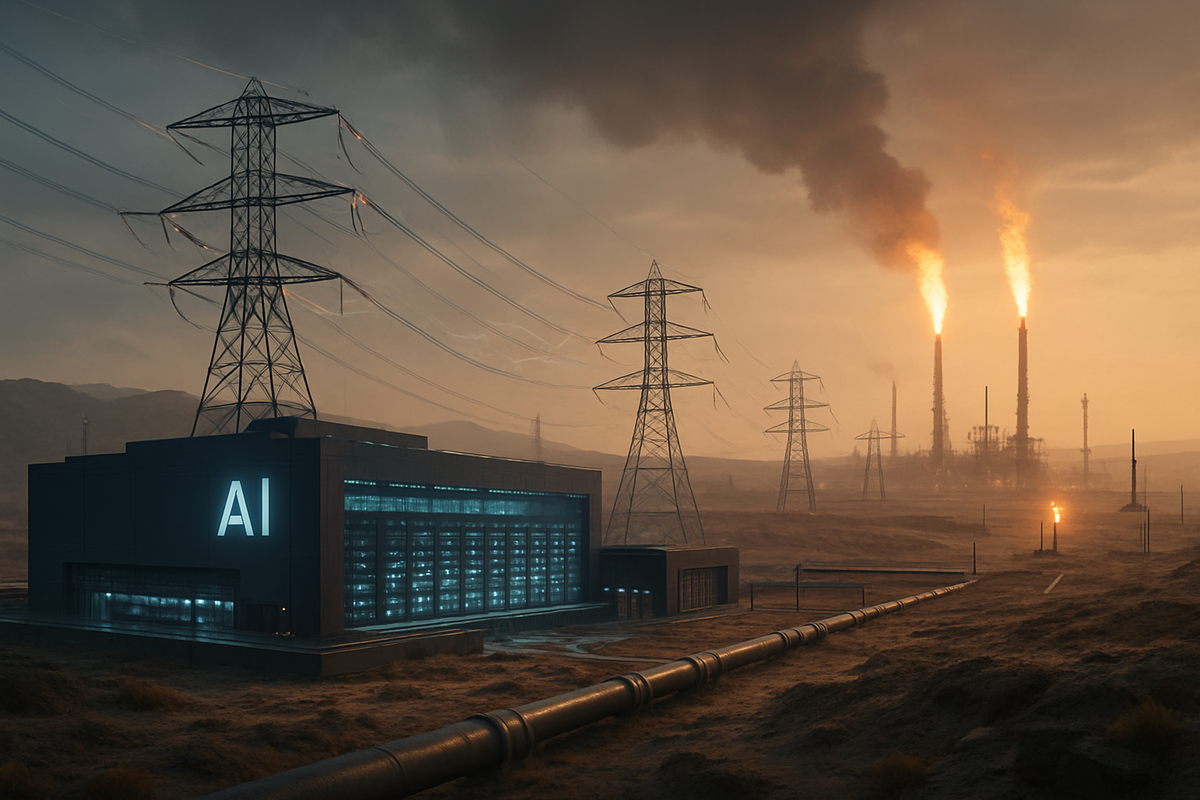

The burgeoning demand for Artificial Intelligence (AI) is pushing the U.S. energy infrastructure to its limits, creating a dual challenge of a strained national electricity grid and an exacerbated natural gas bottleneck in West Texas. AI data centers, rapidly proliferating across the nation, are consuming unprecedented amounts of power, threatening grid stability and driving up demand for reliable energy sources. This surge in consumption is not only accelerating the need for substantial upgrades to an aging electrical grid but is also highlighting critical deficiencies in the nation's energy supply chain, particularly in regions rich with natural gas.

The immediate implications are profound, ranging from potential electricity price hikes for consumers and businesses to a scramble for new power generation and transmission infrastructure. The urgency of these issues is forcing a re-evaluation of energy policy and investment strategies, as the nation grapples with how to fuel the future of AI without compromising grid reliability or environmental goals. The disorganized integration of these massive new loads is already being flagged as a significant reliability risk, particularly in high-growth areas like Texas.

