Wall Street's once-fervent optimism for a rapid succession of Federal Reserve interest rate cuts has hit a significant snag in late September 2025. Following the Fed's initial 25-basis-point rate reduction on September 17, a blend of fresh, nuanced economic data and cautious pronouncements from central bank officials has compelled investors to recalibrate their expectations. This reassessment paints a picture of a Federal Reserve navigating a challenging path, balancing the risks of a softening labor market against stubbornly persistent inflation, leaving markets in a state of tempered anticipation.

The immediate implications are palpable: a market grappling with uncertainty about the pace and extent of future monetary easing. What was once seen as a clear path to lower borrowing costs now appears fraught with data dependency and internal divisions within the Fed, prompting a cautious stance among investors and analysts alike.

The Fed's First Move and the Shifting Economic Landscape

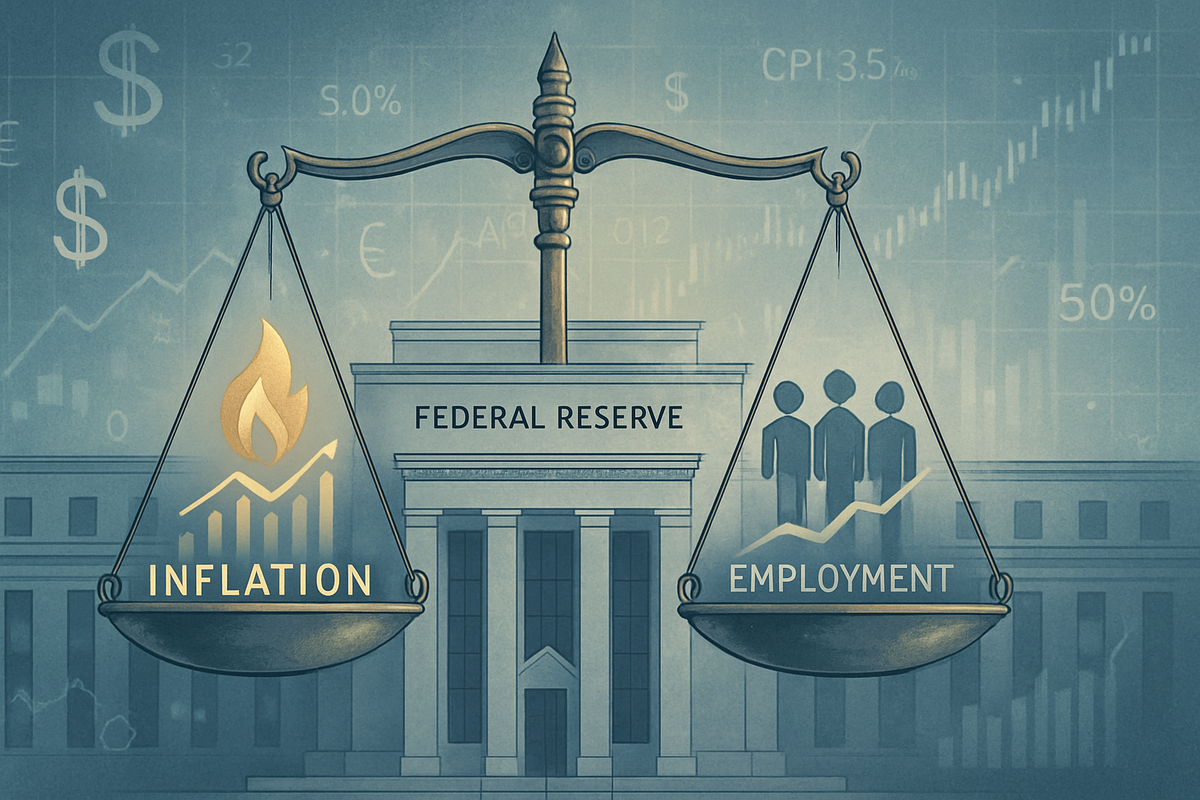

The Federal Reserve's Federal Open Market Committee (FOMC) delivered its first interest rate cut of the year on September 17, 2025, lowering the benchmark federal funds rate by 25 basis points to a target range of 4.0%-4.25%. This move, largely anticipated after signals from Fed Chair Jerome Powell in August, was primarily justified by growing concerns over a weakening labor market and an uptick in unemployment, which presented palpable downside risks to the employment mandate.

