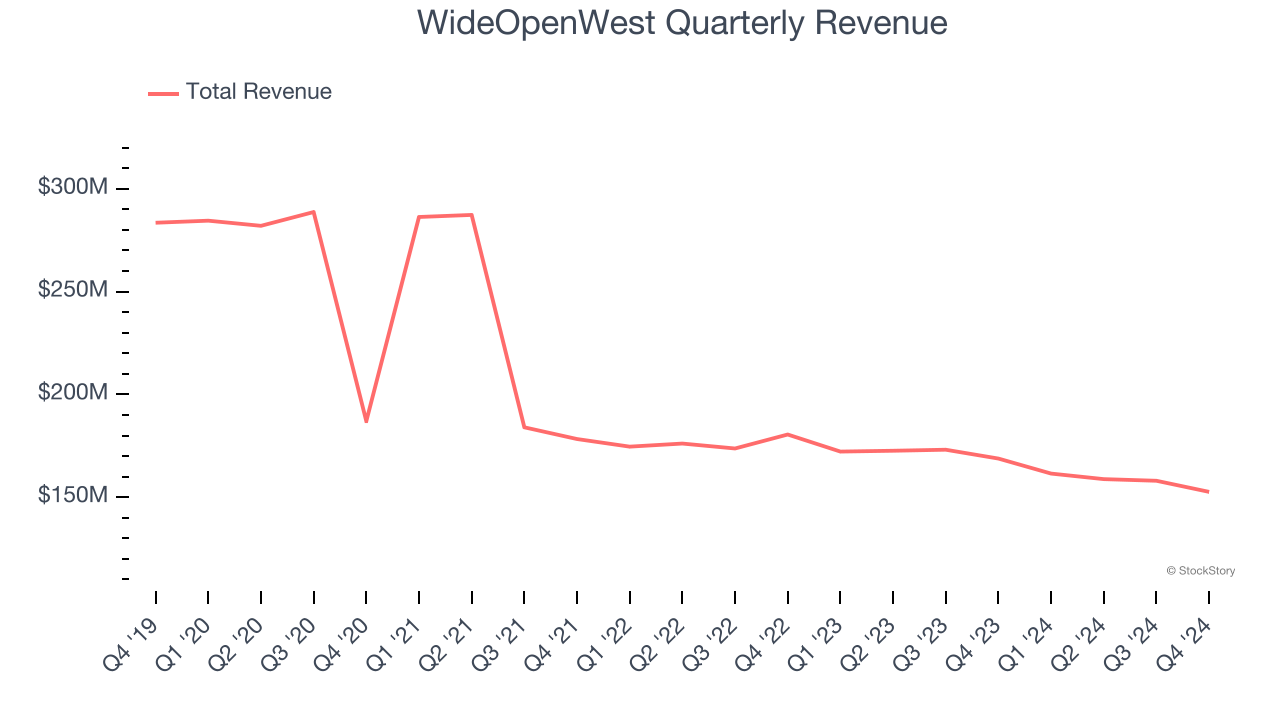

Broadband and telecommunications services provider WideOpenWest (NYSE: WOW) missed Wall Street’s revenue expectations in Q4 CY2024, with sales falling 9.6% year on year to $152.6 million. On the other hand, the company expects next quarter’s revenue to be around $148 million, close to analysts’ estimates. Its GAAP loss of $0.13 per share was 14.5% above analysts’ consensus estimates.

Is now the time to buy WideOpenWest? Find out by accessing our full research report, it’s free.

WideOpenWest (WOW) Q4 CY2024 Highlights:

- Revenue: $152.6 million vs analyst estimates of $154 million (9.6% year-on-year decline, 0.9% miss)

- EPS (GAAP): -$0.13 vs analyst estimates of -$0.15 (14.5% beat)

- Adjusted EBITDA: $73.7 million vs analyst estimates of $70.4 million (48.3% margin, 4.7% beat)

- Revenue Guidance for Q1 CY2025 is $148 million at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for Q1 CY2025 is $73 million at the midpoint, above analyst estimates of $67.6 million

