Pest control company Rollins (NYSE: ROL) met Wall Streets revenue expectations in Q3 CY2025, with sales up 12% year on year to $1.03 billion. Its non-GAAP profit of $0.35 per share was 6.4% above analysts’ consensus estimates.

Is now the time to buy Rollins? Find out by accessing our full research report, it’s free for active Edge members.

Rollins (ROL) Q3 CY2025 Highlights:

- Revenue: $1.03 billion vs analyst estimates of $1.02 billion (12% year-on-year growth, in line)

- Adjusted EPS: $0.35 vs analyst estimates of $0.33 (6.4% beat)

- Adjusted EBITDA: $258.3 million vs analyst estimates of $249.8 million (25.2% margin, 3.4% beat)

- Operating Margin: 21.9%, in line with the same quarter last year

- Free Cash Flow Margin: 17.8%, up from 15.2% in the same quarter last year

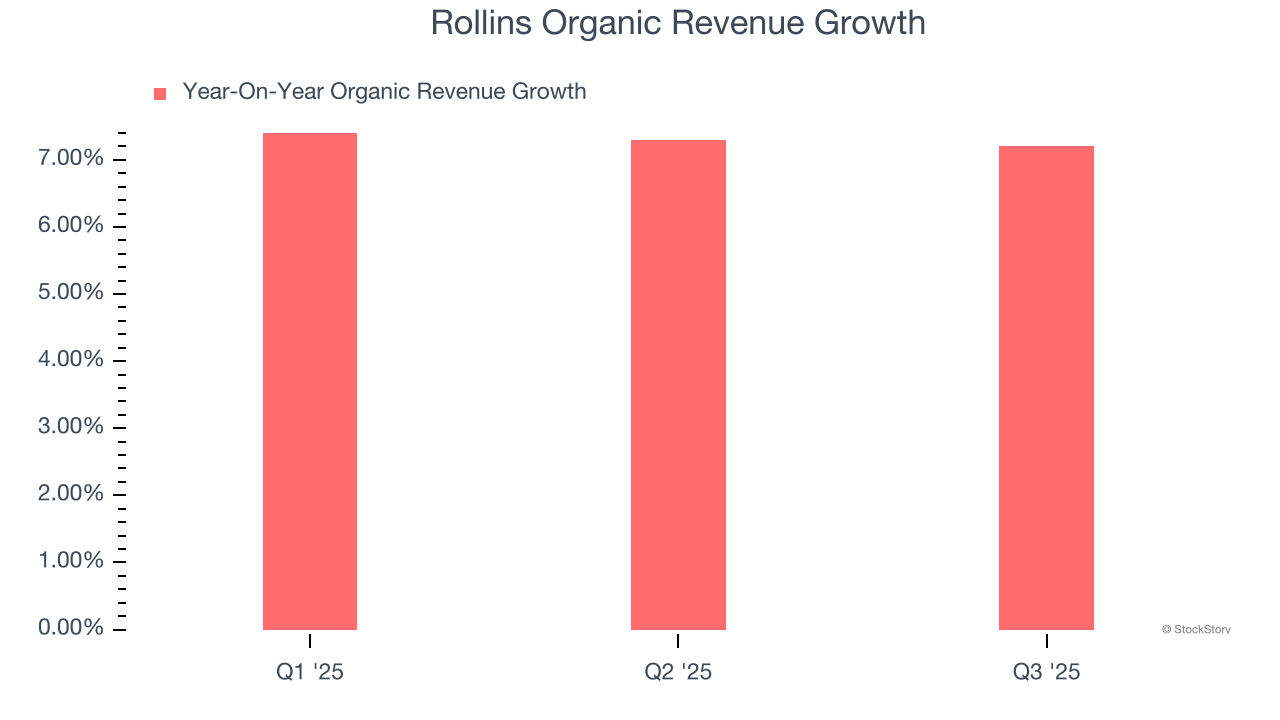

- Organic Revenue rose 7.2% year on year vs analyst estimates of 7.4% growth (18 basis point miss)

- Market Capitalization: $27.16 billion

"We delivered a strong third quarter with record revenue and an improving margin profile, a reflection of an ongoing commitment to execution by our teammates," said Jerry Gahlhoff, Jr., President and CEO.

