by-product of other materials.

The regulatory implications of the Basel III update cannot be overstated. By treating gold as a risk-free asset, regulators have effectively "remonetized" gold within the modern banking system. This has created a permanent shift in demand that mirrors the historical precedents of the 1970s, but with the added complexity of a digital and green economy. Furthermore, the high prices have triggered a regulatory push for increased recycling and "thrifting" technologies. Governments are now considering subsidies for silver-recovery plants to ensure that the solar panels of today do not become the supply bottlenecks of tomorrow.

Historical comparisons to the 1980 silver peak or the 2011 rally are frequent, but analysts argue that 2025 is different. Unlike previous spikes driven by speculation, this rally is anchored by the "AI revolution" and the electrification of the global fleet. The demand for silver in server components and 48-volt EV architectures has created a structural floor that was absent in prior decades. This "valuation reset" suggests that the days of cheap silver may be permanently in the past, forcing a rethink of global supply chain strategies.

The Road Ahead: 2026 and Beyond

As we look toward 2026, the market faces several potential scenarios. In the short term, the high cost of metals will likely continue to drive "thrifting" innovations. We are already seeing solar manufacturers pivot toward silver-coated copper and copper-plated cells to reduce their reliance on pure silver. Companies that can successfully adapt to these new technologies will likely emerge as the next generation of industrial leaders. However, the transition will take time, and the supply-demand gap in silver is unlikely to close overnight, suggesting that prices will remain elevated for the foreseeable future.

Long-term, the strategic pivot toward 48-volt electrical architectures in vehicles, led by companies like Tesla and BMW, will be a critical space to watch. While these systems require less silver-intensive wiring, the overall growth in EV production may still keep total demand high. Investors should also keep a close eye on the "gold-to-silver ratio," which has compressed significantly in 2025. If silver continues to outperform, we may see a strategic rotation back into gold as a relative value play, or a continued surge in silver if the industrial deficit worsens.

Market opportunities will likely emerge in the recycling sector. Technologies like Jet Electrochemical Silver Extraction (JESE) are becoming commercially viable at $60+ silver, offering a way to recover precious metals from decommissioned solar panels. This "urban mining" could become a significant new supply source by the end of the decade, potentially dampening the volatility of the market.

Final Assessment: The Enduring Impact of the Revolution

The year 2025 will be remembered as the year the "Gold and Silver Revolution" changed the financial and industrial playbook. The key takeaway for investors is the dual nature of these metals; gold has solidified its role as the ultimate Tier 1 reserve asset, while silver has proven itself to be the indispensable backbone of the green and digital economy. The 128% rise in silver and 66% rise in gold are not just numbers on a screen, but reflections of a world grappling with geopolitical instability and a rapid technological transformation.

Moving forward, the market will likely remain in a state of "high-plateau" volatility. While the initial shock of the surge may subside, the structural drivers—trade wars, green tech demand, and central bank buying—remain firmly in place. Investors should watch for signs of "demand destruction" in the industrial sector, as well as any further regulatory changes that might affect central bank reserves.

Ultimately, the events of 2025 have proven that precious metals are far from "barbarous relics." They are, instead, the essential elements of the future. As the global economy continues to navigate the complexities of the 21st century, the silver lining of this year's rally is the clear signal it has sent: the era of abundant, low-cost resources is ending, and the era of strategic metal management has begun.

This content is intended for informational purposes only and is not financial advice.