However, the celebratory mood was short-lived as subsequent economic indicators painted a complex picture. The U.S. nonfarm payrolls for August 2025 showed a meager increase of just 22,000 jobs, drastically missing market forecasts and marking a sharp decline from the 79,000 jobs added in July. Compounding this, the unemployment rate climbed to 4.3% in August, reaching its highest level in nearly four years. A preliminary benchmark revision in early September further dampened spirits, suggesting that hiring for the 12 months ending March 2025 was approximately 800,000 jobs lower than initially reported, revising average monthly job growth in 2024 down significantly. Sectors such as manufacturing and the federal government notably experienced job losses.

Simultaneously, the ghost of inflation continued to haunt the economic outlook. Despite the evident labor market concerns, inflation remained stubbornly above the Fed's 2% target. The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.4% in August on a seasonally adjusted basis, with the all-items index rising 2.9% year-over-year. Core CPI, which strips out volatile food and energy components, accelerated to 3.1% year-over-year in August, signaling underlying price pressures. Average hourly earnings continued their ascent, up 3.7% year-over-year, indicating ongoing wage inflation. Fed officials also acknowledged that the full impact of recently implemented tariffs in early August had yet to be fully reflected in the inflation data, suggesting potential for further price increases.

Comments from Federal Reserve officials post-cut further underscored the cautious approach. Chair Jerome Powell characterized the September cut as a "risk-management cut," aimed at mitigating growing downside risks to employment, but warned against cutting "too aggressively," which could jeopardize the ongoing fight against inflation. Chicago Fed President Austan Goolsbee expressed unease with rapid rate cuts, citing the risk of "stagflation" – a grim combination of stagnant growth and high inflation – given that inflation has exceeded the target for over four years. While Fed Governor Stephen Miran dissented, advocating for a more aggressive 50-basis-point reduction, and Governor Michelle Bowman reportedly favored quicker cuts, the overall tone from the FOMC, particularly the median "dot plot" projection of only two more 25-basis-point cuts by year-end 2025, signaled a deliberate and data-dependent path forward.

Initial market reactions to the September 17th cut were broadly positive, with major stock indices like the S&P 500 (NYSEARCA: SPY) and Dow Jones Industrial Average (NYSEARCA: DIA) seeing gains. However, this optimism quickly moderated. The Nasdaq Composite (NASDAQ: QQQ) initially declined, reflecting sensitivities in technology and growth sectors. In the bond market, Treasury yields, including the two-year and ten-year, nudged higher, indicating a reassessment of the Fed's future trajectory. As of September 25, 2025, Wall Street was showing signs of tempered enthusiasm, with major indexes poised for lower opens, as new economic data and cautious Fed remarks led investors to dial back expectations for a swift series of further cuts.

Navigating the Shifting Tides: Potential Winners and Losers

The recalibration of rate cut expectations has significant implications for various sectors and individual companies. A "higher-for-longer" interest rate environment, or one where cuts are slow and deliberate, will create both opportunities and headwinds across the market.

Potential Beneficiaries (or those less impacted by slower cuts): Companies in less interest-rate-sensitive sectors or those with strong balance sheets may fare better. Financial institutions like regional banks, while potentially seeing some compression in net interest margins if cuts are too slow in a weakening economy, could also benefit from a more stable, albeit higher, rate environment that allows for predictable lending. Defensive sectors such as utilities and certain consumer staples (e.g., Procter & Gamble (NYSE: PG), Coca-Cola (NYSE: KO)) tend to be more resilient during periods of economic uncertainty. Real estate investment trusts (REITs) like Prologis (NYSE: PLG) or Simon Property Group (NYSE: SPG), which are highly sensitive to borrowing costs, might still see some benefit from the initial cut, but tempered expectations mean their recovery might be slower than previously hoped. Companies with strong cash flows and less reliance on debt for growth will also be in a more advantageous position.