Company Overview

Operating under multiple brands like Orkin and HomeTeam Pest Defense, Rollins (NYSE: ROL) provides pest and wildlife control services to residential and commercial customers.

Revenue Growth

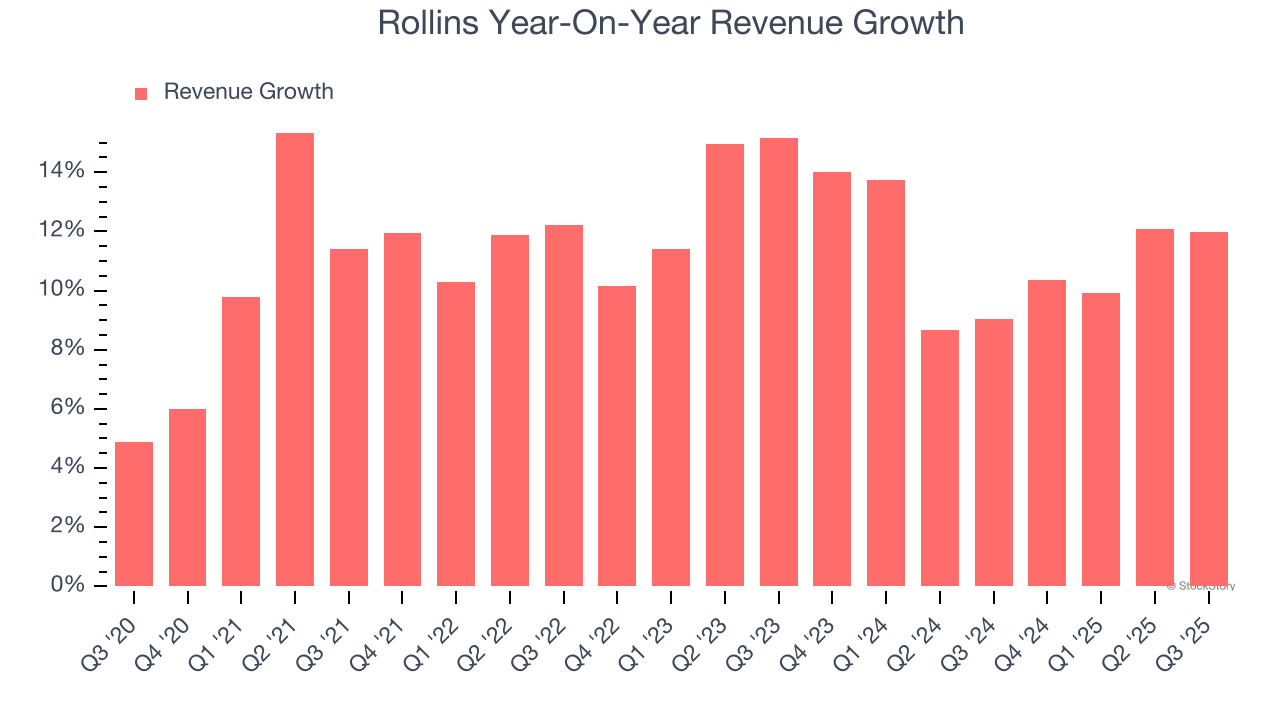

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Rollins’s 11.5% annualized revenue growth over the last five years was impressive. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Rollins’s annualized revenue growth of 11.1% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Rollins’s organic revenue averaged 7.3% year-on-year growth. Because this number is lower than its two-year revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

