On March 16, Seaport Research downgraded Qualcomm (QCOM) stock to a “Sell” rating, assigning a price target of $100. The stock currently trades 30% above this level, which means that analysts are looking at significant downside in the coming weeks.

Seaport Research isn’t the only firm that rates QCOM stock as a “Sell.” Bank of America Securities and Morgan Stanley are also bearish on its prospects, assigning “Underperform” and “Underweight” ratings with price targets of $145 and $132, respectively. Over the course of the last two months, multiple analysts have lowered their targets for QCOM stock, with Qualcomm having already lost 24% so far in 2026.

On a slightly positive note, the company is doing all it can to regain investor trust, recently announcing a stock buyback program worth $20 billion. This is on top of the $2.1 billion remaining from its previous buyback announced in November 2024. There is no set timeline for the freshly announced buyback program, which will happen at the discretion of management upon prevailing market conditions.

About Qualcomm Stock

Qualcomm is a fabless semiconductor company that specializes in mobile processors, 5G, IoT, and chips for the automotive industry, among others. The company is currently headquartered in San Diego, California.

QCOM stock is down roughly 18% in the last 12 months, a significant underperformance compared to the iShares Semiconductor ETF’s (SOXX) 64% gain in the same period. The reasons for this underperformance are mainly associated with supply constraints in the smartphone industry, which drives the company’s core business.

A natural question following the stock buyback news amid fundamental issues in the stock is whether the company can afford to spend so much money on buying back its own shares. After all, if industry headwinds are likely to keep QCOM stock under pressure, is a buyback worth the hassle for investors?

Right now, Qualcomm sits on $7.2 billion in cash and cash equivalents with free cash flow healthy enough to support the buyback, so there is hardly concern there. The company also shouldn’t have a problem supporting its dividend, which was just raised to $0.92. That gives the stock a forward dividend yield of 2.71%, well above the five-year average trailing-12-month dividend yield of 2.13%. At a time when it is facing pressure from multiple fronts, QCOM stock could become a favorite for income-focused investors once again.

Qualcomm Stock Sinks on Poor Guidance

Qualcomm announced its fiscal first-quarter results on Feb. 4. Despite beating Wall Street estimates, QCOM stock fell on poor guidance. For fiscal Q2 2026, the company expects EPS of $2.55 at the midpoint on revenue of $10.6 billion at the midpoint. Wall Street expectations are for EPS of $2.85 and revenue of $11.1 billion.

According to management, the unimpressive guidance is mainly due to the global memory shortage. This is also what’s driving the negative analyst sentiment since earnings. Because many smartphone companies buy memory chips separately and then pair them with Qualcomm’s processors, they are hesitant to order too many processors without having the required memory to go along with them. In other words, the availability of memory is currently defining the market size, and is out of Qualcomm’s control.

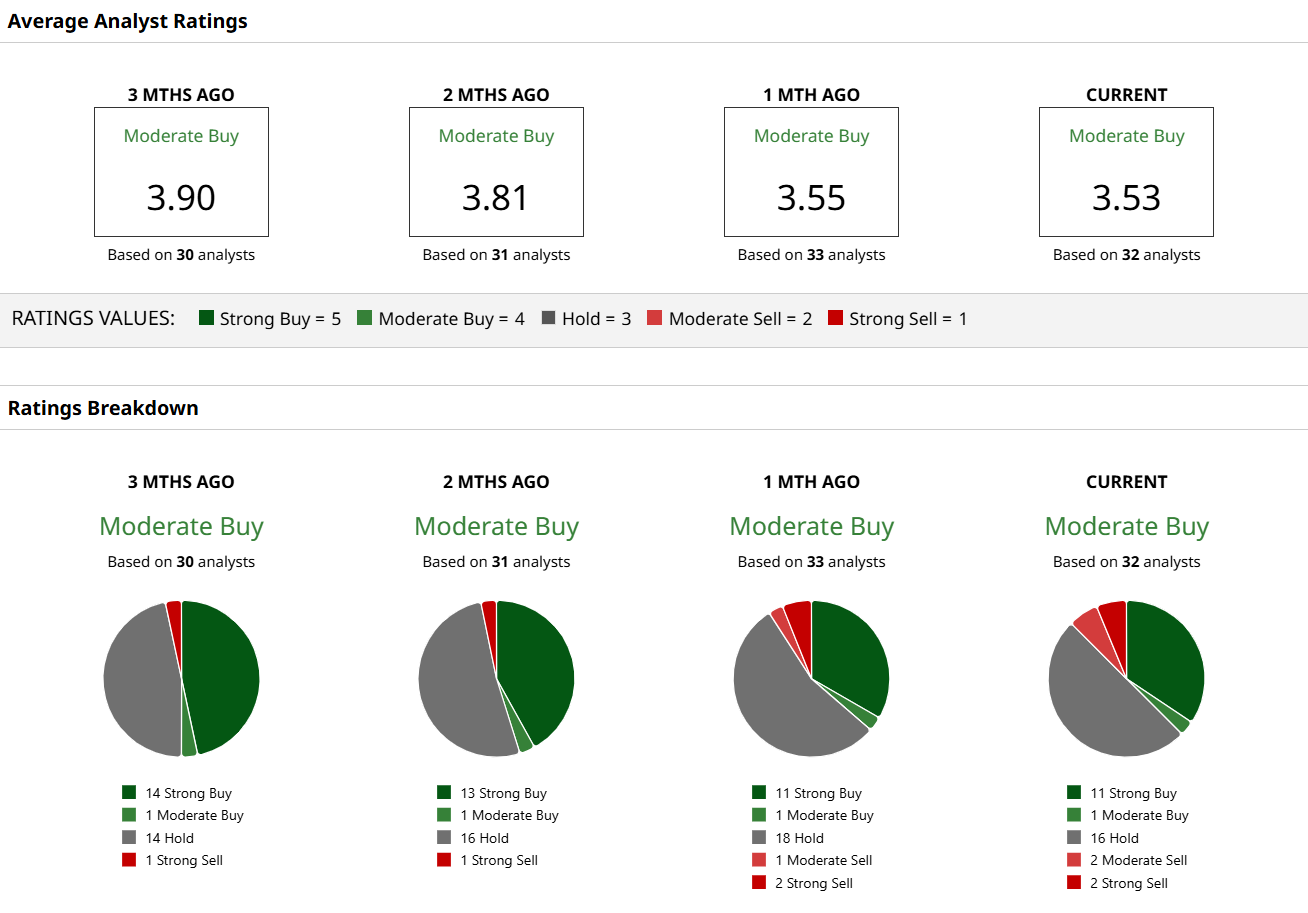

What Are Analysts Saying About Qualcomm Stock?

Several analysts have lowered their price targets on QCOM stock since the Q1 earnings report. Seaport Research also offers the lowest price target on Wall Street, making it the most bearish firm at the moment. The mean target price for the stock is still a healthy $161.32, implying 24% potential upside from here.

Historically, QCOM stock has performed the worst in the first three months of the year. One could argue that the worst has already been priced in for the stock, with multiple headwinds hurting shares at the same time. This is something short-term traders will have a keen eye on, among other QCOM trading strategies.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Does Rocket Lab's $2 Billion Backlog Offset Dilution Concerns?

- Ryan Cohen’s ‘Hollow Men’ Rant Puts Corporate America — and Boards — on Notice

- QCOM Stock Warning: Why Analysts Warn Qualcomm Could Plunge More Than 20% from Here

- This Cathie Wood Stock Is Down 36% Over the Past 2 Years. She Still Can’t Get Enough.