Potential Adversaries (or those more impacted by slower cuts): Growth stocks, particularly in the technology sector (e.g., Apple (NASDAQ: AAPL), Microsoft (NASDAQ: MSFT), Amazon (NASDAQ: AMZN)), which derive much of their valuation from future earnings, can be negatively impacted by higher discount rates. Slower rate cuts mean their future profits are worth less in present value terms. Highly leveraged companies across various sectors will face increased debt servicing costs if rates remain elevated, potentially squeezing profitability and limiting expansion. The housing market, while receiving a slight boost from the initial cut, could see its recovery hampered if mortgage rates don't fall as rapidly as once envisioned. Companies heavily reliant on discretionary consumer spending may also struggle if a slowing economy and persistent inflation erode purchasing power.

Wider Significance: A New Era of Monetary Policy

This reassessment of rate cut expectations marks a crucial juncture in the Federal Reserve's post-pandemic monetary policy. It underscores a shift from an era focused on quickly stimulating growth to one meticulously balancing inflation control with employment stability. This delicate dance has broader implications for industry trends, global markets, and regulatory considerations.

The "higher-for-longer" narrative, even if tempered by some cuts, suggests a continued emphasis on profitability and efficiency over aggressive, debt-fueled growth. This could lead to a slowdown in mergers and acquisitions (M&A) activity as financing becomes more expensive, and a greater scrutiny of corporate investment decisions. Companies may prioritize deleveraging and cash flow generation over expansion, impacting capital expenditure trends across industries. Globally, the Fed's cautious stance could lead to a stronger U.S. dollar, potentially pressuring emerging market economies that hold dollar-denominated debt or rely on exports to the U.S. The spectre of "stagflation," explicitly mentioned by Fed officials, is a concerning historical precedent, harkening back to the 1970s and early 1980s, where policymakers grappled with both high inflation and economic stagnation. This historical parallel highlights the complexity of the current economic environment and the potential for a prolonged period of economic malaise if the Fed misjudges its next steps. Regulatory bodies may also face renewed pressure to address supply-side constraints and structural inflation drivers if monetary policy alone proves insufficient.

What Comes Next: A Data-Dependent Path Forward

The path ahead for the Federal Reserve and the financial markets is likely to be characterized by heightened data dependency and continued volatility. In the short term, investors will be glued to every upcoming economic report, particularly inflation metrics (CPI, PPI) and labor market data (nonfarm payrolls, jobless claims). Any deviation from expectations in these reports could trigger significant market movements, as the Fed's next moves are now explicitly tied to incoming information.

Longer-term possibilities include a protracted period of gradual easing, assuming inflation continues its slow descent while the labor market softens further. This scenario, often referred to as a "soft landing," would see the economy avoid a deep recession while inflation returns to target. However, the risk of a "hard landing" or even "stagflation" remains if inflation proves more entrenched or the labor market deteriorates rapidly. Companies will need to strategically pivot, adjusting their capital allocation, debt management, and operational efficiencies to thrive in an environment where the cost of capital remains elevated compared to the ultra-low rates of the past decade. Market opportunities may emerge in defensive sectors, dividend-paying stocks, and companies with strong pricing power. Conversely, highly leveraged businesses and those reliant on aggressive consumer spending could face significant challenges. Investors should prepare for a landscape where agility and fundamental strength are paramount.

Wrap-Up: Navigating Uncertainty in a Transformed Market

The reassessment of Federal Reserve rate cut hopes marks a significant pivot in the financial markets. The key takeaway is a shift from optimistic anticipation of rapid easing to a more realistic, cautious outlook defined by data dependency and the Fed's challenging dual mandate. The September 25, 2025, market sentiment reflects this new reality: a market moving forward with tempered optimism, keenly aware of the complex interplay between a softening labor market and persistent inflationary pressures.

The lasting impact of this period will likely be a recalibration of investor expectations regarding monetary policy, fostering an environment where economic fundamentals and corporate resilience are valued above speculative growth. Investors should closely monitor upcoming inflation and employment data, as well as the nuanced communications from Federal Reserve officials. The market moving forward will reward adaptability and a deep understanding of economic cycles, rather than a reliance on perpetual monetary accommodation. This is not merely a temporary blip but potentially the beginning of a new chapter in economic policy, demanding a more discerning and strategic approach from all market participants.

This content is intended for informational purposes only and is not financial advice