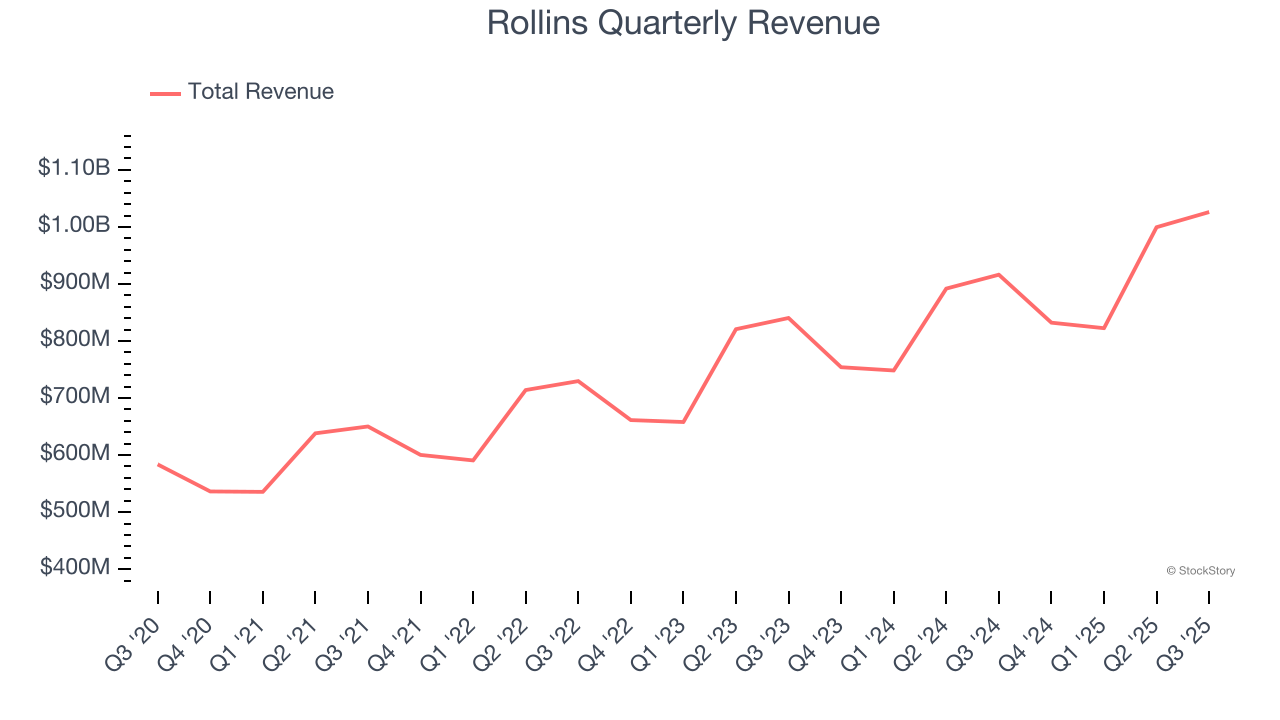

This quarter, Rollins’s year-on-year revenue growth was 12%, and its $1.03 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 9.3% over the next 12 months, a slight deceleration versus the last two years. Despite the slowdown, this projection is noteworthy and indicates the market is forecasting success for its products and services.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