The Unprecedented Energy Appetite of Artificial Intelligence

The rapid expansion of Artificial Intelligence (AI) is fundamentally reshaping the landscape of U.S. energy consumption, creating a “stunning and sudden paradigm shift” for the electric power sector. As of September 2025, AI data centers are on track to account for nearly half of all data center power consumption, projected to reach an astounding 23 gigawatts (GW)—a figure equivalent to twice the total energy consumption of the Netherlands. This trend is set to intensify, with the International Energy Agency (IEA) forecasting that global electricity demand from data centers will more than double by 2030, largely propelled by AI, reaching approximately 945 terawatt-hours (TWh), comparable to Japan's entire electricity consumption today.

In the U.S. specifically, data centers consumed about 4.4% of total electricity in 2023, approximately 176 TWh. However, projections for 2028 indicate a dramatic increase, with data centers expected to consume between 6.7% and 12% of all U.S. electricity, or 325 to 580 TWh. Some analyses suggest AI data centers alone could consume 22% of the electricity used by all U.S. households by the end of 2025. This surge is driven by power-intensive AI workloads that necessitate high-density racks and advanced cooling systems, increasing power density within data centers from 162 kilowatts (kW) per square foot to an estimated 176 kW per square foot by 2027. A single 100 MW data center can consume as much electricity as 75,000 homes, with its cooling systems drawing millions of gallons of water daily.

The timeline of this energy challenge underscores the urgency. For the past two decades, U.S. electricity demand remained relatively flat, but between 2020 and 2025, data center energy consumption soared by 80%. This is part of a broader trend where overall U.S. electricity demand is projected to grow by 9% by 2028 and 18% by 2033, fueled by data centers, AI, electrification, electric vehicles (EVs), and manufacturing expansion. The U.S. power grid, much of which is over 25 years old, is ill-equipped to handle this continuous, high-capacity power. Grid bottlenecks, limited transmission capacity, and extensive delays in connecting new power generation and loads are common, with major upgrades often taking a decade or more to implement. Supply chain constraints, such as 18-24 month lead times for critical power distribution equipment like transformers, further exacerbate these delays.

Key players driving this demand include hyperscalers like Google (NASDAQ: GOOGL), Microsoft (NASDAQ: MSFT), Amazon (NASDAQ: AMZN) (AWS), OpenAI, Meta (NASDAQ: META), Nvidia (NASDAQ: NVDA), and Oracle (NYSE: ORCL). These tech giants are not only consuming vast amounts of power but are also actively exploring and investing in their own energy solutions, including dedicated power plants and even nuclear options. For instance, the OpenAI and Oracle (NYSE: ORCL) “Stargate” project aims for 10 GW of capacity by 2028 through a $500 billion investment, with new complexes expected to generate over 5.5 GW of power capacity, more than double the electricity needed for San Francisco. On the supply side, U.S. utility companies such as Oncor Electric, PPL (NYSE: PPL), Evergy (NASDAQ: EVRG), Salt River Project, Dominion Energy (NYSE: D), and National Grid (NYSE: NGG) are on the front lines, grappling with unprecedented power capacity requests that sometimes surpass their entire existing generation capacity. The U.S. Department of Energy (DOE) launched its “Speed to Power” initiative in September 2025 to accelerate large-scale grid infrastructure projects, acknowledging the national significance of the issue. Initial market reactions reflect widespread concern, with utilities facing "unprecedented challenges" in forecasting demand and financial concerns about who will bear the billions in infrastructure investment costs, potentially leading to higher residential electricity prices. This has prompted hyperscalers to seek dedicated, reliable power sources, including their own small modular reactors (SMRs) or partnerships to restart nuclear plants, like Microsoft's (NASDAQ: MSFT) collaboration with Constellation Energy (NASDAQ: CEG) for Three Mile Island.