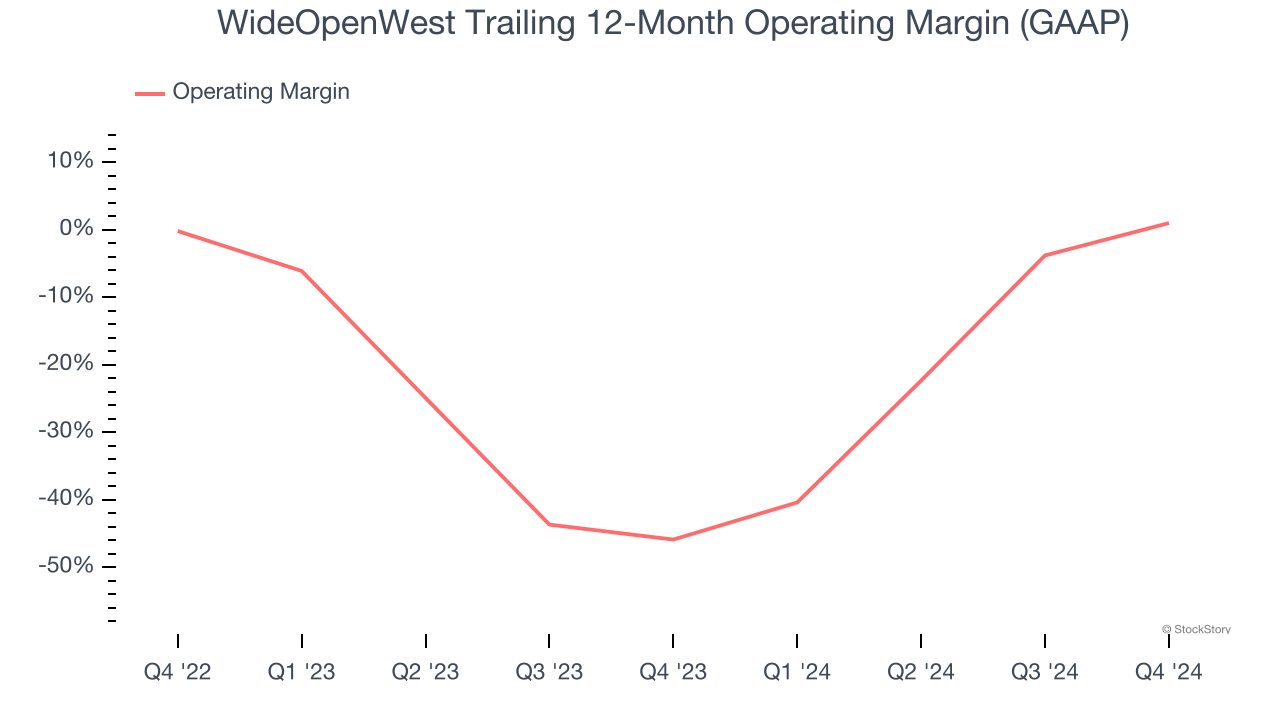

- Operating Margin: -3.1%, up from -21.1% in the same quarter last year

- Free Cash Flow was -$20.8 million compared to -$35.9 million in the same quarter last year

