Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at Charles River Laboratories (NYSE: CRL) and its peers.

Companies specializing in drug development inputs and services play a crucial role in the pharmaceutical and biotechnology value chain. Essential support for drug discovery, preclinical testing, and manufacturing means stable demand, as pharmaceutical companies often outsource non-core functions with medium to long-term contracts. However, the business model faces high capital requirements, customer concentration, and vulnerability to shifts in biopharma R&D budgets or regulatory frameworks. Looking ahead, the industry will likely enjoy tailwinds such as increasing investment in biologics, cell and gene therapies, and advancements in precision medicine, which drive demand for sophisticated tools and services. There is a growing trend of outsourcing in drug development for nimbleness and cost efficiency, which benefits the industry. On the flip side, potential headwinds include pricing pressures as efforts to contain healthcare costs are always top of mind. An evolving regulatory backdrop could also slow innovation or client activity.

The 8 drug development inputs & services stocks we track reported a very strong Q2. As a group, revenues beat analysts’ consensus estimates by 4.4%.

Luckily, drug development inputs & services stocks have performed well with share prices up 24.1% on average since the latest earnings results.

Charles River Laboratories (NYSE: CRL)

Named after the Massachusetts river where it was founded in 1947, Charles River Laboratories (NYSE: CRL) provides non-clinical drug development services, research models, and manufacturing support to pharmaceutical and biotechnology companies.