Corporate Fortunes in the AI Energy Race

The escalating energy demands of AI data centers are creating a distinct cleavage in the financial markets, carving out clear winners and losers across the energy, utility, and technology sectors. Companies that are agile in adapting to this new energy paradigm, or those that provide critical solutions, are poised for significant gains, while others may face substantial headwinds.

In the energy sector, natural gas producers, midstream companies, and power generation equipment manufacturers are experiencing a surge in demand. EQT Corporation (NYSE: EQT), as the largest natural gas producer in the U.S., is a prime beneficiary. Its focus on certified low-emissions gas aligns with hyperscalers' needs for reliable, dispatchable power, potentially securing long-term supply contracts. Similarly, GE Vernova (NYSE: GEV), a dominant manufacturer of natural gas turbines, transformers, and smart grid software, is seeing increased deployment of its equipment as new power infrastructure is built to support AI data centers. Its strategic role in both traditional generation and grid modernization makes it a critical enabler. Integrated energy giants like Exxon Mobil (NYSE: XOM) and Chevron (NYSE: CVX) are also strategically investing in natural gas-fired power plants, often with carbon capture technology, to directly serve data centers, creating new revenue streams and diversifying their operations beyond traditional oil and gas extraction. Pipeline and midstream companies, such as Williams Companies (NYSE: WMB), are crucial for alleviating bottlenecks and ensuring a steady fuel supply, particularly in gas-rich regions like West Texas, positioning them for increased throughput and revenue. Conversely, smaller, unintegrated natural gas producers in West Texas, lacking adequate infrastructure to convert gas into electricity or transmit it efficiently, risk losing market share and may find their abundant reserves a "money pit" due to lost opportunities and discounted sales.

The utilities sector is experiencing a transformative period. Constellation Energy (NASDAQ: CEG), the largest operator of nuclear reactors in the U.S., is a standout winner. Its nuclear power offers 24/7, carbon-free generation, making it a preferred partner for tech giants like Microsoft (NASDAQ: MSFT) and Meta (NASDAQ: META), leading to significant long-term power purchase agreements and the potential restart of facilities like the Three Mile Island nuclear plant. Dominion Energy (NYSE: D), strategically located in Virginia's "Data Center Alley," is investing heavily in generation capacity and grid modernization, including exploring Small Modular Reactor (SMR) development with partners like Amazon Web Services (NASDAQ: AMZN). Entergy Corporation (NYSE: ETR) is building new natural gas plants to serve large data center campuses, demonstrating direct financial benefits from AI-driven load growth. DTE Energy (NYSE: DTE) is in advanced discussions for multiple gigawatts of new load from hyperscalers, leveraging its diverse portfolio including nuclear and renewables. Large utilities like American Electric Power (NASDAQ: AEP) and NextEra Energy (NYSE: NEE), with their scale and generation capabilities, are also well-positioned. Companies like PPL Corp (NYSE: PPL) are forming joint ventures to develop dedicated gas-fired power plants for data centers. Equipment manufacturers such as Eaton (NYSE: ETN) and Schneider Electric (OTCMKTS: SBGSF) are benefiting from the increased demand for essential electrical components needed for grid and data center scaling. However, utilities with limited or slow-to-adapt infrastructure in high-demand regions face potential losses. They risk operational challenges, delayed revenue from new data center projects, or increased costs to upgrade aging systems, potentially leading to lower earnings or regulatory pushback on rate increases.

