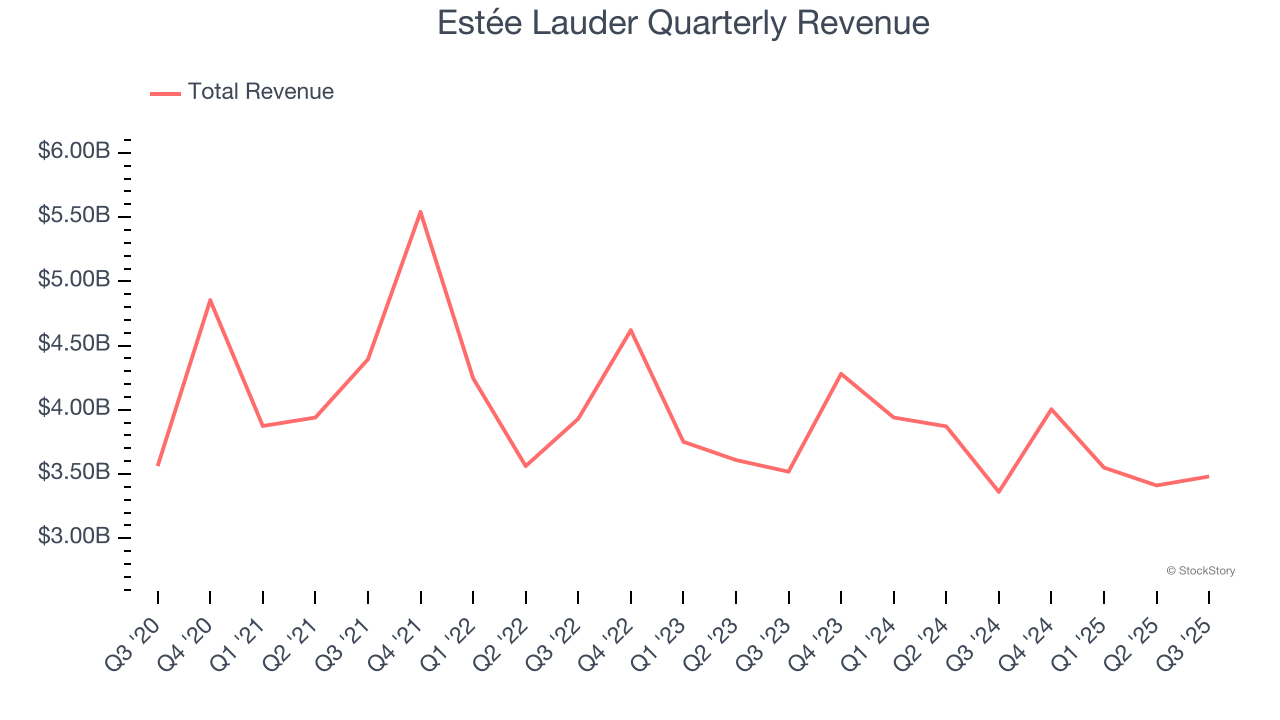

Beauty products company Estée Lauder (NYSE: EL) beat Wall Street’s revenue expectations in Q3 CY2025, with sales up 3.6% year on year to $3.48 billion. Its non-GAAP profit of $0.32 per share was 81.9% above analysts’ consensus estimates.

Is now the time to buy Estée Lauder? Find out by accessing our full research report, it’s free for active Edge members.

Estée Lauder (EL) Q3 CY2025 Highlights:

- Revenue: $3.48 billion vs analyst estimates of $3.38 billion (3.6% year-on-year growth, 2.9% beat)

- Adjusted EPS: $0.32 vs analyst estimates of $0.18 (81.9% beat)

- Adjusted EBITDA: $369 million vs analyst estimates of $369 million (10.6% margin, in line)

- Management reiterated its full-year Adjusted EPS guidance of $2 at the midpoint

- Operating Margin: 4.9%, up from -3.6% in the same quarter last year

- Free Cash Flow was -$436 million compared to -$811 million in the same quarter last year