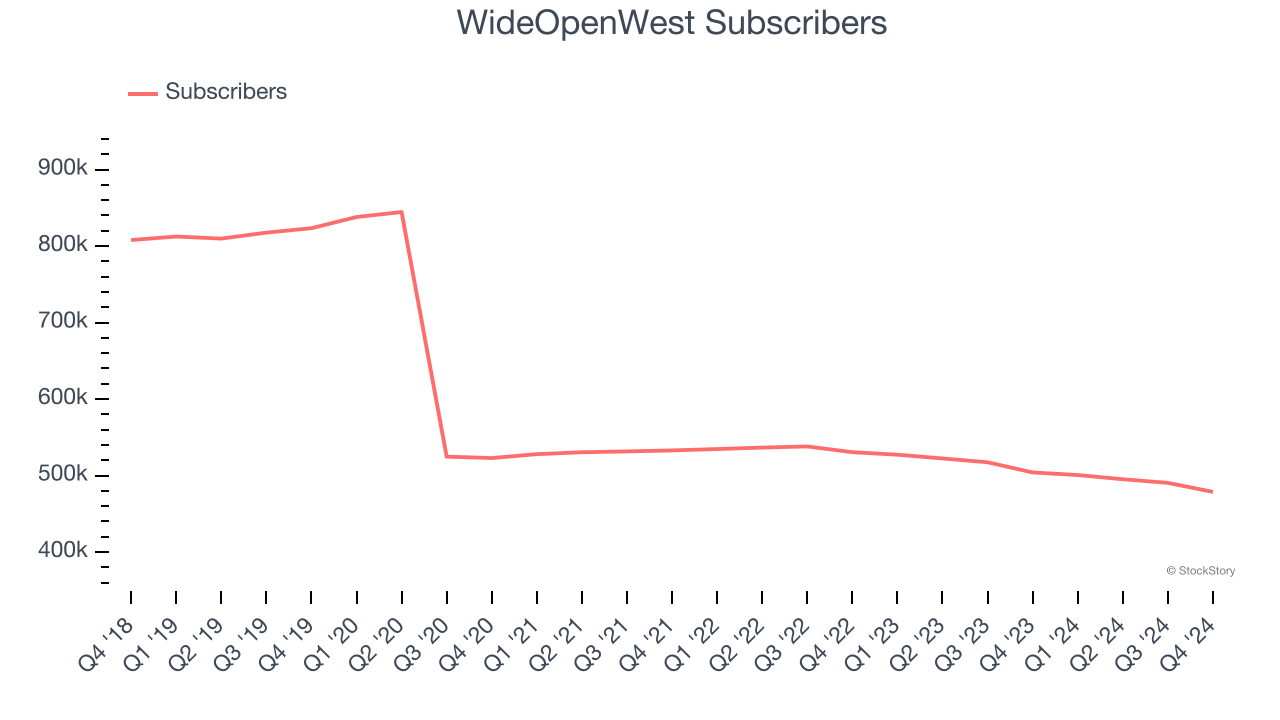

- Subscribers: 478,700, down 25,400 year on year

- Market Capitalization: $342.3 million

"I am pleased with the progress we made in 2024, especially in our Greenfield markets where we passed an additional 31,500 new homes and increased our penetration rate to 16.6%," said Teresa Elder, WOW!'s CEO.

Company Overview

Initially started in Denver as a cable television provider, WideOpenWest (NYSE: WOW) provides high-speed internet, cable, and telephone services to the Midwest and Southeast regions of the U.S.

Wireless, Cable and Satellite

The massive physical footprints of cell phone towers, fiber in the ground, or satellites in space make it challenging for companies in this industry to adjust to shifting consumer habits. Over the last decade-plus, consumers have ‘cut the cord’ to their landlines and traditional cable subscriptions in favor of wireless communications and streaming video. These trends do mean that more households need cell phone plans and high-speed internet. Companies that successfully serve customers can enjoy high retention rates and pricing power since the options for mobile and internet connectivity in any geography are usually limited.

Sales Growth

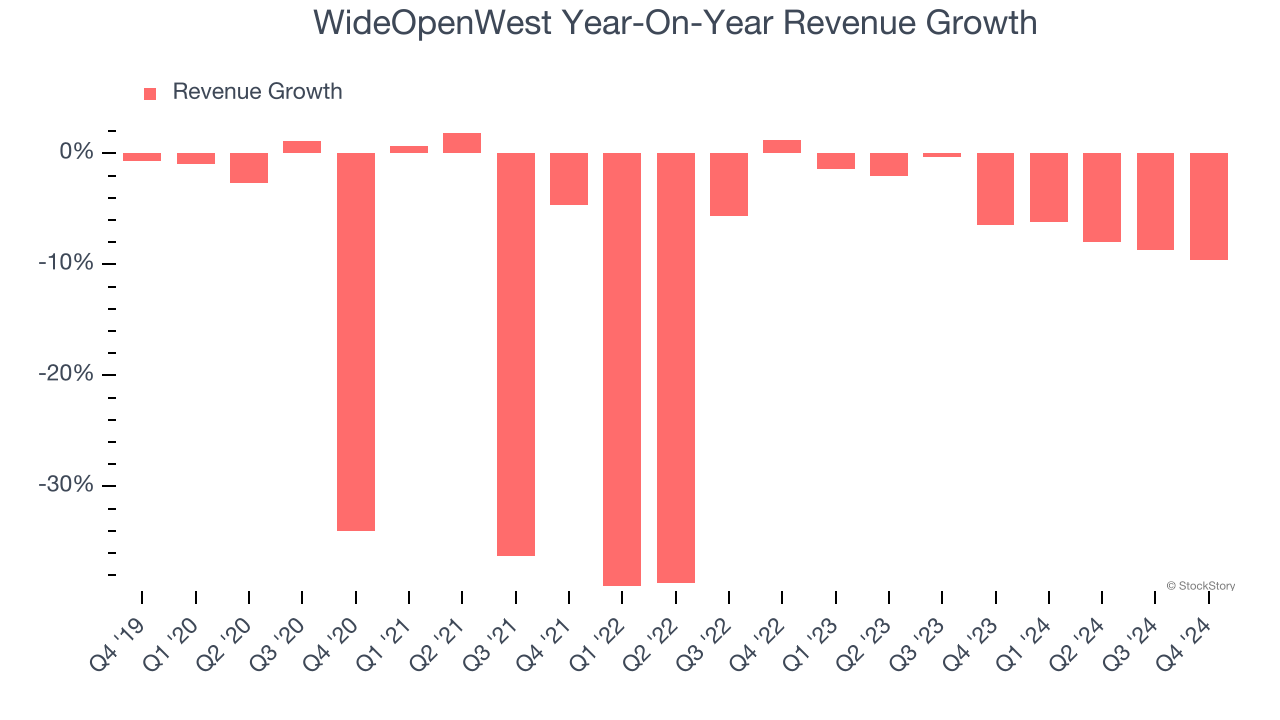

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. WideOpenWest struggled to consistently generate demand over the last five years as its sales dropped at a 11.2% annual rate. This was below our standards and suggests it’s a low quality business.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. WideOpenWest’s annualized revenue declines of 5.4% over the last two years suggest its demand continued shrinking.