Within the AI/Tech Infrastructure realm, hyperscale cloud providers and data center developers like Amazon (NASDAQ: AMZN) (AWS), Alphabet (NASDAQ: GOOGL) (Google Cloud), Microsoft (NASDAQ: MSFT), Meta Platforms (NASDAQ: META), and Oracle (NYSE: ORCL) are making massive investments in securing their own power sources, including nuclear and large-scale renewables. While energy costs are significant, these strategic investments safeguard their core AI and cloud businesses, ensuring uninterrupted growth. Developers of Nuclear Small Modular Reactors (SMRs), such as NuScale Power (NYSE: SMR), are poised for significant growth as tech giants plan to utilize SMRs for reliable, carbon-free data center power. Energy storage solution providers like Fluence Energy (NASDAQ: FLNC), Bloom Energy (NYSE: BE), and Tesla (NASDAQ: TSLA) (Tesla Energy) are critical for managing peak loads, providing backup power, and integrating intermittent renewables, ensuring grid stability for AI operations. Innovative companies like Crusoe, which builds and operates AI data centers by directly sourcing energy from novel sources including natural gas with carbon capture, offer cost efficiencies and competitive advantages. Finally, semiconductor manufacturers focused on energy efficiency, such as TSMC (NYSE: TSM), NVIDIA (NASDAQ: NVDA), and AMD (NASDAQ: AMD), will gain a competitive edge. While AI chips are power-hungry, the immense demand drives revenue, but the focus on "performance per watt" will favor those delivering powerful yet efficient designs. Conversely, data center operators heavily reliant on traditional grid expansion in constrained regions, without a robust energy strategy, risk significant delays and stranded assets. Similarly, semiconductor manufacturers that fail to prioritize energy efficiency may find their products less appealing as energy costs become a dominant factor for data center operators.

AI's Energy Footprint: A Catalyst for Systemic Change

The U.S. electricity challenge and the West Texas gas bottleneck, driven by the insatiable energy demands of AI data centers, represent more than just immediate infrastructure hurdles; they are a catalyst for systemic change across the energy and technology landscapes. As of September 25, 2025, this phenomenon is profoundly influencing broader industry trends, creating significant ripple effects, necessitating urgent policy responses, and drawing comparisons to historical periods of rapid technological transformation.

The escalating energy consumption of AI is pushing U.S. power demand to unprecedented levels. The U.S. Energy Information Administration (EIA) projects consumption to reach 4,179 billion kWh in 2025 and 4,239 billion kWh in 2026, surpassing previous records. By 2030, global data center electricity demand is expected to more than double, with AI alone quadrupling demand from dedicated AI-optimized facilities. In the U.S., AI data centers could account for nearly half of the projected electricity demand growth by 2030, potentially increasing their share of total U.S. electricity use from approximately 4.4% today to as much as 12% by 2028. This rapid and concentrated energy draw poses significant stability concerns for the largely aging U.S. power grid, which was not designed for such exponential growth. The West Texas gas bottleneck, characterized by abundant natural gas in the Permian Basin but insufficient infrastructure to convert and transmit it as electricity, further exacerbates this issue, leading to instances of negative gas prices despite surging demand for power.

These dynamics are accelerating several key industry trends. There is an urgent need for massive investments in new power generation and transmission infrastructure, underscored by the U.S. Department of Energy's "Speed to Power" initiative aimed at accelerating large-scale projects. The energy mix is also evolving; while natural gas remains crucial, there's a growing emphasis on renewables and a diversified portfolio, including existing coal and nuclear plants, to ensure grid stability. The intense power density of AI workloads is driving innovation in energy efficiency and advanced cooling technologies, with liquid cooling gaining prominence and AI-powered energy management systems optimizing power usage. Furthermore, the search for reliable and affordable power is causing a geographical shift in data center locations, moving beyond traditional hubs to secondary and rural markets with better energy access. Data center operators are also increasingly exploring on-site generation and integrating Battery Energy Storage Systems (BESS) for enhanced resilience.

The ripple effects are far-reaching. The surging demand could lead to higher electricity costs for residential consumers and other industries if grid expansion is not managed effectively. Access to reliable and affordable power is becoming a critical competitive differentiator for data centers, potentially influencing where future investments are made globally. This situation presents immense opportunities for energy infrastructure providers, power generation companies, and technology firms specializing in grid modernization, energy storage, and efficient cooling. However, traditional utilities face immense pressure to upgrade aging infrastructure, often encountering long lead times due to complex permitting processes. Beyond energy, the substantial water consumption of data centers, particularly for cooling, raises significant environmental concerns and potential conflicts over water resources in arid regions.