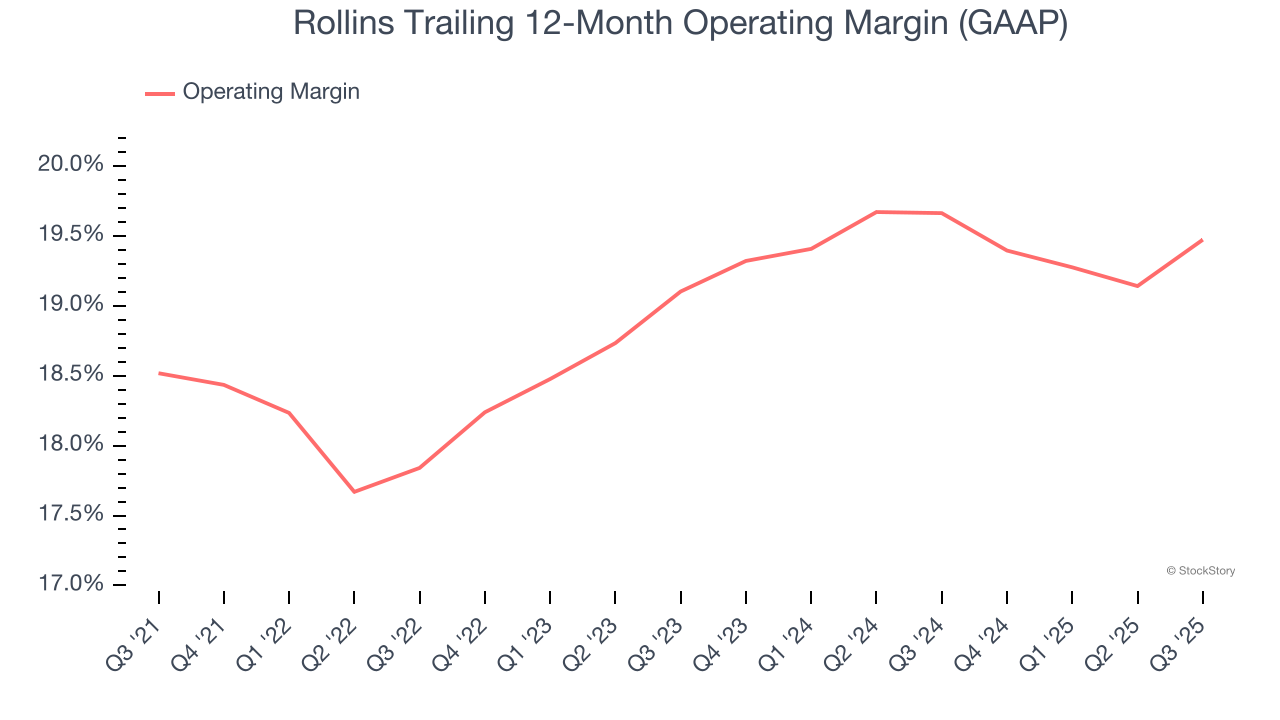

Rollins’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 19% over the last five years. This profitability was elite for an industrials business thanks to its efficient cost structure and economies of scale. This is seen in its fast historical revenue growth and healthy gross margin, which is why we look at all three data points together.

Looking at the trend in its profitability, Rollins’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. We like to see margin expansion, but Rollins’s performance still shows it’s one of the better Facility Services companies as most peers saw their margins plummet.

In Q3, Rollins generated an operating margin profit margin of 21.9%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

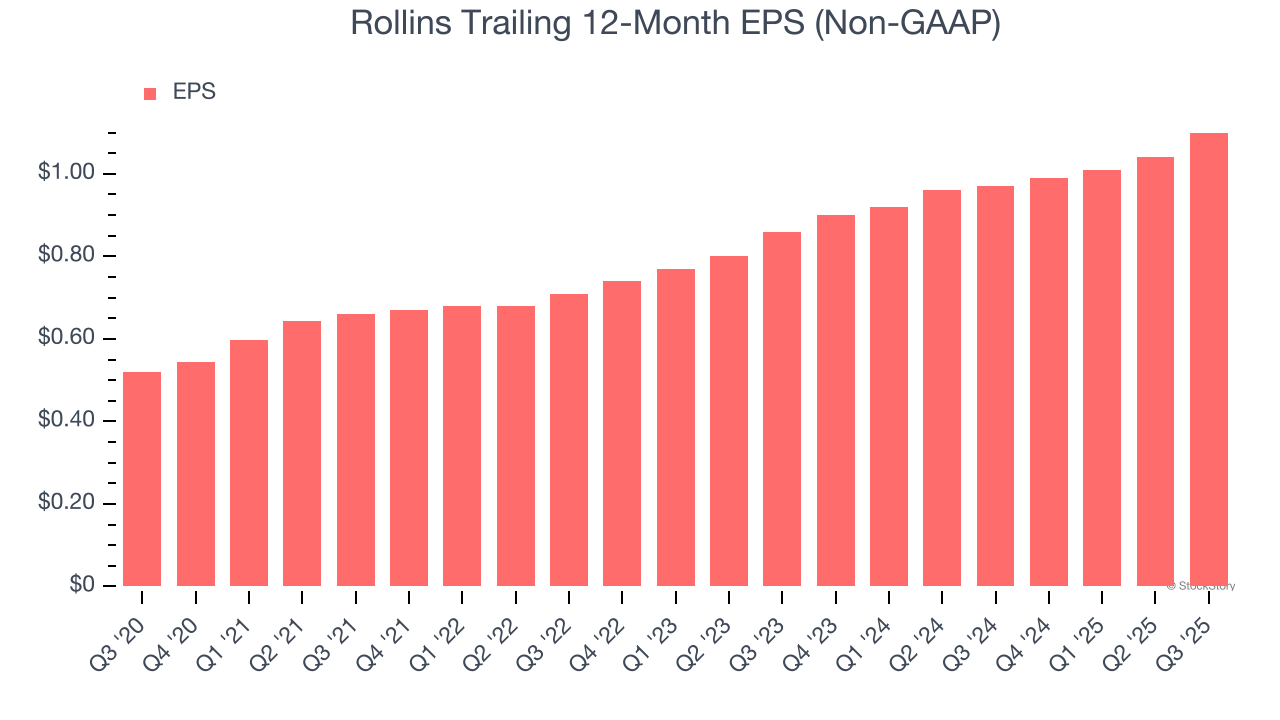

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Rollins’s EPS grew at a spectacular 16.2% compounded annual growth rate over the last five years, higher than its 11.5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