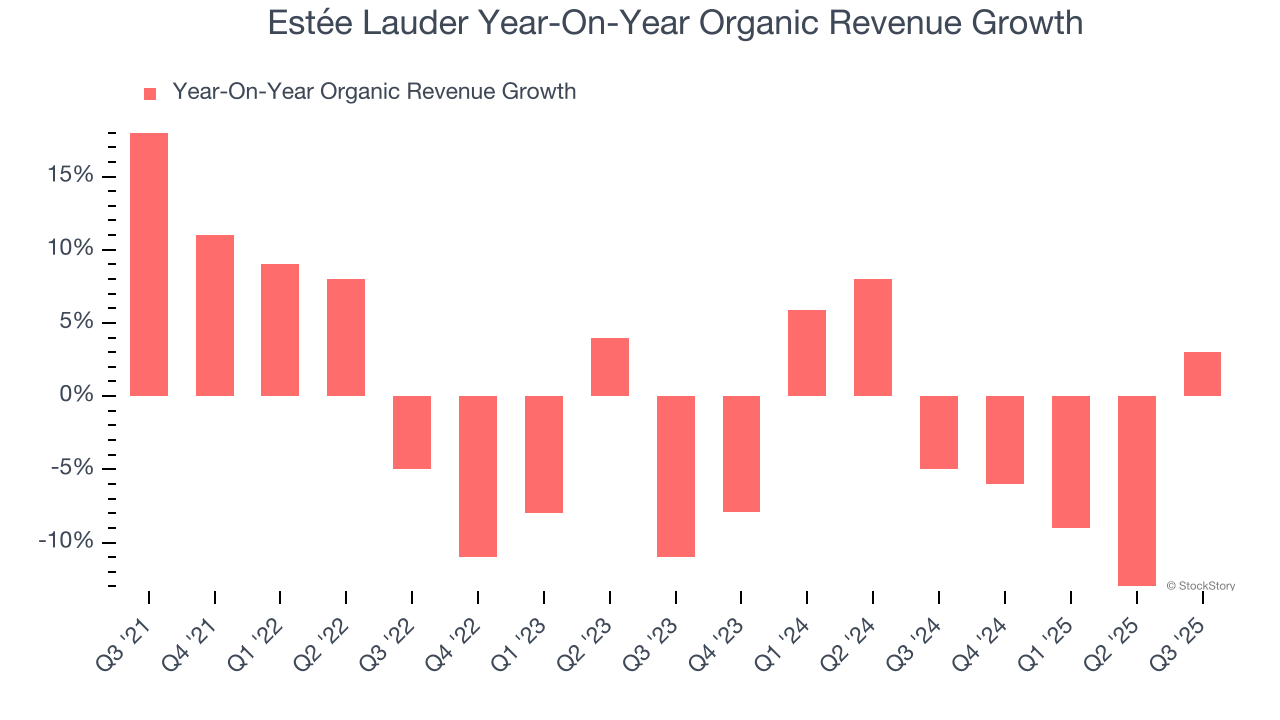

- Organic Revenue rose 3% year on year vs analyst estimates of flat growth (360.8 basis point beat)

- Market Capitalization: $35.08 billion

“We had a strong start to fiscal 2026 as we execute on our Beauty Reimagined strategy—returning to organic sales growth, gaining prestige beauty share in a few key strategic areas of focus, and improving profitability. Encouragingly, we are building momentum across the organization from the significant operational changes we have executed to-date to be faster and more agile,” said Stéphane de La Faverie, President and CEO.

Company Overview

Named after its founder, who was an entrepreneurial woman from New York with a passion for skincare, Estée Lauder (NYSE: EL) is a one-stop beauty shop with products in skincare, fragrance, makeup, sun protection, and men’s grooming.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $14.45 billion in revenue over the past 12 months, Estée Lauder is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there are only so many big store chains to sell into, making it harder to find incremental growth. To accelerate sales, Estée Lauder likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, Estée Lauder struggled to generate demand over the last three years. Its sales dropped by 5.8% annually, a poor baseline for our analysis.

This quarter, Estée Lauder reported modest year-on-year revenue growth of 3.6% but beat Wall Street’s estimates by 2.9%.

Looking ahead, sell-side analysts expect revenue to grow 3.5% over the next 12 months. While this projection suggests its newer products will spur better top-line performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

Estée Lauder’s demand has been falling over the last eight quarters, and on average, its organic sales have declined by 3% year on year.

In the latest quarter, Estée Lauder’s organic sales rose by 3% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

Key Takeaways from Estée Lauder’s Q3 Results

It was good to see Estée Lauder beat analysts’ organic revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed. Overall, we still think this was a decent quarter with some key metrics above expectations. The stock traded up 5.2% to $102.50 immediately after reporting.

Estée Lauder had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.