Both federal and state governments are actively engaged in addressing these challenges. The Trump administration has declared the situation a national energy emergency, with Executive Orders in early 2025 emphasizing grid reliability and security, and streamlining permitting for data center infrastructure. The "Speed to Power" initiative aims to reduce regulatory bottlenecks and expedite approvals for critical energy projects. States are competing to attract data center investments through incentives, increasingly tying them to infrastructure readiness and renewable energy use. There's also a growing call for greater transparency from tech companies and utilities regarding their energy and water usage to better inform policy decisions.

Historically, the current AI-driven energy demand draws parallels to the Dot-Com Boom and the early internet's demand for data centers, and more recently, the energy-intensive cryptocurrency mining boom. However, the sheer scale, speed, and concentrated nature of AI's energy requirements make this situation unique. AI data centers create large, localized clusters of 24/7 power consumption with significantly higher energy usage per square foot. The specialized hardware for AI processing is inherently energy-intensive. This demand is so profound that by 2030, the U.S. economy is projected to consume more electricity for AI data processing than for manufacturing all energy-intensive goods combined, such as steel, cement, and chemicals. This marks a transformative moment, akin to past industrial revolutions, necessitating a rapid and extensive overhaul of energy infrastructure.

Navigating the Future: Pathways for AI and Energy

The path forward for the U.S. electricity challenge and the West Texas gas bottleneck, driven by the relentless energy demands of AI data centers, requires immediate and sustained strategic pivots from both industry and government. As of September 2025, the future outlook presents a complex interplay of short-term fixes, long-term visions, significant market opportunities, and formidable challenges.

In the short-term (next 1-3 years), the focus will be on maximizing existing grid capacity and rapidly deploying flexible generation and storage solutions. Utilities are prioritizing high-probability projects, particularly in battery energy storage and natural gas peaker plants, to offer near-term capacity gains. Streamlining the interconnection process for new power projects is crucial to reduce backlogs. Natural gas will continue to serve as a critical bridge fuel, leveraging its abundant supply and flexible generation capabilities to meet surging demand. Data centers themselves will implement demand-side management strategies, such as power capping on processors and optimizing cooling systems (which can account for up to 40% of their electricity demand), to reduce immediate load. Tech giants are increasingly pursuing direct power purchase agreements, sometimes bypassing traditional utility structures to secure dedicated power.

Looking long-term (beyond 3 years), a fundamental transformation of the energy infrastructure is imperative. This includes significant upgrades to transmission infrastructure, projects that typically require 5-10 years for permitting and construction. Goldman Sachs estimates approximately $720 billion in grid spending through 2030, with U.S. electric utilities expected to invest over $1.1 trillion between 2025-2029. Utilities will need diversified energy portfolios that balance renewables (wind and solar with long-duration storage) and natural gas. Nuclear power, especially Small Modular Reactors (SMRs), is poised for a renaissance as a reliable, low-carbon baseload power source, with tech companies like Microsoft (NASDAQ: MSFT) actively exploring its potential. Widespread deployment of advanced energy storage technologies will be crucial to manage renewable intermittency, and geothermal energy offers potential for both direct data center cooling and baseload electricity. Ironically, AI itself is expected to play a critical role in optimizing grid operations, predicting problems, integrating renewables, and improving overall efficiency.

