The pandemic surged pet ownership. As people stayed home, they embellished in hobbies and embraced adding a fur baby to the family. A Forbes Advisory survey found that 78% of pet owners acquired pets during the pandemic. During the pandemic, in almost one in five households, 23 million brought home a new pet. This explains the surge in pet stocks during the pandemic. However, they have fallen back from normalization against tough yearly comps and weakening consumer discretionary spending.

The pet industry is expected to grow at an 8% CAGR reaching $277 billion by 2030. These stocks have become dogs (pun intended) in 2023 but may seem attractive to value investors or growth investors looking to get into them at lower prices. Here are two pet stocks in the dog house now, but they could escape later this year.

Chewy Inc. (NASDAQ: CHWY)

Chewy is the dominant online retailer of pet supplies and medicines with a 40% market share in the U.S., beating out online giant Amazon.com Inc. (NASDAQ: AMZN), which holds a 30% market share. It also operates the largest pet pharmacy in the U.S. The company whiteboards its e-commerce platform, partnering with veterinarians who promote as their storefronts. Since buying pet food and supplies can be a repetitive chore, they provide an Autoship program that will automatically ship out supplies on a scheduled basis to customers.

Chewy is growing its pet wellness and insurance business and is looking to expand its offering internationally. It also provides hefty discounts to customers that use its Autoship program, which accounts for 73% of its sales. Most of its Autoship products are consumer (pet) staples like food and medicine. Celebrity billionaire co-founder Ryan Cohen started Mr. Chewy with partner Michael Day and sold it to PetSmart for $3.35 billion in 2018. PetSmart split from Chewy, which was spun off as its own standalone company, with neither company owning any piece of the other.

Surprise Profit

Chewy reported a surprise profit in its Q4 2022 earnings report on Mar. 12, 2023. The company reported an EPS profit of $0.16 versus consensus analyst estimates for a loss of (-$0.10), a $0.26 beat. Revenues grew 13.5% YoY to $2.71 billion beating the $2.65 billion analyst estimates. Adjusted EBITDA rose $120 million to $92 million from the year-ago period. However, weakness in consumer discretionary spending caused its active customers to slip by 100,000 sequentially to 20.4 million. Nearly 60% of Chewy's customers came on board during the pandemic, which makes its comps challenging due to the normalization. The company expects 11% YoY revenue growth for the full-year 2023 between $11.1 billion to $11.3 billion.

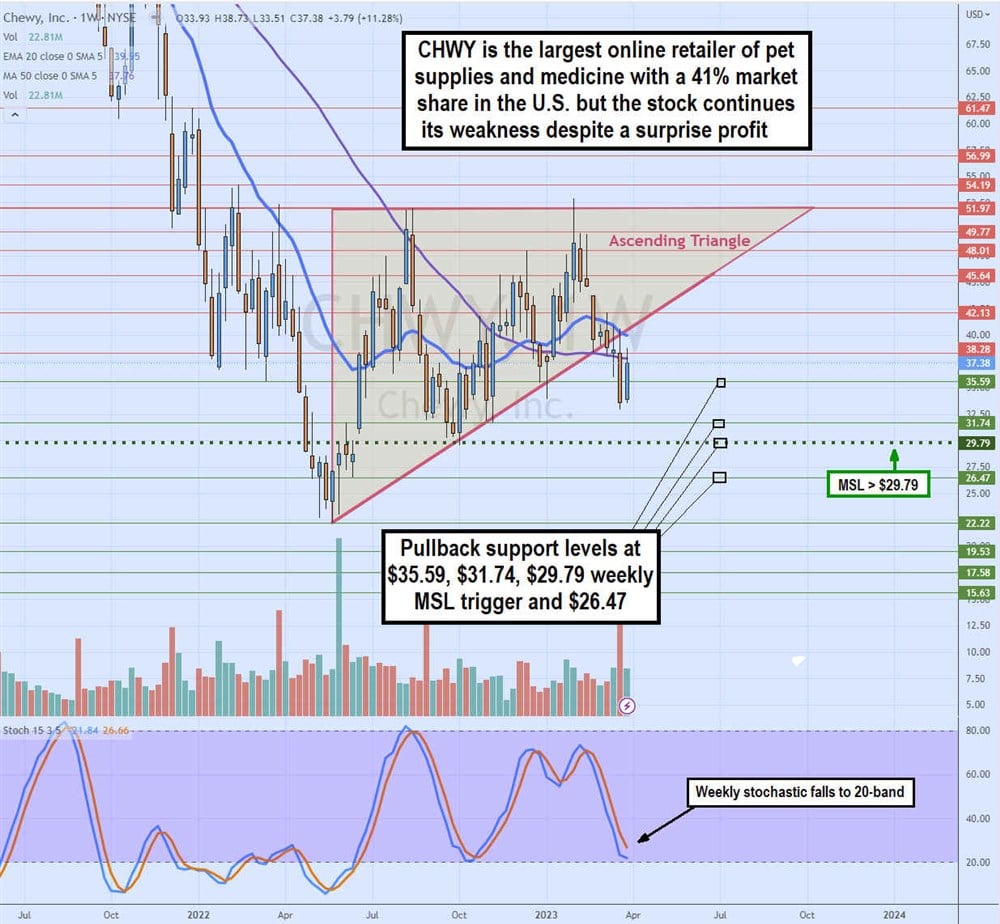

CHWY Weekly Ascending Triangle Breakdown

CHWY failed to attempt a weekly ascending triangle breakout through the $51.96 flat top trendline. Shares fell back down through the rising trendline at $38.28, which it needs to recover to stay within the triangle. The weekly stochastic has fallen to the 20-band. If shares can bounce off the 20-band, then it may attempt another breakout. Otherwise, it could continue to fall lower toward its $22.22 swing low. Pullback support levels are $35.59, $31.74, $29.79, and $26.47. The MarketBeat MarketRank™ Forecast gives CHWY stock a 2 out of 5 stars with a 15% upside price target of $43.

Petco Health and Wellness Company Inc. (NASDAQ: WOOF)

This brick-and-mortar pet store chain operates nearly 1,500 locations with 200 in-store veterinary clinics. While the company also sells products online, its physical locations account for most of its business. Stores offer a one-stop shop for grooming, training, medicine, pet food, and pet supplies. The company offers pet insurance and a subscription-based wellness plan under Vital Care. The company spooked investors with a weak top and bottom line forecast for 2023.

Severely Lowering the Bar

Petco reported EPS of $0.23 versus the $0.22 consensus analyst estimates for its Q4 2022. Revenues grew 4.2% YoY to $1.58 billion beating $1.57 billion analyst estimates. The company issued full-year 2023 guidance for EPS to fall, coming in between ($0.21) to ($0.13) versus an EPS profit of $0.74 consensus analyst estimates. Sales are expected between $6.15 billion to $6.28 billion, falling short of the $6.36 billion consensus analyst estimates. The company will make $100 million in principal payments on its term loan in addition to an estimated increase in interest expense between $44 million and $54 million.

Weekly Descending Triangle Breakdown

WOOF has a weekly descending triangle breakdown in effect. The flat bottom trendline of $9.12 is also the weekly market structure low (MSL) trigger. Shares collapsed through the trendline on its earnings release but attempted to coil back into the triangle. The weekly stochastic continues to fall towards the 20-band. The weekly 20-period exponential moving average (EMA) resistance is falling at $10.44. Pullback support levels are at a $7.59 weekly swing low, $6.55, $5.54, and $4.53. The MarketBeat MarketRank™ Forecast gives WOOF stock a 3 out of 5 stars with a 37.4% upside price target of $12.36.