We can better understand the company’s revenue dynamics by analyzing its number of subscribers, which reached 478,700 in the latest quarter. Over the last two years, WideOpenWest’s subscribers averaged 4.2% year-on-year declines. Because this number aligns with its revenue growth during the same period, we can see the company’s monetization was fairly consistent.

This quarter, WideOpenWest missed Wall Street’s estimates and reported a rather uninspiring 9.6% year-on-year revenue decline, generating $152.6 million of revenue. Company management is currently guiding for a 8.4% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 8.3% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

WideOpenWest’s operating margin has risen over the last 12 months, but it still averaged negative 23.4% over the last two years. This is due to its large expense base and inefficient cost structure.

In Q4, WideOpenWest generated a negative 3.1% operating margin. The company's consistent lack of profits raise a flag.

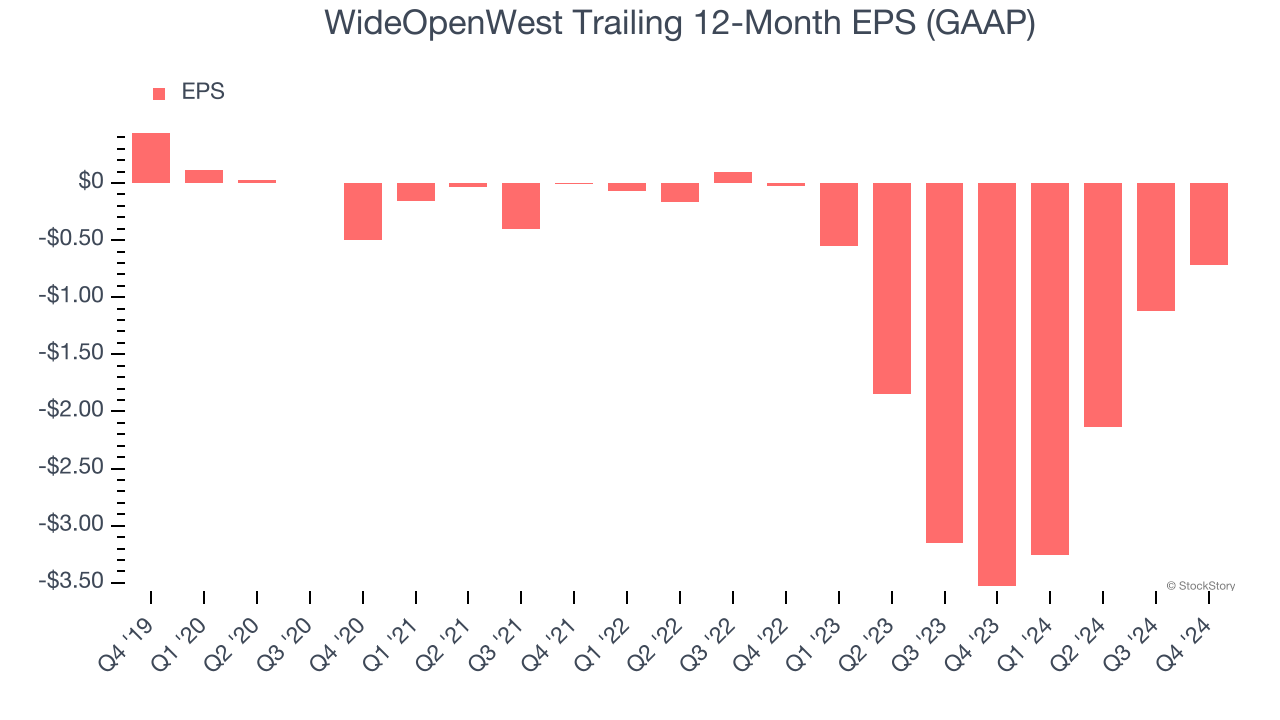

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for WideOpenWest, its EPS declined by 29.4% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q4, WideOpenWest reported EPS at negative $0.13, up from negative $0.53 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast WideOpenWest’s full-year EPS of negative $0.72 will reach break even.

Key Takeaways from WideOpenWest’s Q4 Results

We were impressed by WideOpenWest’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also happy its EPS outperformed Wall Street’s estimates in the quarter. On the other hand, its number of subscribers missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this quarter was mixed but still had some key positives. The stock traded up 9.4% to $4.56 immediately after reporting.

WideOpenWest had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.