Strategic adaptations are required across the board. Industry (Data Centers & Tech Companies) must refine their siting strategies, prioritizing locations with robust power infrastructure, available land, and streamlined permitting. Investing in energy efficiency innovations, such as advanced chips, liquid cooling technologies, and rethinking AI model training, can significantly reduce energy consumption per computation. Exploring on-site generation, including small-scale natural gas plants or microreactors, offers energy independence. Furthermore, data centers will increasingly need to actively share in the costs of new substations, transmission lines, or water systems required by their clusters. For Government (Federal, State, Local), a national coordination strategy is essential, moving beyond piecemeal agreements to a unified framework for grid modernization and clean energy incentives. Streamlining the permitting process for new generation and transmission projects is paramount. Providing incentives for infrastructure upgrades and clean energy deployment, potentially linking tax benefits to data center efficiency standards, will be crucial. Developing "regulatory sandboxes" for AI applications in grid management and revising outdated integrated resource plans to accurately account for exponential AI demand are also critical steps.

The market opportunities emerging from this challenge are substantial. An infrastructure investment boom is imminent, creating significant opportunities for grid operators, energy developers, gas suppliers, and infrastructure funds. New energy technologies, including long-duration energy storage, advanced nuclear (SMRs), geothermal systems, and carbon capture technologies, will see accelerated market growth. Companies offering innovative cooling solutions, more efficient hardware, and AI-driven energy management systems will find a booming market. Conversely, the challenges are formidable. Grid constraints and reliability issues, exacerbated by interconnection queues that have increased by 700% in some regions, pose a serious risk. The scale of required investment is enormous, demanding hundreds of billions to trillions of dollars, coupled with persistent regulatory hurdles and permitting delays. Environmental concerns, particularly regarding carbon emissions and water consumption, will continue to be prominent.

Considering potential scenarios, a best-case outcome involves rapid and coordinated public and private investment leading to aggressive grid modernization and expansion. This would integrate a diversified mix of clean energy sources alongside highly efficient AI data centers, with streamlined permitting and AI-optimized grid operations. The U.S. would maintain its AI leadership while achieving decarbonization goals and managing energy costs. A worst-case scenario would see insufficient investment and persistent regulatory hurdles leading to chronic grid instability, frequent power outages, and escalating electricity costs. Data center growth would be constrained, potentially forcing operations abroad and eroding U.S. competitiveness in AI, while increased reliance on fossil fuels would derail climate targets. The probable-case scenario is a mixed bag: regional disparities in energy supply and grid readiness will become more pronounced. Natural gas will continue as a significant bridge fuel, especially in gas-rich areas, while efforts to scale renewables, storage, and nuclear accelerate but face delays. Data centers will become more proactive in on-site generation and efficiency, but grid constraints will remain a persistent issue, causing some project delays. This involves a continuous balancing act between meeting surging AI demand and achieving sustainability goals, with innovation in energy technologies and grid management playing a crucial role in navigating these tensions. The economic boost from infrastructure investment will be realized, but not without considerable cost and effort.

The Power Paradox: Fueling AI's Future

The burgeoning demand for Artificial Intelligence (AI) has thrust the U.S. energy infrastructure into a critical juncture, revealing a profound "power paradox" where the engine of future innovation is simultaneously straining the very systems designed to support it. As of September 25, 2025, the U.S. electricity challenge and the West Texas gas bottleneck are not merely isolated issues but central themes defining the nation's energy and technological trajectory.

Key Takeaways: The most salient point is the soaring AI energy demand, with data centers projected to account for a rapidly increasing share of U.S. electricity consumption, potentially reaching 8.6% of all U.S. electricity demand by 2035, and even higher in some forecasts. This exponential growth means the U.S. economy is expected to consume more electricity for data processing in 2030 than for manufacturing all energy-intensive goods combined. This unprecedented load is severely stressing the U.S. electricity grid, much of which is decades old and ill-equipped for such high-density power requirements, leading to concerns about stability and rising costs. Compounding this is the West Texas gas bottleneck, where abundant natural gas resources are hindered by inadequate infrastructure for conversion and transmission, preventing this vital fuel from efficiently reaching power-hungry data centers. The national urgency of this situation is underscored by the U.S. administration reportedly declaring a national energy emergency in January 2025 to fast-track infrastructure development.