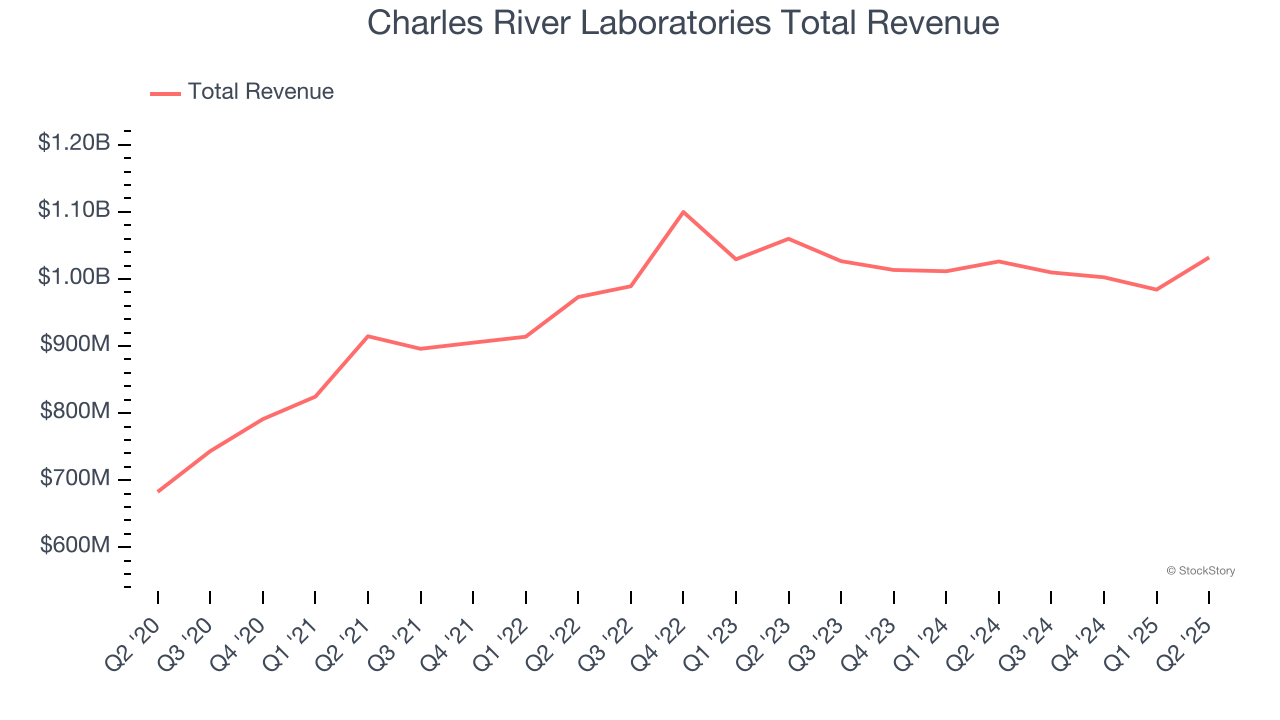

Charles River Laboratories reported revenues of $1.03 billion, flat year on year. This print exceeded analysts’ expectations by 4.6%. Overall, it was an incredible quarter for the company with a solid beat of analysts’ organic revenue estimates and a beat of analysts’ EPS estimates.

James C. Foster, Chair, President and Chief Executive Officer, said, “We are continuing to see clear signs that the biopharmaceutical demand is stabilizing, and in this environment, we are making gradual progress to return to organic revenue growth. This progress was demonstrated in our solid second-quarter financial performance, driven principally by favorable results in our DSA segment.”

Interestingly, the stock is up 3.6% since reporting and currently trades at $173.47.

Is now the time to buy Charles River Laboratories? Access our full analysis of the earnings results here, it’s free for active Edge members.

Best Q2: West Pharmaceutical Services (NYSE: WST)

Founded in 1923 and serving as a critical link in the pharmaceutical supply chain, West Pharmaceutical Services (NYSE: WST) manufactures specialized packaging, containment systems, and delivery devices for injectable drugs and healthcare products.

West Pharmaceutical Services reported revenues of $766.5 million, up 9.2% year on year, outperforming analysts’ expectations by 5.6%. The business had an incredible quarter with an impressive beat of analysts’ revenue estimates and a solid beat of analysts’ full-year EPS guidance estimates.

The market seems happy with the results as the stock is up 17.9% since reporting. It currently trades at $267.93.

Is now the time to buy West Pharmaceutical Services? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q2: Azenta (NASDAQ: AZTA)

Serving as the guardian of some of medicine's most valuable materials, Azenta (NASDAQ: AZTA) provides biological sample management, storage, and genomic services that help pharmaceutical and biotechnology companies preserve and analyze critical research materials.

Azenta reported revenues of $143.9 million, flat year on year, falling short of analysts’ expectations by 3.8%. It was a softer quarter as it posted a significant miss of analysts’ revenue estimates.

Azenta delivered the weakest performance against analyst estimates and slowest revenue growth in the group. The stock is flat since the results and currently trades at $32.64.

Read our full analysis of Azenta’s results here.

Fortrea (NASDAQ: FTRE)

Spun off from Labcorp in 2023 to focus exclusively on clinical research services, Fortrea (NASDAQ: FTRE) is a contract research organization that helps pharmaceutical, biotech, and medical device companies develop and bring their products to market through clinical trials and support services.

Fortrea reported revenues of $710.3 million, up 7.2% year on year. This number beat analysts’ expectations by 12%. Overall, it was a stunning quarter as it also logged a beat of analysts’ EPS estimates and an impressive beat of analysts’ revenue estimates.

Fortrea delivered the biggest analyst estimates beat and highest full-year guidance raise among its peers. The stock is up 55.4% since reporting and currently trades at $10.22.

Read our full, actionable report on Fortrea here, it’s free for active Edge members.

Medpace (NASDAQ: MEDP)

Founded in 1992 as a scientifically-driven alternative to traditional contract research organizations, Medpace (NASDAQ: MEDP) provides outsourced clinical trial management and research services to help pharmaceutical, biotechnology, and medical device companies develop new treatments.

Medpace reported revenues of $603.3 million, up 14.2% year on year. This print topped analysts’ expectations by 11.3%. It was a stunning quarter as it also put up an impressive beat of analysts’ organic revenue estimates and a solid beat of analysts’ revenue estimates.

The stock is up 71.5% since reporting and currently trades at $529.98.

Read our full, actionable report on Medpace here, it’s free for active Edge members.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.