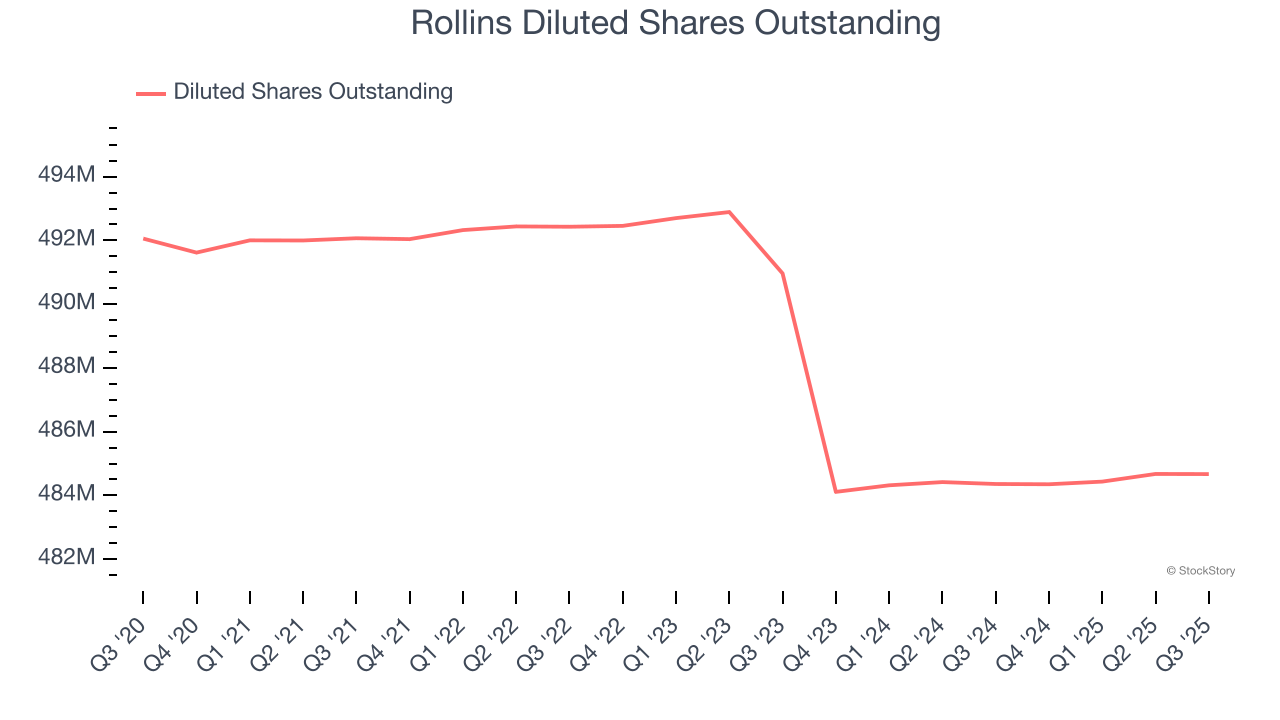

Diving into the nuances of Rollins’s earnings can give us a better understanding of its performance. A five-year view shows that Rollins has repurchased its stock, shrinking its share count by 1.5%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Rollins, its two-year annual EPS growth of 13.1% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q3, Rollins reported adjusted EPS of $0.35, up from $0.29 in the same quarter last year. This print beat analysts’ estimates by 6.4%. Over the next 12 months, Wall Street expects Rollins’s full-year EPS of $1.10 to grow 10.2%.

Key Takeaways from Rollins’s Q3 Results

It was encouraging to see Rollins beat analysts’ EPS and EBITDA expectations this quarter. Overall, this print had some key positives. The stock traded up 1.6% to $54.74 immediately after reporting.

So do we think Rollins is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.