Market Assessment Moving Forward: The market is at a critical "build-out or bottleneck" crossroads, necessitating massive capital expenditure across both technology and energy sectors. Hyperscalers are investing hundreds of billions in AI data centers and their dedicated power systems. Simultaneously, electric and gas utilities are forecasting record increases in capital expenditures to upgrade and expand the grid.

Solutions are emerging across several fronts:

- Diversified Power Generation: A mix of energy sources will be crucial, with renewables (solar, wind) and natural gas expected to take the lead due to cost-competitiveness and availability. There's also a focus on integrating long-duration storage and prioritizing flexible generation to ensure reliability.

- Efficiency Innovations: Technological advancements in AI data center design, chip efficiency, and cooling systems (e.g., liquid cooling, immersion cooling) are vital to reduce power demand. AI itself is being leveraged to optimize cooling and overall data center efficiency.

- On-Site Generation and Microgrids: To circumvent grid limitations and reduce dependence on aging infrastructure, many facilities are investing in on-site power generation, including solar farms, wind turbines, and natural gas generators. Co-location of data centers with existing or new power plants is also gaining traction.

- Grid Modernization and Transmission Expansion: Significant transmission upgrades and new pipelines are needed to deliver power where it's needed most. Streamlining permitting and regulatory processes for these projects is critical. The Electric Reliability Council of Texas (ERCOT), for instance, estimates a roughly $30 billion investment is needed to lay thousands of miles of long-distance transmission lines to meet growing demand.

Final Thoughts on Significance and Lasting Impact: The AI energy demand is not merely a temporary spike but a fundamental reshaping of the energy landscape. AI has transitioned from being purely a digital or software concern to a physical infrastructure challenge, impacting everything from power grids to urban planning and resource allocation. The trajectory of AI growth is now intrinsically linked to the ability to generate, transmit, and efficiently utilize electricity. The energy sector's evolution will determine the pace and scale of AI's future development. This dynamic signals a long-term shift where access to reliable, abundant, and increasingly sustainable power will be the new competitive advantage in the tech world. The race to build "AI factories" is now a race to secure power.

Advice for Investors in Coming Months: Investors should closely monitor developments in several key areas over the coming months:

- Energy Infrastructure Companies: Focus on utilities and companies involved in power generation (especially those with diversified portfolios including natural gas and renewables), transmission, and distribution. Companies specializing in grid upgrades, such as manufacturers of transformers, circuit breakers, and transmission lines, will see sustained demand.

- Data Center Co-location and On-site Power Solutions: Companies that offer integrated power solutions, including on-site generation, microgrids, and advanced energy storage systems, are well-positioned. Look for partnerships between energy providers and data center operators.

- Efficiency Technologies: Investigate companies innovating in data center cooling technologies (e.g., liquid cooling providers), power conversion, and more energy-efficient chip and server designs. These innovations will be critical for managing the exponential energy growth.

- Natural Gas Infrastructure (especially in Texas): Given the West Texas bottleneck, companies involved in building new natural gas pipelines and gas-fired power plants in regions with high data center growth, particularly Texas, could see significant opportunities.

- Policy and Regulatory Developments: Keep an eye on government policies, incentives, and regulatory changes aimed at accelerating energy infrastructure development, streamlining permitting, and promoting sustainable energy solutions. These will significantly influence where and how quickly new capacity comes online.

- "AI for AI" Solutions: Companies that leverage AI to optimize energy management, predict demand, and enhance grid stability will also be valuable.

- Real Estate with Power Access: Data center developers and real estate companies specializing in sites with approved access to large amounts of power will become increasingly valuable as interconnection queues grow in most markets, with wait times now around four years.

The confluence of AI innovation and energy infrastructure limitations presents both significant challenges and substantial investment opportunities. The next phase of the digital economy will be shaped as much by who powers it as by who programs it.

This content is intended for informational purposes only and is not financial advice